I’ve mentioned the prospect of a reprieve for beleaguered equities in the near-term.

Sentiment is obviously subdued, bear markets abound and generally speaking, positioning is light. Much depends on Fed rhetoric, which is in turn a function of the incoming data, virtually all of which now presents event risk. Further evidence of inflation’s persistence is conducive to policy panic, as is jobs data showing workers remain scarce and demand for labor robust. At the same time, figures which suggest growth momentum continues to slip will be interpreted as confirmatory for the recession narrative.

The case for a meaningful bear market rally (assuming it makes sense to use the adjective “meaningful” to describe fleeting risk asset reprieves which, by their very nature, aren’t meaningful) rests on the notion, however tenuous, that markets are set to drift through a kind of purgatory for several weeks, during which risk assets become mostly numb to Fed messaging that doesn’t deviate from what’s already expected and priced — namely, another 75bps rate hike in July and 50bps in September.

To be sure, pinpointing “peak hawkishness” has been a fool’s errand in 2022. I’ve tried. And just like everyone else, I’ve met with little success. That said, it’s worth noting that incremental hawkishness from here probably has to manifest in a higher terminal rate or recalibrated expectations for the cycle as a whole. I’ve been as hyperbolic as anyone in lamenting the disastrous nature of the incoming inflation data, but it would take a truly harrowing turn to compel the Fed to consider a 100bps increment next month and/or an inter-meeting, emergency move before the September meeting. If it comes to that, all bets are well and truly off. Assuming it’s mathematically possible for US inflation to accelerate higher than, say, 10% or 12% between now and September, such a scenario is virtually impossible to hedge in equities outside of the binary: You either have crash protection or you don’t. On the geopolitical front, any kind of nightmare escalation in Ukraine wouldn’t be met with a hawkish monetary policy response.

My sense, then, is that equities can stabilize, or even rally, locally, pending the next shoe to drop. That shoe is Q2 earnings, when the Street will almost surely be compelled to begrudgingly accept the reality of a downshift in corporate profit growth. If the odds of a recession rise materially between now and then, it’s possible consensus will be forced to recalibrate EPS expectations to incorporate a cascade of downgrades to house GDP forecasts.

When I glance at the figure (below) I see two things: Declining corporate confidence and corporate confidence that’s still far too high given margin headwinds and waning economic momentum.

As Deutsche Bank’s Binky Chadha and Parag Thatte wrote, in a recent note, weakening corporate confidence may well prompt “further cuts to guidance and therefore consensus estimates.”

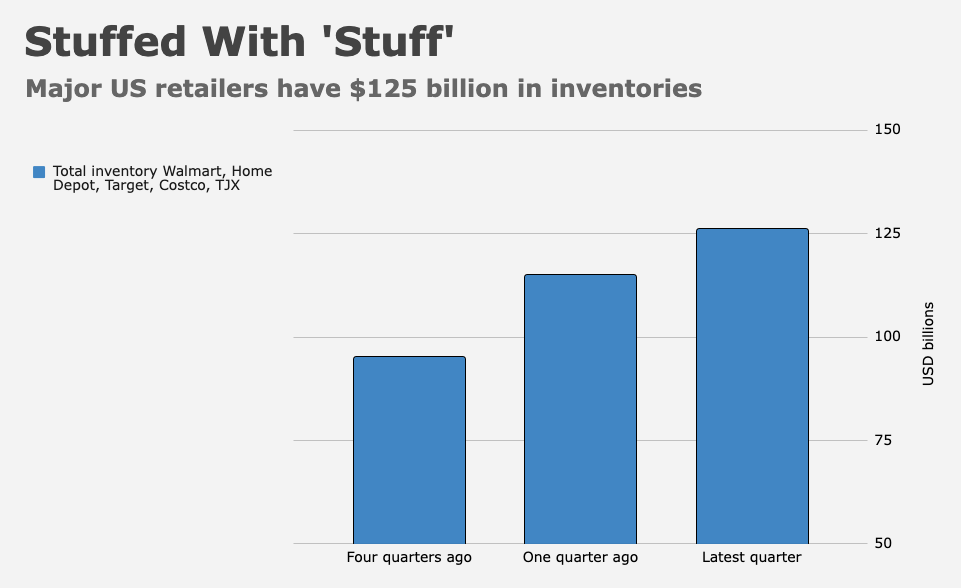

Every week investors are greeted with news of hiring freezes, layoffs, guidedowns or some other canary indicative of C-suite angst. Some of America’s most recognizable executives have resorted to poorly articulated metaphors (Jamie Dimon’s road hurricane) and comic book clichés (Elon Musk’s “I’ve got a bad feeling about this“) in warning of impending doom. Meanwhile, the country’s largest retailers inadvertently saddled themselves with $125 billion in inventory, some of which will need to be discounted to lure stretched consumers who, according to some of the very same retailers, are shunning discretionary purchases in favor of necessities as inflation bites.

