“Shortsighted.”

That, in a word, is what the Biden White House thought of OPEC+’s move to cut oil output by two million barrels per day. The decision, which was in the market (and at least partially in the price) prior to the official announcement, was viewed in Washington as the second slight in as many months.

On September 5, the alliance announced symbolic curbs for October, negating a token supply increase delivered under pressure from US officials keen to arrest rising gas prices in a politically sensitive year. The offsetting adjustments (100,000 barrels) were meaningless from a market perspective, but they were important in other ways.

The September reduction (agreed in August) was seen as a small concession to the US, while the quick reversal for October (agreed last month) was ostensibly aimed at addressing what Prince Abdulaziz bin Salman bemoaned as a “disconnect” between paper and physical markets. The prince’s lament for a broken market was self-serving, but it wasn’t wholly disingenuous. Liquidity has dried up and there are indeed structural concerns. Open interest in futures dropped to a seven-year low last month, for example, and large daily price swings are now the norm. Removing barrels is seen as a partial fix to the extent reduced supply reinvigorates an increasingly moribund market.

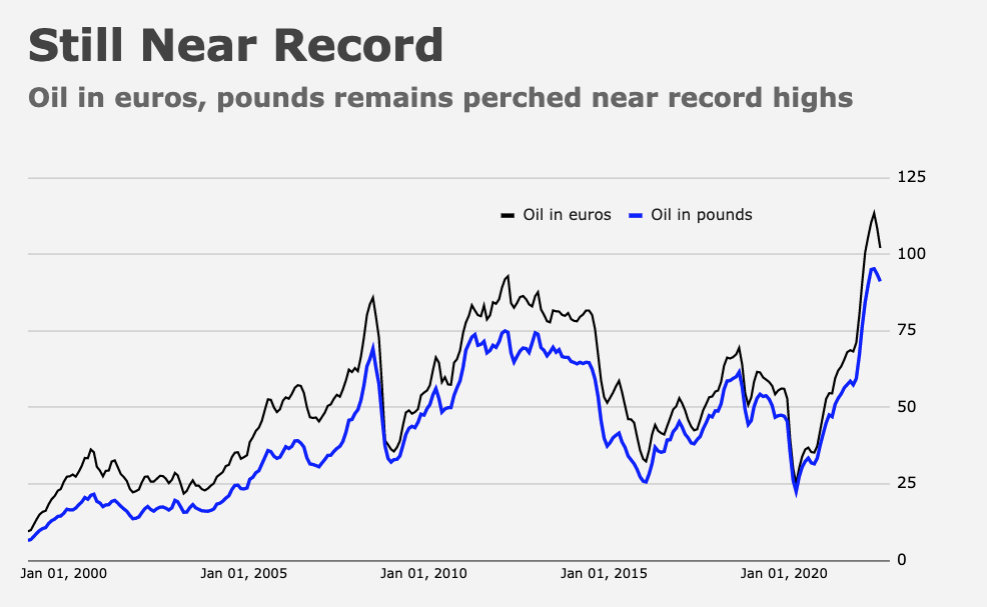

Of course, the drop in crude prices from this year’s nosebleed highs (figure below) isn’t just a market functioning issue. There are pervasive demand concerns tied to expectations for a global recession, and China’s quixotic battle with COVID isn’t helping. At the same time, the stronger dollar has undercut prices, even as severe weakness in the pound, euro and yen, have driven up import bills for America’s allies, who are the unfortunate recipients of exported US stagflation.

On Wednesday, OPEC cited “the uncertainty that surrounds the global economic and oil market outlooks” as well as “the need to enhance the long-term guidance for the oil market,” in explaining the two million barrel per day cut from August’s required production levels, starting next month. The cartel and its allies, including Russia, lauded their own market management efforts as a “successful approach” built on a commitment to being “proactive and preemptive.”

The in-person proceedings in Vienna featured a cameo from Alexander Novak, who Janet Yellen sanctioned last week, alongside Elvira Nabiullina. “With Novak set to appear in person, despite his recent inclusion on the US sanctions list, one can’t help but be reminded of Vienna’s Cold War past and wonder if there will be a Third Man overlay to [the] proceedings,” RBC’s Helima Croft wrote.

