Stocks should be fine. Sort of.

That’s a (deliberately) colloquial way of summarizing Goldman’s take on equities (from an asset allocation perspective) at a time of extreme uncertainty on both the policy and geopolitical fronts.

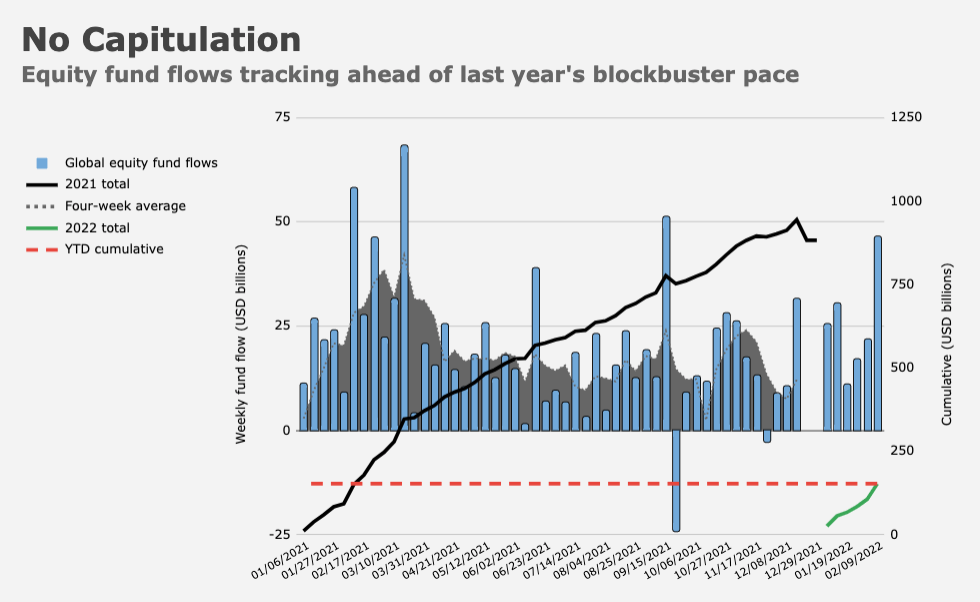

Again and again over the past several weeks, I’ve pointed to robust equity inflows as a sign that investors haven’t become despondent despite looming Fed hikes and the threat of a war in eastern Europe. Until last week, inflows to global equity funds actually outpaced those seen over the comparable stretch in 2021, a banner year.

I’ve also emphasized that cracks are starting to show in credit, where outflows have picked up materially. The latest Lipper data showed the second-largest combined weekly outflow from IG and high yield funds since the onset of the pandemic, for example (figure below).

“Looking at fund flows, the recent hawkish shift has already started to trigger a rotation out of fixed income, especially HY which registered record outflows as a share of AuM, and into equities,” Goldman’s Cecilia Mariotti wrote, in a new asset allocation update.

If that rotation continues, it could provide a pillar of support for stocks. While it may seem counterintuitive to suggest investors would simply rotate out of one risk asset and into another given the challenging macro backdrop, Mariotti noted that “a rotation out of the fixed income space and towards equities is consistent with the historical pattern during Fed hiking cycles since the mid-1980s.”

The figures (below) illustrate the point. In the six months after liftoff, stocks generally see inflows, while fixed income flows are robust headed into a tightening cycle, but decelerate thereafter.

You’ll note from the visuals that the last hiking cycle was an exception. A repeat of that anomaly seems unlikely, according to Goldman. “On that occasion the Fed started hiking against a weak macro backdrop which triggered a more risk-off market reaction as growth concerns were looming,” the bank said, adding that in their view, the “current inflationary pressures increase the risk that the impending Fed hiking cycle will be steeper and thus weigh more on fixed income.”

As for stocks (and this brings us full circle), Mariotti conceded that “a less friendly growth/inflation/policy support mix increases the potential for indigestion in the equity market and could resemble the 2015 and 2018 periods where we eventually saw large equity drawdowns.” That said, Goldman believes the outlook for growth is decent and corporate fundamentals strong, a combination which can mitigate the downside.

Still, Mariotti wrote that calls on gold may work as “a broad portfolio hedge… against bad inflation” and geopolitical tumult. It’s also worth noting that Goldman is now Overweight cash, which the bank casually noted is “becoming a more competitive asset.”

{kind=link}

I would assume investments in companies which develop and manufacture missiles of all types, tanks, submarines, aircraft and firearms (including robotic) would pick up big time when (if) Russia invades Ukraine. I think the large surface vessels are becoming too easy as targets for missiles fired from land, sea or air at great distances. As also are any land based targets like large manufacturing companies which may have to set up underground or in say a mountain to avoid new targeting systems. America can no longer assume it is safe from attack.

US defense procurement focus, as I understand it, is focused on missiles, missile defense, communications and intelligence, aircraft esp stealth, aircraft carriers and submarines. The companies involved are easy enough to identify.

(Survivability of carriers is unknown to me, but they are how US projects power in Pacific so the fleet is being modernized. Carriers do carry a ton of electronic warfare and missile defense, are defended by many support vessels, and are mobile thus present some issues for long range fire – so I’m told anyway.)

The focus for European NATO members might (my speculation only, haven’t studied it – yet) have more focus on ground weapons and less on naval.

Stocks will be fine after indices drop another 7%-10%.