Hope springs eternal, which is why, when US equities staged their fifth biggest intraday reversal in history this week, some took the opportunity to ask if the lows were in.

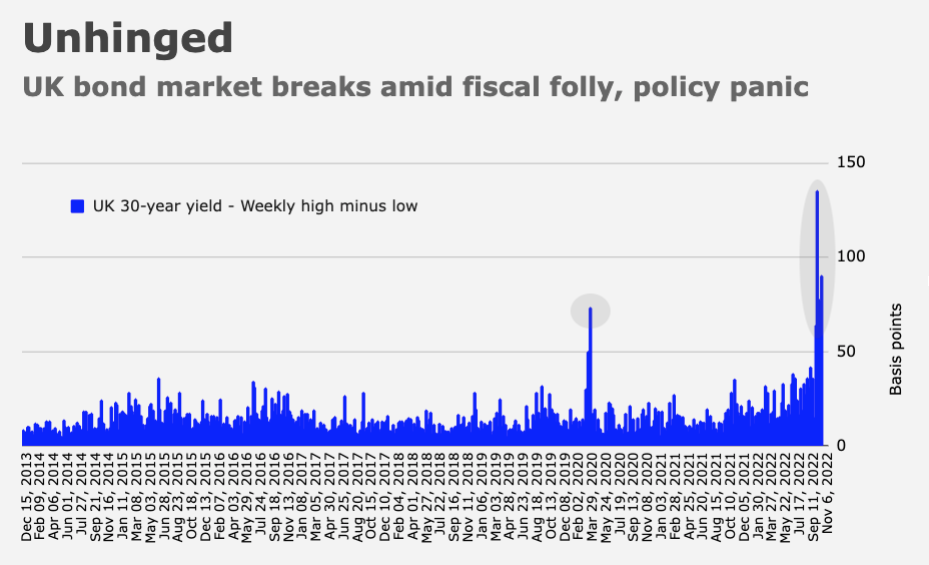

Such hopes were summarily dashed on Friday, when stocks slid again, a baleful bookend to a ludicrous week defined by unprecedented volatility in the UK rates complex.

One popular US Treasury ETF fell an eleventh week in 12, while the S&P fell a fourth week in five and a seventh in nine. The simple figure (below) gives you a sense of the ongoing pain for simple 60/40 strategies.

That’s almost too bad to be true. The latter half of the so-called “Great Moderation” was defined by an almost religious belief in the sanctity and stability of a negative stock-bond return correlation. Inflation is a heretic.

I assume most readers are aware of this, but there’s no precedent for 2022’s 60/40 drawdown. It’s the worst in history. And it’s not close.

The figure (below) from BofA’s Michael Hartnett never fails to elicit raised eyebrows.

“2022’s annualized return on a 60/40 portfolio is -34.4%, the worst in the past 100 years,” Hartnett wrote, in his latest. So, 2022 is on track to be the year during which the simplest of purportedly “foolproof” asset allocation strategies underperformed its historical mean by 45 percentage points.

Notably, even a portfolio that’s 25/25/25/25 in cash, commodities, stocks and bonds is on track for a 12% loss, the worst since the financial crisis. There really isn’t anywhere to hide, unless you’ve been 100% in cash, and even then, your (rising) nominal returns have been eroded by inflation.

The figure (below) shows the drawdown in what, ostensibly anyway, should be an even safer balanced portfolio.

That too is egregious. You’ll note that things have deteriorated quite rapidly following the summer rally.

I should emphasize that this goes beyond the notion that The Great Moderation was an anomalous period from a macro standpoint — an aberration rather than a new normal. This is bigger than the (now self-evident) idea that we should’ve been more cautious about accepting certain correlations as akin to natural laws.

