Risk sentiment was very poor to start another pivotal week.

Trade data for April betrayed a sharp slowdown in Chinese exports, and the yuan plunged against the dollar, extending a rapid bout of depreciation.

Global equities are on the brink of a bear market. The MSCI All-Country World Index is down more than 15% from highs hit late last year (figure below).

Bearish sentiment is pervasive. And for good reason. It’s difficult to conjure a compelling bull case for equities at a time when the threat of stagflation hangs over the global economy like stale cigarette smoke and the Fed’s hands are tied by generationally high inflation in the US.

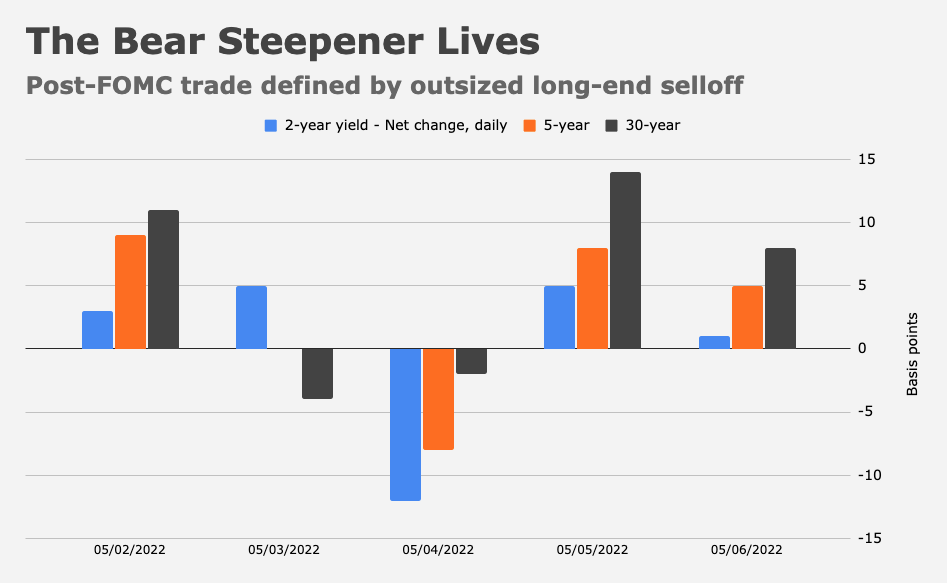

Paradoxically, it may take an even more hawkish Fed to calm markets. Strategists spent quite a bit of time opining on the bear steepener in US rates that unfolded on Thursday and Friday. One explanation is that the market isn’t convinced the Fed is prepared to be sufficiently aggressive.

“Yes, central banks are on course to hike rates 251 times in 2022 and yes, QT starts in the second half, but yields and volatility will rise until the Fed and central banks are ahead of the curve,” BofA’s Michael Hartnett said. “They’re quivering at the thought of QT after buying $23 trillion since Lehman, and $11 trillion since COVID,” he continued. “Little wonder bond vigilantes are back to trading the ‘end of central bank credibility’ [leading to] entrenched volatility.”

Of course, higher US yields and volatile markets invite dollar strength. “It’s a post-2002 high for the dollar index as risk aversion sweeps across markets,” SocGen’s Kit Juckes wrote Monday. “Last week’s CFTC data shows the net dollar long growing, but still relatively modest,” he added, flagging a still sizable yen short, a renewed net short euro position and a “really moving” sterling short which Juckes said “remains the market’s favorite way to express a long dollar position, as the UK economy runs into a brick wall, the government is unpopular and the threat of calls for a new Scottish referendum and more trouble over the Northern Ireland protocol threaten to become market factors.”

Europe is facing possible severe stagflation, the Bank of England adopted a very dire outlook last week and Japan is committed to yield-curve control, which exacerbated the BoJ-Fed policy divergence, resulting in a record losing streak for the yen in April.

DXY is nearly 8% higher since Russia invaded Ukraine, and 16% higher over the past 12 months alone (figure below). “No G10 currency is up on the dollar since the beginning of the year [and] dollar shorts are underwater,” BNY Mellon’s John Velis said Monday.

“We think this period of dollar strength will endure, in large part based on our Fed view,” Velis added, suggesting the forward curve still hasn’t priced in a high enough terminal rate. “An eventual repricing higher of those rates should continue to support the dollar,” he remarked.

Expectations for ongoing Fed tightening (and the possibility that Jerome Powell may need to escalate things further) have pushed up US real rates, another boon to the greenback and a severe impediment for risk assets.

That could become a self-fulfilling prophecy, especially if it starts to undercut EMs. The Bloomberg Dollar Index sits at a two-year high (figure below).

Fed officials will have ample opportunity to talk things back this week. A bevy of scheduled speaking engagements will be parsed relentlessly for tradable information.

