“It’s a ‘no harm, no foul’ kinda thing,” I told someone last week, while explaining the rationale for orchestrating a controlled demolition of what many believe are twin bubbles in America’s equity and housing markets.

Monetary largesse in the aftermath of the pandemic facilitated one the most spectacular wealth creation events in modern history for those fortunate enough to own stocks and a home.

Dramatic gains in the value of US real estate and equities were largely responsible for a $40 trillion cumulative increase in household wealth (figure below).

Those gains didn’t accrue equally. Far from it. By definition, you needed to own a home and stocks to participate. The more homes you owned, and the larger your stock portfolio, the better you did.

Of course, stocks are overwhelmingly concentrated in the hands of the richest Americans and a sizable percentage of US “households” aren’t really “households” because they have no house. Indeed, the surge in property prices put the dream of home ownership even further out of reach for many low- and even middle-income Americans.

At the same time, surging inflation disproportionately affected the same lower- and middle-income Americans who were underrepresented in the housing boom and stock bonanza. The implication: The post-pandemic environment was defined by one of the largest transfers of wealth in history, as generationally high inflation eroded incomes for everyday people while ballooning the fortunes of the richest members of society.

The figure (below) shows that as of December 2021, the entire American middle class owned just 10.5% of all corporate equities and mutual fund shares. The top 1% of Americans owned 54%.

Do note that absent a rebalancing, this dynamic will only get more pronounced. Unequal initial distributions are conducive to exponential (not linear) outcomes.

All of this is supremely ironic. The Fed justified the retention of a policy bent conducive to asset price inflation by reference to the necessity of ensuring the people who benefit least from higher asset prices were able to find work.

Now, in yet another paradox, the Fed’s efforts to rescue workers from the inflation they (the Fed) helped create, are set to disproportionately impact the least well-off members of society who, as the old adage goes, just can’t seem to catch a break.

Neel Kashkari acknowledged as much on Monday. “It’s the lowest-income Americans who are most punished by these climbing prices, and yet your policy tools to tamp down inflation most directly affect those lowest-income Americans as well, either by raising the cost to get a mortgage … or if we have to do so much that the economy [falls] into recession,” he told CNBC. “It’s their jobs that are most likely put at risk,” he added.

Let’s walk through this one more time, because it’s as important as it is tragic. The Fed, in the name of rescuing lower- and middle-income Americans from the highest unemployment since the Great Depression, adopted a policy stance they knew would inflate the value of assets concentrated in the hands of the wealthy on the assumption that, consistent with the post-financial crisis experience, real-economy inflation wouldn’t accelerate. But it did.

So, the explosive wealth gains enjoyed by the rich were set against a rapid erosion of purchasing power and real wage growth among the poor and middle-class.

Real wages and salaries of private industry workers are being eroded at the fastest pace in 40 years (figure above).

In order to correct the situation, the Fed is now poised to rapidly tighten policy, an endeavor which, in a perfect world, would result in sharply lower stock prices, slightly lower home prices, much lower consumer prices and, ultimately, a more equitable economic conjuncture in which the wealthy effectively give back some of their post-pandemic gains in order to “fund” a reduction in inflation for low- and middle-income Americans.

However, as Kashkari admitted on live television Monday, that probably isn’t how things are going to work out. In reality, the same low- and middle-income Americans who funded (through higher consumer prices) the epochal explosion of wealth enjoyed by the rich, will now be forced to fund their own rescue from the scourge of high inflation.

It’s not, as I euphemistically (and, I’d add, innocently) suggested last week, a “‘no harm, no foul’ kinda thing.” The rich will still be rich even if stocks and real estate prices plunge. The poor (and the relatively poor) won’t just remain poor, but will in fact get poorer because the only thing more insulting than getting a pay “raise” that’s actually a pay cut when adjusted for inflation, is getting fired during a recession engineered in the name of fighting that same inflation.