I’ve spent countless hours editorializing around those talking points, and I believe wholeheartedly in their explanatory power. But at the risk of lapsing into the colloquial, 2022 is just plain old bad. Global high-grade credit is down 22%. That’s unheard of. In 2008, IG lost just 8%. Global high yield could easily match 2008’s drawdown if the macro environment deteriorates over the balance of the year. Gold is down 9%. It rose 4% in 2008. Admittedly, stocks are unlikely to match 2008’s historic declines, but that’s small comfort given the uniformity of the cross-asset malaise.

And make no mistake, more losses may well be in store for equities. If you ask BofA’s Hartnett, we just aren’t there yet, where “there” means the fabled “Big Low,” a proper noun for some analysts.

The table (below, from BofA) shows that metrics from the bank’s closely followed Global Fund Manager Survey for cash, equity allocations and economic growth, do indicate capitulation. Hartnett also noted that breadth is close to full capitulation, as is the bank’s pseudo-famous “Bull & Bear Indicator.”

What’s missing, Hartnett said, is capitulation from retail (in this case BofA’s private clients) and evidence of fatalism in institutional equity flows.

More importantly, “everyone expects the Fed to cut” at The Big Low, Hartnett reminded investors. “That just ain’t the case today,” he added.

The market is “so oversold and investors so cashed-up” that there’s “decent” scope for a counter-trend rally, but in BofA’s view, the “ultimate lows ain’t seen yet.”

{kind=link}

Historically stock/us treasury bonds are inversely correlated roughly 70% of the time, not 100%. And the exception is generally in a rising rate environment. Bingo! Hindsight capital management is easy, investing is hard. A pandemic shock, followed by a regional Europe war shock was not very predictable either before or its effects afterward, with all due respects to Larry Summers and Mohamed El-Erian. It continues to be tiring to see their commentary everywhere.

“A pandemic shock, followed by a regional Europe war shock was not very predictable either”

Except that the history of Europe is (quite literally) just one long history of huge wars, and every infectious disease expert on the planet warned that a pandemic was just a matter of time. The fact is, we ignored the Putin risk even after he seized Crimea, we failed to make the energy transition fast enough (or if you don’t like energy transitions, then we can say Europe didn’t diversify its supplies despite knowing the Ukraine powder keg might explode at any time) and no Western government had a viable pandemic contingency plan in place. If COVID had been a hemorrhagic fever, we’d probably all be dead. And if the Russian military hadn’t turned out to be totally inept, Kyiv would be run by a puppet regime right now.

Also, I’d reiterate that tilting at the Summers / El-Erian windmill is quixotic. They’re celebrities. Where else are they going to be except on TV and in the mainstream financial media? Saying it’s “tiring” to see them is like saying it’s “tiring” to see Leonardo DiCaprio in movies or “exhausting” to see Joe Kernan anchoring CNBC’s morning programming. Where else are DiCaprio and Kernan going to be if not in movies and on CNBC?

Admittedly, I’m probably too cynical vis-a-vis market participants and observers of all sorts, but I just think people generally fail to extrapolate from the way they experience their own lives. Let’s say you design shoes for Nike. Chances are, you don’t go home at the end of the day and just bombard your family from 5:00 PM until the second they fall asleep with shoe talk. “Listen, I design shoes. So, all I’ve got to say is shoes. I don’t care how your day was or how the kids did at school, because all I can think about is shoes. Shoes. Shoes. And more shoes.”

So, I don’t believe that the vast majority of market participants and/or pundits and/or economists and/or political commentators actually care all that much about any of this stuff at the end of the day. When the cameras go off, and the laptops are shut, and soundbite-/talking point-time is over, the majority of humanity goes home, zones out, eats dinner, hangs out with the family and so on, and doesn’t care one way or another about much of what they spend all day pretending to be obsessed with.

I realize that’s actually the healthy way to live, as opposed to the way I live, which is constantly immersed in some kind of study or analysis every waking hour, but my overarching point in the last paragraph in my comment above is that you can’t take any of these people too seriously. The world is a business. People do what they do not because they care, but because due to the randomized lottery that is human existence, they ended up being economists, or anchors, or actors, or journalists, or whatever else. Sure, they enjoy it (some of them anyway), but they do it because it gives them a livelihood. And everyone’s livelihoods are entangled in a grand structure we call the economy. But, again, it’s all just a business. 95% of people would rather be on the couch, eating or wandering around daydreaming.

