I’ve said it before, and I’ll say it again: I don’t envy anyone tasked with penning daily market wraps for mainstream financial media outlets.

I imagine it’s a thankless task. It’s just boilerplate copy, and the byline is meaningless. It’s not exactly a résumé builder. Nobody ever won a Pulitzer for editorializing around one session’s cross-asset price action.

More importantly for investors, most of those wraps are just plain wrong to the extent they rely almost exclusively on retrofitted explanations, tortured interpretations of macro developments and soundbites from the kind of people who never miss an episode of “Power Lunch” on CNBC.

The S&P was up more than 3% in three days through midday Tuesday (who knows where stocks will be by the time you read this), and accurate accounts of why were in short supply. So, I thought I’d do my solemn duty and shed a little light on the situation.

For one thing, the dollar was down 3% over the same period. Funny how that works. The DXY’s 1.8% plunge late last week (documented here on Friday) was anomalous. In fact, as Bloomberg’s Simon Flint pointed out on the terminal, Friday’s swoon counted “in the bottom 0.2% of all moves going back to 1970.”

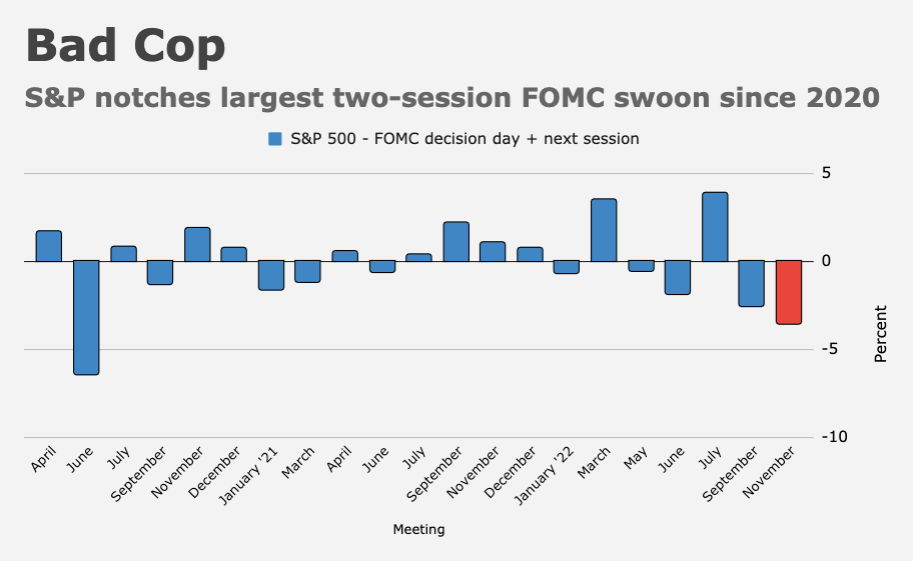

On Tuesday, Nomura’s Charlie McElligott noted that the three-day move (figure above) was a four-sigma event.

That matters. And it matters a lot. “This violent ‘weak dollar’ trade from the rush to monetize USD-longs is not just creating a massive ‘impulse easing’ in financial conditions, but specifically for US equities,” McElligott wrote, noting that USD liquidity screened “as the #1 largest” positive price-driver macro factor variable for the S&P 500 and Russell 2000 in a quant model, and the second largest for the Nasdaq.

Meanwhile, a predictable list of options- and flow-related catalysts were at work. “The legacy ‘short gamma / extreme negative $delta’ profile of the options market [has seen] enormous ‘positive $delta’ flows on put monetization as they then move OTM, causing dealers to cover their short hedges in futures,” Charlie went on to say. “Knowing the market is under-positioned for rallies and that dealers are covering short delta, we see immediate grab into 0-1 days-to-expiration calls,” as market participants, wise to the zeitgeist, look “to exploit these dynamics and creat[e] further ‘positive $delta’ to buy as we rally, which are then also monetized / closed into strength by EOD,” he added.

For regular readers, that’s all very familiar, particularly the bit about monetizing downside expressions at the first opportunity, then gaming the knock-on effects by leveraging (figuratively and literally) very short-dated options to play the expected rebound. It amounts to creating a same-day, self-fulfilling prophecy and participating in it. Everyone’s doing it. It’s no longer the sole purview of retail investors.

