Mortgage rates in the US rose above 6% last week for the first time since November of 2008.

The 13bps jump from the prior week marked the fourth consecutive weekly increase, and the fifth in six (figure on left, below).

In July, as rates fell alongside a retreat in Treasury yields and a rally in US stocks, some observers who should’ve known better suggested we’d seen the highs. We hadn’t. And probably still haven’t.

Housing market aficionados are, in my experience, among the most biased market observers you’ll ever come across. They’re not ill-intentioned. They’re just hopeless Pollyannas who habitually lean on old saws and the self-evident fact that generally speaking, it’s never a “bad” time to own a piece of a land with a sturdy house on it. While unequivocally true, that latter notion doesn’t necessarily mean it’s always a “good” time to buy.

Rates are up almost 90bps since mid-August (figure on the right, above). That portends another slowdown in activity.

Part and parcel of the Fed’s efforts to tighten financial conditions and bring down inflation is a deliberate attempt to cool the housing market. Officials have publicly referenced a slowdown in activity across virtually all housing metrics while suggesting the effects of rate hikes are starting to manifest in the economy.

And yet, while stock prices have fallen dramatically, reducing the value of household equities by almost $11 trillion during the first half of 2022, property values rose by more than $3 trillion over the same period (figure below).

Q2’s $1.4 trillion rise was the seventh consecutive quarterly gain of at least $1 trillion. Arguably (I actually don’t think it’s a debate, but we can pretend), the Fed would like to see prices fall. Maybe even a lot.

Although the pace of home price appreciation has slowed sharply, almost no one currently predicts a collapse, even if many are now belatedly on board with the idea that prices may decline nationwide, not just in select locales.

My contention has long been that the US is sitting atop a housing glut without realizing it — that the country has too many homes. That’s still a (wildly) out-of-consensus view, but maybe it shouldn’t be. Last year, you’d have been called a fool had you suggested America’s largest retailers had too much inventory. In hindsight (where that means a scant nine months later, after every major retailer in the country cited massive inventory overhangs in cutting forecasts amid collapsing demand for discretionary goods) it seems so obvious.

Quite a bit of that excess “stuff” will have to be discounted if retailers hope to move it at a time when the combination of goods-to-services switching and the financial imperative of diverting more income to necessities will reduce household demand for discretionary purchases of consumer products.

The situation in housing is, I’d argue, conceptually similar. Mortgage rates that are double what they were late last year combined with record high property prices may leave a sizable share of newly-built homes similarly redundant, for example. Allow me to recycle some language from a July article.

Notwithstanding the often sage, real-time advice we receive from our “fight or flight” instinct in times of peril, panic isn’t conducive to good decision making. Employers and homebuilders were in a state of panic for most of 2021, a year defined by voracious demand and a dearth of supply. In the event the economy slows materially, it seems plausible to suggest that many of the decisions made last year, from hiring to stocking to building, will be exposed for exactly what they were: Haphazard judgment calls born of hysteria and perceived necessity rather than careful planning and prudent execution.

It’s with that in mind that I wanted to (re)highlight the anomalous increase in months’ supply. In a recent note, Morgan Stanley flagged the two-month leap in supply over just eight months as a historical outlier. At issue is the juxtaposition (I’d be more inclined to call it “tension”) between what, under virtually any other circumstances, would be an alarming increase in inventory and an optical (i.e., ostensible) shortage of homes.

As Morgan wrote, supply increases like that seen since the beginning of the year are exceedingly rare, and when they do happen, they’re naturally followed by falling prices a year later (figures above).

“In fact, in the 34 instances in which months of supply increased by more than one month over any six-month period, annual price growth was negative 12 months forward 88% of the time,” the bank said.

As for cases when months’ supply has risen by more than two over a six-month period, prices have fallen 12 months later 100% of the time.

And yet, due to a number of factors (including demographics and, most importantly, the notion that overall, the country suffers from a dearth of homes no matter what the trend in a supply metric calculated using the current sales pace says), most observers expect prices to rise, albeit far more modestly going forward.

But what about all the construction? What about all the panicked building? What about all of those unfinished neighborhoods where builders assumed endless demand for new homes? What about all the (greedy) people who waited one (or two or three) months too long to list their house hoping to time the exact top? How is any of that going to sell with mortgage rates at 6% without markedly lower prices?

Spoiler alert: It’s not. Going to sell without lower prices, I mean. Because it can’t. People can’t afford what they can’t afford. This debate isn’t a debate anymore. It’s a tautology.

You can draw your own conclusions. If home prices do drop sharply, it’ll be too late for the Fed.

