“Meaningful setbacks.”

That’s how BofA’s equity derivatives team described recent stumbles for US stocks, which have gyrated in the weeks since options expiry amid a laundry list of macro catalysts including perilous brinksmanship inside the Beltway and fears of a spiraling property meltdown in China.

For the first time since June of 2020, the S&P moved 1% or more in four consecutive sessions (figure below).

The accompanying rise in realized vol “triggered” what had become extreme loading in the vol control universe. Subsequent mechanical de-allocation from target vol contributed to downside pressure on stocks, which are in the throes of the first real setback since March.

September was, of course, the worst month for equities since the onset of the pandemic.

Late last week, the S&P snapped a 227-day stretch without a 5% pullback, the longest such streak since February of 2018, just prior to “Volpocalypse.” As BofA wrote, it was also the fourth longest in the last half century.

“Consistent with our thesis that stability breeds fragility, the two other longest streaks since the GFC culminated in severe risk-off episodes in August of 2015 and February of 2018,” the bank remarked.

Note the chart on the right (above, from BofA). Admittedly, the math is a bit tortured (that’s not a criticism, it’s just to say that if you go looking for anomalies, statistics will oblige if you insist on it), but last Thursday marked just the 24th time in nearly 100 years that the benchmark experienced two 3-standard deviation “shocks” in the space of 10 sessions.

As the subheading on the chart points out, stocks managed to make new highs over the subsequent month in just three of those historical instances.

The point isn’t to make mountains of molehills vis-à-vis a 5% pullback. Rather, BofA’s derivatives team simply noted that although “equity selloffs have in recent years signaled an opportunity to profitably buy the dip, history is less supportive of buying after clustered shocks.” The financial media is awash with conceptually similar stories documenting “the first real test” of the dip-buying mentality in the post-pandemic world.

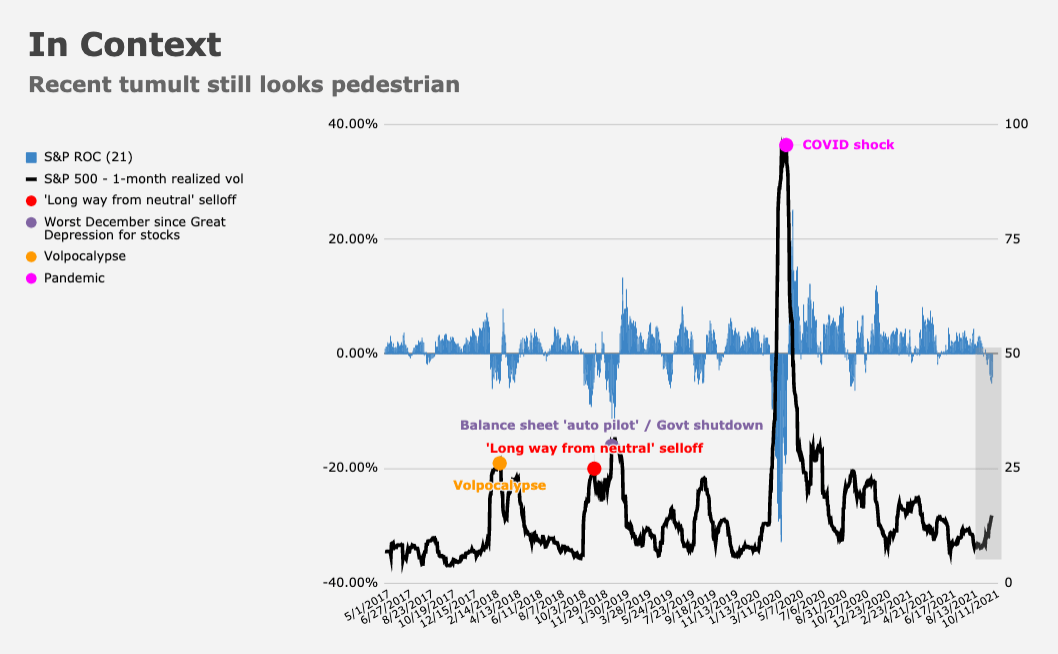

I’d be remiss not to reiterate that context is critical (figure below).

Seen through that (purposefully simplistic) lens, things don’t appear so dramatic.

BofA nodded to the relatively pedestrian nature of the pullback. “The magnitude of the recent weakness won’t make the history books,” the bank conceded, but cautioned that the fragility statistics documented above “may carry important sentiment implications for a momentum driven market.”

Remember, part and parcel of the post-GFC muscle memory is the consistent reward on offer for buying on any sign of weakness and/or selling vol at the first opportunity. That manifestation of classical conditioning optimizes around itself as traders attempt to front-run one another’s Pavlovian response function.

Although it’ll take more than one unprofitable counterexample to break the spell, failing to deliver a treat after ringing the bell confuses the dog. At some point, the animal will dissociate the sound from the food.

As BofA put it, “most important may be the realization that buying the dip has failed to be profitable this time, which may lower investors’ confidence in buying the next dip and helping resume the market’s climb.”

Love the Pavlovian reference there, sir!

“Although it’ll take more than one unprofitable counterexample to break the spell, failing to deliver a treat after ringing the bell confuses the dog.” I subscribe for the great and informative content, perfectly placed sarcastic humor is just icing on the cake.

“At some point, the animal will dissociate the sound from the food.” My sophomore Psyc prof was a staunch behaviorist. Part of his PhD researched involved training pigeons to respond to a light to get food. He trained them using something known as variable interval reinforcement. Once trained he removed the reinforcement and started flashing the light with no food to see how long it would take for the pigeons to give up believing in the relationship. Repeatedly, his pigeons would exceed 80,000 empty responses before they “disassociated.”