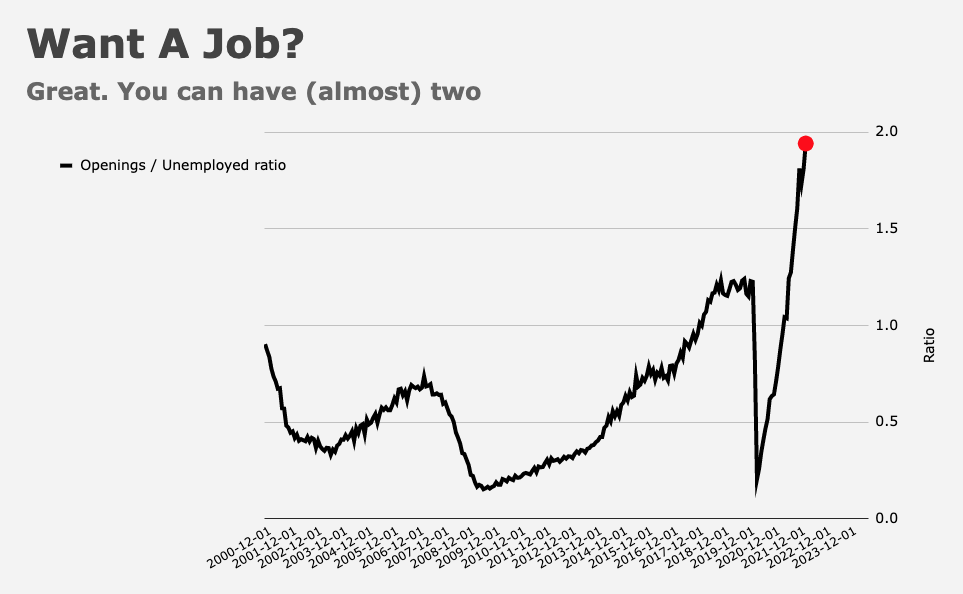

There’s a silver lining, though. As one astute reader pointed out recently, the ratio of job openings to Americans officially counted as unemployed is now nearly 2:1. That, the reader darkly quipped, means “we get the first one million jobs losses for free.”

{kind=link}

1 million jobs for free and wage suppression.

When COVID first hit, I was on a Zoom call with a couple of guys and I wondered out loud what the financial impact would be. One of the guys on the call said, “The same as always . . . the rich will get richer and the poor will get poorer.”

And there you have it.

Spot on

I’m sure sure what Kashkari is talking about when he says “… directly affect those lowest-income Americans as well, either by raising the cost to get a mortgage …”. Since when have the lowest -income Americans ever been able to afford home ownership, regardless of Fed policy? His comments are nothing more than pseudo empathy for millions of people who have been and will continue to be lip serviced by the plutocracy that is our government.

How true and I can’t for the life of me see a mechanism for changing it. Even the revolutions of days gone by seem impossible.

I’m no fan of Steve Bannon. That said, I read an old interview this weekend that you might find informative. Bottom line, the fuse is lit and everyone knows it. We just don’t know how long it is or the resulting changes. The URL is https://www.pbs.org/wgbh/frontline/interview/steve-bannon-3/ if you care to check it out.

Which will happen first: 1) the “Fed put” gets triggered at where-ever it is, or 2) the economy sheds >1MM job openings?

I think the US economy has a long way to slow before ordinary workers broadly see net permanent job losses.

Granted, some ordinary workers are seeing real wages decline -5% due to inflation. Others are seeing substantial increases. People don’t hop jobs for minor wage boosts, and the ones moving from unemployed to employed are seeing +100% real wage increases (“100%” is expository, not mathematically accurate). The biggest pain in a recession is when one moves from employed to unemployed with real wage -100%, and as long as job openings-to-unemployed stays elevated, mercifully few Americans will have to suffer that.

I’m not trying to make light of the suffering of small business owners, retirees on fixed incomes, soon-to-be-unemployed Wall Streeters, and workers in circumstances that make taking advantage of those job openings very difficult (older, not geo mobile, etc).

My guess is that we’ll see “1” before we see “2”.

I wonder if the angst towards vaccines and forced shutdowns would have been compounded if we let the recession happen when many were forced to stay at home or unproductively work from home.