{kind=link}

When you say, ‘it’ll be too late for the Fed”, are you saying that no amount of easing will help the resultant contraction? Given The geopolitical and economic realities, is the dynamic that followed and became embedded since the GFC about to be broken? I looked at the referenced graph.

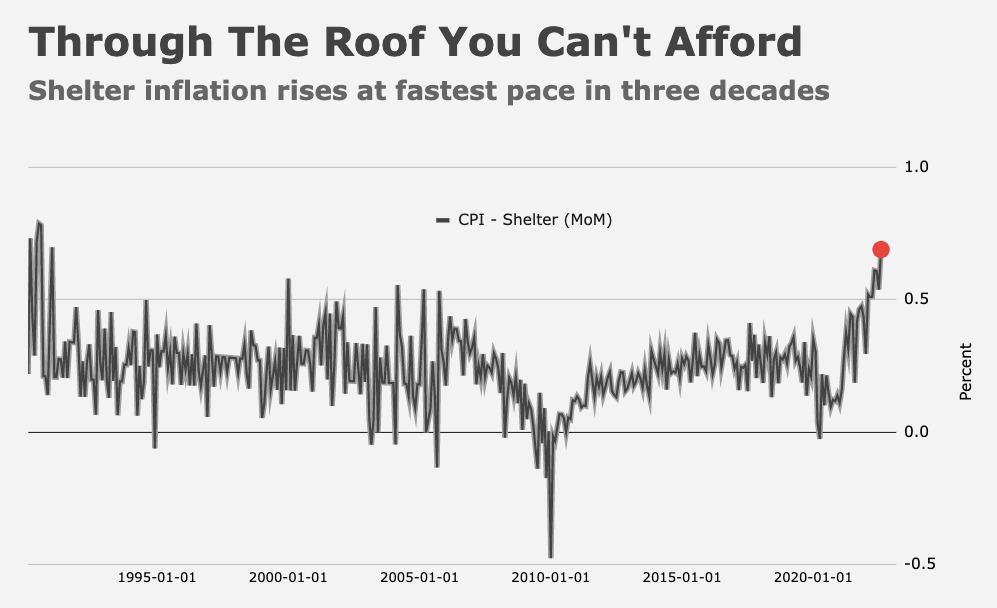

No, I’m saying when you engineer a housing bonanza that turns everybody with a $500k home into a nominal millionaire over an 18-month period (which is what the Fed did post-pandemic), shelter inflation is going to go through the roof on a 9- to 12-month lag as sure as night follows day. And by the time you (where, in this case, “you” means the Fed) realize what’s going on, it’s going to be too late to do anything about it.

But wait, there’s more. Because everybody with a $500k home now has a $900k home and thereby thinks they’re genuinely well-off (as opposed to just “reasonably secure”), and because everyone with a $750k home now has a $1.2 million home and thereby thinks they’re actually rich (as opposed to just “genuinely well-off”), a lot of people are going to retire, reducing the size of the labor pool, which in turn increases competition for increasingly scarce workers, thereby driving up wages, perpetuating the wage-price spiral.

Variable rate home equity’s will come into place soon

If we want young people to form households then we need those prices to come down. I could not afford my house today that I bought for cash almost 12 years ago. A 20% down payment would be slightly more than I paid for the home, and the bank would probably never approve the mortgage based on my income. I don’t know how my nieces will ever buy a home.

I am not as bearish as h, but nominal prices need to adjust moderately now. Where I agree wholeheartedly with h is real inflation adjusted prices. They need to come down a lot. They will over the next 5 years. In areas where growth is strong in the next 5 years the adjustment will be less. In slow growth areas it will be greater. You can probably bet that nominal prices will be flattish in most markets over the next 5 years.

Having finished reading your last six posts, I would opine they all should have been framed in black. Normally, Halloween is at the end of October, but this year it may come much earlier.

My wife “virtually” shops for homes on-line all of the time. She looks at homes all over the country, but mostly on the West Coast, where demand and prices are usually high. For the first time in two-years, she is seeing properties sit for more than two-weeks. She is also seeing the number of three bedroom, two bathroom homes increase–particularly in non-metropolitan areas–and she is seeing price reductions of $25,000 on many of those homes. This was even before mortgage rates reached 6%, and they are likely to go even higher. For much of the pandemic, real estate prices seemed to mirror the rise in tech stocks, which I myself found rather unsettling.

I put my home and property on the market in July. We have continuously dropped the price. However, the list price is still a nice premium. Praying (not literally of course) I can get of here before the Winter.

Can’t wait to feel genuinely well off. Though that happened when the pandemic enabled firms hire remote software consultants.