“The stock market is not only in correction, it is already in bear market territory without a recession in sight,” JPMorgan strategists said, adopting a somewhat defiant cadence in a note dated January 31. “The equity market selloff is overdone in our view, and we reiterate our call to buy the dip.”

To be sure, there is something patently absurd about equities careening 10-20% lower (depending on what benchmark you’re referencing) and various manifestations of froth associated with policy largesse collapsing 50-80% with Fed funds still glued to the lower bound, real rates still deeply negative and the liquidity spigot still open.

It’s certainly true that the pain threshold for rising yields to undermine equities is lower over time, and there’s a multiplier effect when you consider that the longer real rates remain suppressed, the more inflated multiples become, and thus the more vulnerable to a de-rating in the event reals creep even a little bit higher.

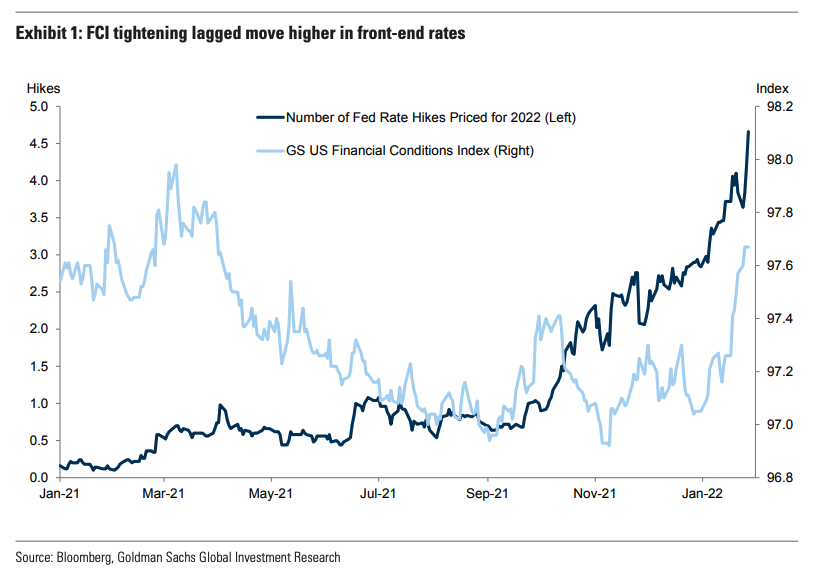

That said, even after a 50bps jump in reals over a four-week period, financial conditions are still easier than they were in March of 2021. Even if you assume a few rate hikes, additional losses for equities and some modest widening in IG, it’s hard to conjure a scenario where conditions become unduly restrictive in the near-term and even harder to imagine the Fed countenancing such a thing.

Inflation is politically unpopular. But so are recessions and stock market crashes. Obviously, inflation that spirals totally out of control would be ruinous for Democrats, but absent an unthinkable CPI escalation, it could very well be that the Fed quickly pivots to concerning themselves primarily with how to gradually normalize policy settings without upsetting the economy and markets. Everyone knows inflation is going to run above target in the medium-term. If it can just abate in-line with forecasts, that’ll give the Fed some breathing room.

“On the valuation side, the S&P 500 post-pandemic re-rating has almost been completely erased with P/E now only 0.5x higher versus pre-pandemic levels when rates were more restrictive and fundamentals were less supportive,” analysts led by Marko Kolanovic wrote. They went on to call the compression in small-cap valuations “extreme,” while pointing to a “sharp” decline in equity exposure among systematic strats. “CTAs are now outright short equities, and Vol Targeters have significantly reduced leverage,” the bank remarked.

That latter bit is important. Although it’s difficult to make definitive statements about dynamic models, there’s no question that systematic strats have been sellers. On Nomura’s estimates, CTA Trend sold more than $82 billion across global equities futures positions over the past two weeks, including $46 billion in US stocks. Vol control, meanwhile, shed $18 billion in US equities futures over the same period.

“It’s worth reiterating the magnitude of the equities selling by systematic strategies because this potent mix of ‘de-allocation’ flows (Vol Control) along with outright ‘shorting’ (CTA Trend) could act like synthetic ‘short Gamma’ on the way up, requiring mechanical ‘buying’ into sharp rallies,” Nomura’s Charlie McElligott said.

Meanwhile — and I’ve pounded the proverbial table on this lately — buybacks are set to resume. Blackouts peaked on Monday.

“More generally, investor sentiment is already extremely bearish with the Put/Call ratio reaching the highest level since March 2020 and AAII survey the lowest since H120,” Kolanovic and co. went on to say, adding that “as long as S&P 500 remains below ~4600, gamma is negative with dealers buying on strength and selling on weakness [which] would amplify market moves, especially in the current low market liquidity/depth environment.”

All of that will be familiar to regular readers. But it’s also worth noting that JPMorgan sees 2004-2006 as the closest parallel with the “current” tightening cycle (the scare quotes around “current’ denote that this cycle still hasn’t begun).

“From the start of 2004 to the end of 2006, the S&P 500 index delivered annualized total returns of around 10% supported by annualized 12-month trailing EPS growth of around 15%, and this allowed P/E multiples to gradually de-rate through the expansion without hurting the equity market,” the bank said.

They did concede the obvious: “No two cycles are identical, and the starting point for equities is somewhat different with a current P/E multiple above that seen in the run-up to the first hike in 2004.”

But if you’re not necessarily buying the notion that the US economy is on the verge of stumbling towards a shallow recession, the comparison makes sense, JPMorgan said. Additionally, the bank emphasized that “the hurdle for additional hawkish surprises this year has increased.” I’d say that’s an understatement. As I wrote pre-dawn on Tuesday,

[I]t does feel like market pricing for policy tightening has run as far as it can given currently available information. If something were to come along and force March to be fully priced for 50bps from the Fed, that would effectively be “max hawkish.” With runoff widely expected to commence in June/July (at the latest), and the Street coalescing around five hikes for 2022, there’s really nowhere to go other than fully pricing a “double-hike” in March. On the other side, there’s plenty of room for markets to reprice the Fed path lower.

Ultimately, Kolanovic and JPMorgan see the risks for stocks as “skewed more to the upside” considering the return of buybacks and quarter-end rebalancing from pension funds later in Q1.

As for the event risk posed by the March FOMC meeting, JPMorgan said simply, “If the March meeting proves hawkish and causes another correction in equity markets, that should be seen as another temporary dip/consolidation within a bull market.”

{kind=link}

You must be logged in to post a comment.