The gathering took place under the shadow of a looming price cap on Russian crude. Last month, Moscow was reportedly reluctant to countenance a production cut. The Kremlin, some observers said, was concerned about the signaling effect at a time when Vladimir Putin needs to preserve bargaining power with whatever buyers he can find. A production cut might signal demand concerns, thereby undermining his leverage. “This time, Moscow has made a push for a big reduction against the backdrop of the G-7 frantically working to finalize a price cap plan,” Croft went on to say.

The actual decline in physical supply from the announced cuts will be far less, likely on the order of one million barrels per day given production shortfalls versus quotas. And notwithstanding legitimate demand concerns, Chinese consumption will rebound as soon as Xi pivots on pandemic containment, assuming he ever does. Supplies are tight, and there’s scant evidence to suggest high prices have constrained demand. So, on a superficial read, the curbs are somewhat dubious.

It’s also notable that OPEC+ extended the Declaration of Cooperation until the end of next year. “The Riyadh-Moscow alliance, which started six years ago, is becoming a permanent axis, redrawing energy geopolitics,” Bloomberg’s Javier Blas wrote, calling that a “dangerous development for the future of energy security.” The timing of the move, he said, made the cut look like “a personal attack on Biden,” a perception “reinforced” by “the fact that OPEC+ hastily gathered in person in Vienna, rather than via video-conference as scheduled.”

It’s probably not a stretch to say the Biden administration is furious. In the same statement cited here at the outset, the administration called on energy companies to keep lowering gas prices, and said Biden would speak to lawmakers about “tools and authorities” to loosen OPEC’s grip on the market. I have a few modest suggestions in that regard:

- First, and most obviously, the US is energy self-sufficient when it wants to be. This shouldn’t be an issue in the first place. That’s a woefully simplistic version of a very complex story, but the overarching message is clear enough. The US doesn’t need the Saudis.

- Second, the Saudi riyal is pegged to the dollar. Nothing irritates an oppressed populace more than a currency crisis. And nothing scares a monarchy more than a restive populace. (You can make of that what you will.)

- Third, the Saudis need US security guarantees. The White House and Congress aren’t obliged by any divine dictate to provide them.

- Fourth, there are likewise no stone tablets that declare the US must accept Mohammed bin Salman’s farcical self-conferred Prime Minister designation, which grants him immunity in proceedings tied to the murder of Jamal Khashoggi.

- Fifth, Janet Yellen could sanction Mohammed bin Salman and the Saudi central bank. Trust me: US intelligence could put together a (long) list of OFAC-ready offenses if prompted.

To be clear, I’m not suggesting the implied policy actions are feasible (or advisable). Rather, the point is that if the White House is really as concerned about the situation as they claim to be, and if pretensions to pulling all available levers are anything more than nebulous bluster, there are levers to pull. Plenty of them.

“For the past several days, Biden’s senior-most energy, economic and foreign policy officials were enlisted to lobby their foreign counterparts in Middle Eastern allied countries including Kuwait, Saudi Arabia and the United Arab Emirates to vote against cutting oil production,” CNN reported, adding the following additional color:

Some of the draft talking points circulated by the White House to the Treasury Department on Monday that were obtained by CNN framed the prospect of a production cut as a “total disaster” and warned that it could be taken as a “hostile act.” “It’s important everyone is aware of just how high the stakes are,” said a US official of what was framed as a broad administration effort. The White House is “having a spasm and panicking,” another US official said, describing this latest administration effort as “taking the gloves off.”

Again, I’d note that the US is plainly not prepared to “take the gloves off.” If they were, there’s a veritable cornucopia of options. To recapitulate, the US could ramp up domestic production using any and all means, threaten to undermine the riyal peg, disavow all security agreements with the Kingdom formal or informal, ban weapons sales and refuse to recognize MBS’s status-based immunity in any and all legal proceedings tied to Khashoggi.