This is why I take almost nothing I hear or see seriously. I’ll entertain it in order to entertain my readers, because not every article can be profound. Too much profundity is exhausting for people. Most of the time, in fact, people want to be entertained. There are notable exceptions. For example, Charlie M. pretty clearly loves what he does and is totally immersed in it, which is why he’s so great and why I quote him so often. Also, DB’s Kocic is a genuine deep thinker and it shows in his work.

But more broadly, if you’re looking for true insight into existential issues related to political economy, Larry ain’t it. Neither is El-Erian. And neither are any of the people you see on TV or see tweeting. Crucially: They’re not supposed to be “it.” They’re supposed to entertain you. Like DiCaprio. If you want that genuine insight into political economy, you have to read the crazy people, which typically means going back in history and reaching for the tomes penned by folks for whom life was synonymous with introspection and inquiry. For those people, everything else in life was totally secondary. We don’t have many of those types left.

(Incidentally, I also think our inability to extrapolate as described above is contributing to societal breakdown. We hear some political pundit on TV say something and we forget that in all likelihood, that same person is going to be… you know… watching a college football game on Saturday, eating chips, not ranting and raving about identity politics. That, in turn, makes it difficult for people to relate to one another as people with more in common than not.)

H> constantly immersed in some kind of study or analysis every waking hour

You’re not alone, H. There are plenty of obsessive individuals who stay busy to survive.

Here’s one. Reminded me of you when I read the article. Here’s a quote: “. . . the economic era Americans just lived through was miraculous. And now it is over.”

The article was in The Atlantic, titled, “The Economist Who Knows the Miracle Is Over”. It describes Brad Delong’s obsession and his new book. “The miracle ended around 2010. . .”

The Atlantic describes Delong’s obsession, “He kept writing, for years, for decades, for so long that he ended up writing for roughly 5 percent of the time capitalism itself has existed.”

He’s been busy extrapolating!

There are other obsessive extrapolators. Some of your subscribers are seriously, constructively obsessive. There is hope!

[ go to the light, Carol Ann ]

Great comments. Probably should be a separate (free to read) article of some sort.

H, There is a “cost” to choosing a “normal” life that is likely too high a price for you to willingly pay. I say this based upon the tiny bit about your current and past life that you have chosen to explain to us.

“Constantly immersed in some kind of study or analysis every waking hour (that is not harming you or anyone else)” combined with over 14,000 people who think you are amazing- seems like you are well on your way to achieving “self actualization” as in Maslow’s hierarchy. Plus, I am guessing the “ego” portion of those needs is simultaneously being met. 🙂

+1

I remember reading an article a few years ago by Kevin Muir that mentioned a virus running rampant in China. That was before it had a name. I didn’t connect the dots and my portfolio paid the price. It was a lesson learned and a mistake I hope not to make again.

I don’t pay a professional to lose my money.

If I lose, it’s my fault.

So, I depend on “tiresome” pundits to inform me. To date, I’ve been ahead of the curve; up 16% and now my money is safely invested until such time that I’m comfortable with reinvesting it.

As I’ve said before, I’m not that smart, but I’m aware of what is going on in the world.

To me, that’s significantly more important than a company’s bottom line.

Mr. H:

I taught high school economics for a time. Despite that experience, I profess very little working knowledge about the intricacies of leveraged options, fx, and things like international monetary flows. (It was my job merely to teach the basics, and a master’s degree was not required.) I enjoy your careful dissection of daily economic events, your cynicism, and the sometimes stark extrapolations that you make as a result. It is an important counterbalance to the fluff and outright dearth of information I can find elsewhere, and it is why I subscribe to your report. Keep up the good work.