We will see how trillions of inflation and forced bubbles will add to the mix and whether they could or would want to keep the put in.

Re-reading my comment, I realized I failed to include scenario 3) the economy adds >1MM job seekers. Which is the other way the economy could reach the Fed’s (other) put level.

I don’t know what to think about this scenario. Many reasons for workers to remain unemployed are rapidly diminishing: stimulus checks, buoyant portfolios, Covid fear, closed schools, fat savings – all in the past or soon to be. Other reasons are harder to assess: new perspective on life’s meaning, and so on. Yet other reasons are quasi-permanent: of the 1MM US Covid deaths, at least a quarter were working-age, and for every death from Covid there are probably multiple disabilities from long Covid.

If anyone has links to good analyses and forecasts of the labor force shortage, I’d be interested. The implicit assumption among investors and economists seems to be that the job supply-demand gap will be closed, if it is closed, by constricting demand, a negative outcome. direction. If that gap were to be closed by expanding supply, that would be a positive outcome.

Someone in the comments a few days ago posted a link to a WSJ article looking at a few microeconomic case studies of low wage workers who had engaged in job hopping. It was eye-opening (though more anecdotal than data-driven). Basically, employers in the past few years have instituted a system of hiring more workers than they can employ full-time, deliberately, so as to maintain workforce flexibility and to avoid paying anybody the benefits owed to a full-time worker. So in spite of the availability of jobs, many workers struggle to put together 40 hours a week, so they leave for another employer. I also know (first-hand and second-hand) that the use of screening software and hiring criteria has made it really difficult to hire people, even though the job openings are there and the candidates are there. If you can’t get by the screening software, you don’t get hired, and the job stays open. In years past, employers might have lowered their criteria, e.g. stop requiring a college degree for administrative positions, or taking a chance on someone who doesn’t quite meet the ideal profile. But it seems that this kind of flexibility is not easy to find these days. On the other hand, if companies are getting by without actually hiring to fill the open positions that they supposedly have, then it will be pretty easy to just cut those positions when things start going south. I guess we’ll see.

Joey makes a great point there at the end. I too wonder how quickly and by how much that much cited mega-cushion of job openings will shrink in the face of a slowdown.

I normally attribute little forecast value to sector rotations in the stock market, assuming much or most is driven by the day’s prime broker talking points. But recent declines in the transport and chip stocks presaged actual weakness in demand in those sectors.

Yesterday the heavy losses in many travel-related stocks made me wonder if we are starting to see a ratcheting down of expectations for travel & leisure spending. With gasoline, food and now rental costs taking up more and more of consumer budgets, spending on less vital things will often be cut. Is the widely assumed pivot from spending on goods to services being called into question?

H

Very nice piece. This kind of post is why I will keep sending you my gelt. Thanks for the insights.

Sadly, those same poor people will vote for politicians whose solution will be more tax cuts for “job creators.”

And cuts in the social safety nets those poor people will need.

Which means the government will have to ensure a steady supply of booze, pot and porn, just like the USSR used long lines and vodka to keep the masses from storming the castle walls.

We’re placing too much emphasis on what the Fed has done. Politics have effectively deprived the technocrats at the Fed from more nuanced tools, like applying different interest rates to different lenders (people vs. banks), supporting MBS differently based on the value of the mortgages lumped together, selecting what types of bonds to buy (educational loans, municipal bonds, small business loans, etc.).

It’s pretty much by design that QE helps the rich and QT harms the poor. Of course that if you get to design the game, you tilt it in your favor: tails you lose, heads I win.

Can someone please help me understand better the “lesser of two evils”: does quantitative easing (the recently invented bazooka) or lowering interest rates more help the common person?

(I’m not trying to pick absolutes and say either/or since QE for keeping credit markets moving is a given)

I think it is importnat to remember that countries like Germany or Sweden have more monetary and fiscal options because they have a safety net. We are ashamed to have a safety net and therefore 80 percent of the population is in a lose lose situation…This citizens united crap just makes a way out harder to find…..