Analysts can’t ignore all of this forever. It’s becoming more obvious virtually by the day that corporate America over-earned, over-ordered and over-compensated during a period of artificially elevated demand. The idea that lost goods demand will simply find its way to services with no meaningful “slippage” is laughable at a time when inflation has broadened out to impact every corner of American life.

The good news is, the market is wise to this even if analysts aren’t. The figure on the left (below), shows stocks have priced in “a much sharper decline in earnings,” as Deutsche’s Chadha put it.

The figure on the right (above) shows revisions are “quite muted” (to employ Chadha’s euphemism) compared to the rapidity of the selloff.

Forward estimates did fall during Q1 earnings season, and if you exclude energy and companies that suffered the most during the pandemic (COVID “losers,” as it were) the decline in consensus quarterly EPS compared to the beginning of the prior reporting season was almost double the 10-year median.

But, as Chadha and Thatte went on to write, netting the Q1 aggregate beat with downgrades for the remainder of 2022’s quarters leaves the annual estimate mostly flat, while 2023 estimates are down only slightly. Neither of those projected outcomes are commensurate with the scope of the equity drawdown, nor do they seem consistent with corporate rhetoric, hiring freezes and so on.

All in all, consensus (still) points to earnings growth of around 10% in 2022 and a repeat of that in 2023. That seems pretty optimistic considering the Fed intends to deliver more than ~200bps of additional tightening over that period and also considering the US economy has already logged one quarterly contraction while the Fed’s own real-time GDP tracker currently pegs growth at 0% for Q2.

As Chadha and Thatte remarked, expectations for ongoing profit growth despite gale-force headwinds to profitability come on top of the rapid acceleration post-pandemic. If consensus is right, the overshoot versus the trend would approach record extremes (figure on the right, below).

“S&P 500 earnings are already 20% above trend,” Chadha wrote. “Consensus estimates will take them nearly 30% above, approaching the peak seen in 2007.”

Over the weekend, I made a rare pilgrimage to the “nearest” Walmart. The trip requires traversing three islands, and braving a sweltering hot coastal highway littered with dead armadillos and mined with speed traps. It’s a long drive in the off season. During vacation season, it’s a veritable odyssey.

An aisle in the stationery section was blocked by empty merchandise boxes with a stamp on the side instructing employees not to discard them. A long self-checkout line moved faster than I thought it would. Consumers, it would appear, are adapting to the circumstances, becoming more adept at scanning and bagging their own items. Only there weren’t any bags. “All we have are those small ones by the candy,” the employee supervising the self-checkout explained. “We have these boxes, though. They’re 50 cents each.”

{kind=link}

I heard through my work that we are in the midst of a cardboard shortage. Laptops we had ordered were on backorder for months, not because the equipment was unavailable, but because there were no boxes to ship them in.

A lot of our problems now are neither monetary or fiscal… A man with a hammer sees nails everywhere….

Ukraine and Russia are major suppliers of neon gas and palladium, vital elements in chip and computer manufaturing…

I’ve mentioned this before, but using 2023 consensus estimates, the aggregate and market cap-weighted SP500 will by 2023 have grown revenue by 30% and EBIT margins by 400bp since 2019. That looks like “over-earning”, and in my opinion it is very unlikely to play out that way.

The market is sniffing out the coming estimate cuts for 2023, even if analysts aren’t there yet. My first cut suggests that a return to normalized i.e. 2019 margins implies 2023 aggregate EBIT estimates are 18% too high, and adding a topline slowdown in 2022+23 implies larger EBIT estimate cuts.

The SP500’s -23% decline to date barely discounts the likely estimate cuts, without even including the multiple contraction implied by slower growth, estimate cuts, and rising rates.

There will surely be some bear market rallies on the way to the SP500’s final trough, but I don’t think they should matter much except to very short-term traders.

My bottoms-up SP500 model keeps pointing at fair value between 3200 and 3400, and prices typically overshoot FV.

I had thought the sort-of-optimistic scenario was that rapidly declining inflation or rapidly deteriorating employment allows or forces the Fed to prematurely stop its tightening and shift to easing. With inflation unrelenting, jobs still very strong, and the default rate hike 75bp, that seems less likely. The other optimistic scenario, an end to the war and associated sanctions, looks not imminent.

I am planning for SP500 to get to the low 3000s this summer.

And do you have a parallel analysis/prediction for IWM (Russell 2000)?

No.

About 1/3 of R2G companies have negative earnings, and a large portion don’t have consensus estimates past 2024, so a rollup of company PE or DCF valuations to an aggregate conclusion doesn’t make sense. Or, at least, would require too many assumptions and interpolations.

As a practical matter, there’s no need (that I can think of) to have a fair value for R2G or even to try to figure out when R2G will trough.

Small cap won’t bottom until large cap does, so just work on figuring out the SP500.

When equities do bottom, pretty likely that many of best opportunities will be in small cap. But that’s individual company work not index work.

Thanks!