Before you write all of that off as extreme or deride it as a list of wholly unrealistic non-starters, consider that if CNN’s reporting is accurate, and unofficial talking points seen by Treasury framed a large production cut as a “hostile act,” then it’s not clear why the US wouldn’t be “hostile” in return.

But Washington won’t. Be hostile, I mean. Instead, the Biden administration will make a lot of noise in public, do a lot of panicking in private, consider export restrictions and, possibly, squander more of America’s oil reserves in a game of pre-midterm-election Whac-A-Mole with pump prices.

“We believe Washington’s response will absolutely require close watching,” RBC’s Croft went on to say, noting that while the bank does “see scope for product export restrictions in the event there’s a significant spike in retail gasoline prices,” a muted price reaction could instead see the Biden administration “seek to downplay the importance of this OPEC meeting and attempt to change the subject.”

As a quick reminder, Exxon and Chevron raked in a combined $29.5 billion in net income during the second quarter, a record haul. Saudi Aramco made $50 billion during the same three-month period. By itself.

{kind=link}

{kind=link}

The US could decide that Saudi’s increasing and active political closeness to Russia requires a review of military technology sales, mil-intel links, and security relationships. Hold up pending weapons deliveries, including spares and supplies. Pull back approved sales for re-review. Cut back assistance in operations, maintenance, etc. The Houthis might take the hint. I don’t think the US would need to pull very hard on the Saudi security blanket to make MBS, or his father, quite worried.

Domestic voters would like that (no-one likes the Saudis) and gives Biden a blame finger to point.

Just stop draining the SPR. That is ridiculous. The SPR has been reduced by 50%, it is now lower than commercial storage, commercial + SPR combined are seriously low.

Draining the SPR was a brilliant move. Not just for the damper it put on prices already but for the commitment it makes to oil producers. The eventual refill promises to make the US a buyer of last resort if the global economy does fall off a cliff.

With friends like MBS, who needs…well, you know the rest.

Maybe initially the US did not want to use up its own oil but would rather deplete mid eastern oil. However, with the move away from fossil fuels it seems likely the US will end up with billions of gallons of oil in the ground that will be worthless. It is very frustrating that we let the Saudis’ jerk us around when we have more than enough oil to see us through. It is even more irritating when you see the Russians pulling their strings.

A nuclear deal with Iran is also a possibility. That would unleash some supply. The Saudis better be careful- they could get burned by geopolitics as well as benefitting from it.

Iran is the enemy of Saudi Arabia and several other MidEast countries (proxy war in Yemen). Some of these countries are more “moderate” than others. And we can agree that “moderate” is a very relative term in the geopolitics of the Middle East. By our flirting with the mullahs in Iran (who are currently facing a rebellion of young ladies in high-school)…..perhaps it shouldn’t be a surprise that countries that have a history of partnering with US for decades, and are enemies of Iran …aren’t feeling too sympathetic.

What is trully sad is that because of our broken poltical system we can’t establish a long term energy policy. If we did what the UK does and subsidize solar panels for businesses and homes, as well as heat pumps 100% we could be on our way to true energy independence. There is also Solar thermal which could be put in deserts and other arid unoccupied land. We currently have 93 operational nuclear plants, if our country built another 100 across the country then we could meet 80% of our nations energy needs so we couldn’t get rid of all the natural gas electric plants but we could get rid of a significant portion of them.

The US makes about as much oil as it consumes. US production is currently near all time highs, and should achieve new all time highs in 2023.

2017: 3,415,257,000 Barrels of Crude Oil

2018: 3,993,288,000 Barrels of Crude Oil

2019: 4,485,635,000 Barrels of Crude Oil

2020: 4,129,563,000 Barrels of Crude Oil

2021: 4,082,478,000 Barrels of Crude Oil

U.S. crude oil production in our forecast averages 11.8 million barrels per day (b/d) in 2022 and 12.6 million b/d in 2023, which would set a record for the most U.S. crude oil production during a year. The current record is 12.3 million b/d, set in 2019.

https://www.eia.gov/outlooks/steo/report/us_oil.php