In the wee hours of Tuesday morning in New York, S&P futures were down. By noon, they’d rallied 65 handles, and wouldn’t you know it, almost two thirds of SPX options volume was in 0-1DTE (tables below).

“They’re playing the game, trying to ‘gamma squeeze’ it,” McElligott remarked. Nomura estimated an implied positive $delta add of $287 billion over just two sessions.

At the same time, McElligott flagged nearly $50 billion in buy-to-cover flows from CTA trend over the past five weeks (so, not specific to the last two days, but germane nevertheless) and $13 billion in added vol control equities exposure over the past two weeks, all along with spec covering in US equity futures last week.

The irony in all of this (there are actually layers of irony, all of which were explored in Charlie’s Tuesday note, but I’ll make it easy on readers, and myself, by employing the obvious punchline) is that it comes on the heels of the largest two-session, FOMC S&P selloff since summer of 2020.

That selloff was surely what Jerome Powell wanted to see given the Fed’s need to tighten financial conditions through engineering a reverse wealth effect and capping equities. By midday Tuesday, that selloff had totally reversed. If you see a “reversal of the reversal,” so to speak, by the end of Tuesday’s trading, don’t be surprised. Everyone’s a day trader now.

{kind=link}

Wow, look at the action in BTC. Did someone say “Going down”?

It’s impossible to make any sense of crypto today. Or any day, for that matter, but particularly today. Tuesday was all about the FTX thing. In my opinion, it’s too silly for serious people to spend time on. Which is why I’m not spending any time on it. I tried this year, but crypto just isn’t for real investors, and won’t ever be. I don’t intend to cover it in a serious way going forward.

Might it have value as some sort of proxy for risk-on/-off sentiment?

Bankman-Fried was running around “bailing out” other crypto companies, as far as I can tell to keep valuations from collapsing. Looks like he’s been knee-capped by Binance, and now been forced to sell to the knee-capper. Crypto consolidation is a rough sport.

@jyl you are very diplomatic. A more cynical observer might equate crypto consolidation with Ponzi schemes being exposed.

@mfn, I probably just don’t grasp how convoluted and bogus crypto is.

I paid attention to it until it became clear that whatever is required to be a successful investor in crypto-related things is not within my skillset, and then I largely stopped paying attention.

(I believe that while there are many ways to invest, only fools and genuises can be good at multiple ways. If one is not the latter, best to avoid being the former.)

Reading about H’s spelunking in the DeFi Depths and Crypto Caves further inflamed my disinterest. Those posts were among H’s most valuable work, I think.

SBF caught my attention because he was earlier throwing money at political candidates in my state, so I paid slightly more attention to him.

Same with SPACs, meme stocks, all that stuff. It’s kind of entertaining to watch, for a while, and then you have to get back to work.

Spoke too soon. Binance says after reviewing FTX books, likely not doing bailout.

Good for you. I’m so sick of hearing about it. As I’m sure you’ve noticed, Bloomberg feels obliged to cover it (as I suppose they must) and that’s more than enough for me.

Like you, I spend almost none of my time on crypto news. However, today’s large drawdowns in even the major cryptocurrencies made me interested in reading your insightful and fun take (a description I don’t use very frequently when referring to finance articles) on that

Crypto = The most epic vaporware. Not only is it the new pets.com, but its also not ahead of its time in the sense that eventually ecommerce was eventually a thing.

As H points out, crypto doesn’t add anything new. I could create a digital image and sell it on my website. I can send people US Dollars using Venmo. We still have 0 actual real world, practical use cases for crypto.

“Smart contracts” you say? Oh sure, yeah I want to sell my house using a completely automated system to make sure everything goes as planned…

Open up the New York Times, see this — https://www.nytimes.com/2022/11/08/arts/design/frida-kahlo-nft-martin-mobarak.html

Yesterday I got a survey from Barron’s (I get them all the time .. my big mouth). As usual they are late to the party. They were asking for my level of interest in regular coverage on special topics, like crypto. They wondered if I would be willing to pay $30 a month for this promised coverage. I said, “Are you serious?”

Is it just me or if CPI comes in even slightly under expectations are stocks going to rip one for the ages?

I don’t know how slight or how much of a rip, but I do think there are a lot of managers desperate to salvage the year.