Alas, it seems likely policymakers will skew hawkish, possibly to the further detriment of risk assets. And that underscores the “damned if you do, damned if you don’t” situation stocks currently face. If the Fed is seen as unwilling to do what’s necessary to curtail demand and force inflation lower, the bond vigilantes may push the envelope at the long-end to the chagrin of equities (a la Thursday/Friday’s trade). If, on the other hand, the Fed indicates a willingness to keep all options open, including 75bps hike increments, that could help anchor long-end yields and prevent a disorderly bear steepener, but it’d likely put more upward pressure on real rates, pressuring stocks further. Note that stocks’ “damned if you do, damned if you don’t” predicament is a “heads I win, tails you lose” setup for the dollar.

This could reverse course simply because the trade is now stretched, or because Fed pricing finally reaches a plateau. “The greenback may be fast approaching the upper reaches of its valuations in the near-term,” Bloomberg’s Ven Ram suggested.

Here’s hoping. Because, again, inexorable dollar strength is a de facto liquidity withdrawal for the entire world. It’s bearish for nearly everything, and that feeds on itself because, as markets relearn every now and then, when push comes to absolute shove, nobody wants anything other than US dollars.

{kind=link}

Well stated and illustrated. The US dollar’s impending demise keeps being misforecasted.

Everything sounds compelling when things are going well — profitless software stocks with “bright” futures, streaming services burning through cash to create a never-ending menu of TV shows, expensive WiFi-enabled exercise bikes, social networks-turned VR headset makers, 90s nostalgia stocks, virtual Chuck E. Cheese tokens and even $500,000 jpegs of monkeys wearing sweaters.

When things start falling apart in earnest, the strength of the dollar’s shared myth reasserts itself. NFTs and crypto are an extreme example, but it’s the same dynamic at work across all assets in a real pinch: No matter how much I like my NFTs or my Bitcoin or my Netflix shares or my GameStop or my yen or my euros or my pesos or my stamps or my baseball cards or my comic books or even my gold coins, I can’t be sure that my proverbial “neighbors” will like them as much as me, let alone accept them as payment for goods and services. As things stand in 2022 (and this could change over time, but no time soon), I can be reasonably sure that no matter where I am in the world or what I’m trying to do, whoever I’m trying to transact with will accept a shoebox full of authentic US dollars.

The only exception to that is an honest-to-God Mad Max scenario. If that’s your base case, then sure, you want commodities — real commodities. Physical ones. And what I’d note is that none of the people touting commodities right now are actually buying commodities. They’re buying paper contracts that reference commodities with no intention to take delivery. Nobody shouting about the merits of “investing” in commodities on Twitter is prepared to store a thousand barrels of oil in their basement. What they mean by “investing” in commodities is betting on higher prices. And what are commodities priced in? Exactly.

Short of Mad Max scenario, people will also take Euros and Yens. Maybe a slightly bigger discount than USD but those currencies are still backed by a powerful polity and going nowhere fast. The advantage of the dollar is to be wider spread thanks to dominating intl’ trade for 75 years, not because we believe in the dollar myth harder than we believe in the Euro myth (much as I like Harari too and find his take on the social contract fascinating)

The standard for connecting what I value and others is indeed in dollars for most.

I don’t know if I’d want the current brexit, food and energy uncertainties on top of armed conflict that comes with the euro.

Well, I’d be happy to buy any Euro you might have and give you Dollars instead at the prevailing exchange rate with… let’s say a 15% discount?

I bet you won’t take that deal…

A strong $ should make bond bears cautious. If the $ continues to appreciate, the likelihood of a financial accident becomes greater and likely. A financial accident augurs for lower rates not higher ones.

I find myself thinking of putting at least some of my cash into commodities such as solar panels, battery storage, freezers, bikes, freeze dried vacuum packed food, farmable land, Teslas, random manually operated tools and extras clothing these days. Have lost my belief that the nest egg we’ve worked so hard to accumulate will retain its value, even in dollars, five to ten years from now.

Why not, Babe-in-woods? Your ideas make perfect sense to the extent they align with your wishes and needs.

I’m somewhat aged. Forty years ago, I reckoned a man like me would be hanging up his spikes. But today I have no intention of hanging up anything.

Aging shows me every day what a short one-way street I’m traveling on. And it keeps getting shorter.

Not to be fatalistic at all. I do not take excessive risk, and I’m grateful to have resources that I can invest. There is always some risk. All I can do is take intelligent risks when buying. But my desire is to persist and grow within this fabulous capitalistic system in which we thrive.

On the other side of the world the Chinese throw cold water on the impulses and appetites of their own people. They express hubris and arrogance, thinking they know better than the wishes of their own people. Shades of Vladimir Putin!

I’ve rotated recently into small-cap growth technology and financials, including some buys I made today after the bottom fell out this morning. That’s just my speed. I’m not in a hurry and never have been. I could live another 30 years, or not. The proposition of owning a piece of American capitalism through stocks gives me a lot of pleasure. I’m not wealthy. I just like to be involved, to learn, and to grow. I intend to do these things as much as I can until I run out of road.