If the bearish US rates trade was already tired, December’s cooler-than-anticipated read on PPI could leave it exhausted. For now.

This goes without saying (although I said it anyway), but “cool” is an extremely relative term when it comes to all things “inflation” in the US currently. So, no one should misconstrue the message. The point is just that the market is looking for incremental evidence that the situation is becoming less acute, and even a slight downside miss on December PPI arguably sufficed.

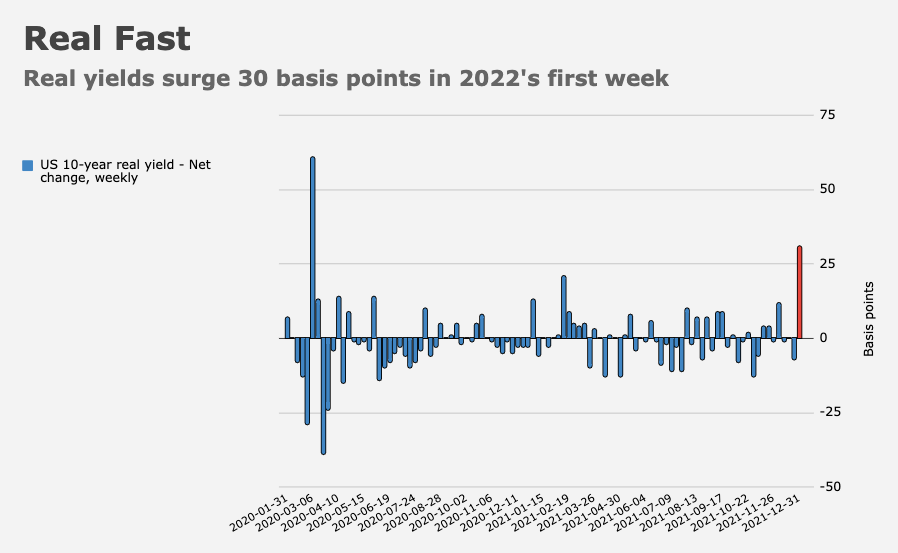

Assuming the above is a semblance of accurate, what does it mean for US equities in the near-term? Well, when taken in conjunction with my ad nauseam refrain that Fed pricing is likely maxed out for now barring some outlier data print, it suggests scope for additional relief in secular growth, tech and, more to the point, the rotational pain associated with the Fed pivot and last week’s real rate shock.

“Long-duration stocks declined sharply in the last two months of 2021, and that selloff has continued at the start of 2022 alongside the latest move higher in rates,” Goldman’s Ben Snider said, in a note dated Wednesday.

“The derating of equity duration is evident in the performance of select industries like Biotechnology as well as the relative returns of our Long Duration and Short Duration baskets,” Snider added, referencing the figures (above).

On Thursday, Nomura’s Charlie McElligott weighed in. “US Treasury yields now may be able to consolidate and help pause pain from the ‘(cheap) Value / (expensive) Growth’ rotation bleed, especially [if] you see Tech / NDX / SPX rally on [the] marginal PPI ‘disappointment’,” he wrote, on the way to saying dealer positioning is much more conducive to local stability.

At the same time, he noted that tech positioning “is much cleaner now, as per flows and PB data,” which, in turn, suggests reduced hedging needs. Charlie again mentioned moderation in vol metric extremes observed in QQQ options, with skew, put skew and term structure all “coming off the boil.”

Of course, these are mostly tactical considerations — the economy is at a pivotal juncture and it’s by no means clear that the Fed can ultimately succeed in corralling inflation absent the kind of draconian tightening that would prompt a recession. The “soft landing” debate is… well, still up for debate.

With that obligatory caveat, what counts right now is the extent to which there’s just nowhere else to go (if you will) when it comes to Fed messaging and pricing.

McElligott summed it up. “In the past week, we’ve seen 1) the Fed Minutes (and speakers thereafter) confirm balance sheet runoff beginning mid-year alongside simultaneous hikes; 2) US unemployment dipping below 4%; and 3) US CPI YoY at 7%,” he wrote Thursday.

What’s come of all that? Not much on the rates side, really. “EDM3 (June ’23 Eurodollar) is unchanged week-to-date and TY has rallied, which is telling us that the Fed, at this juncture, is generally priced-in,” McElligott said, on the way to driving the point home. “The longer the trade sits and stops working, shorts / downside trades in UST futs and ED$ will be incentivized to ‘profit-take.'”

{kind=link}

To play devils advocate, couldn’t a cooling of inflation be bearish for real yields and thus have a negative impact on growth plays?

H-Man,TY stabilized after being pounded down. Looks more like a dead cat bounce.