It wouldn’t be too much of a stretch to suggest that headline writers and financial media outlets were pleased to see German inflation accelerate in September.

After all, headlines about spiraling price pressures in Germany make for great click fodder — “Weimar,” and such.

For folks outside the polite world of mainstream financial coverage, it’s an excuse to use those old photos of paper money in wheelbarrows. Happy day!

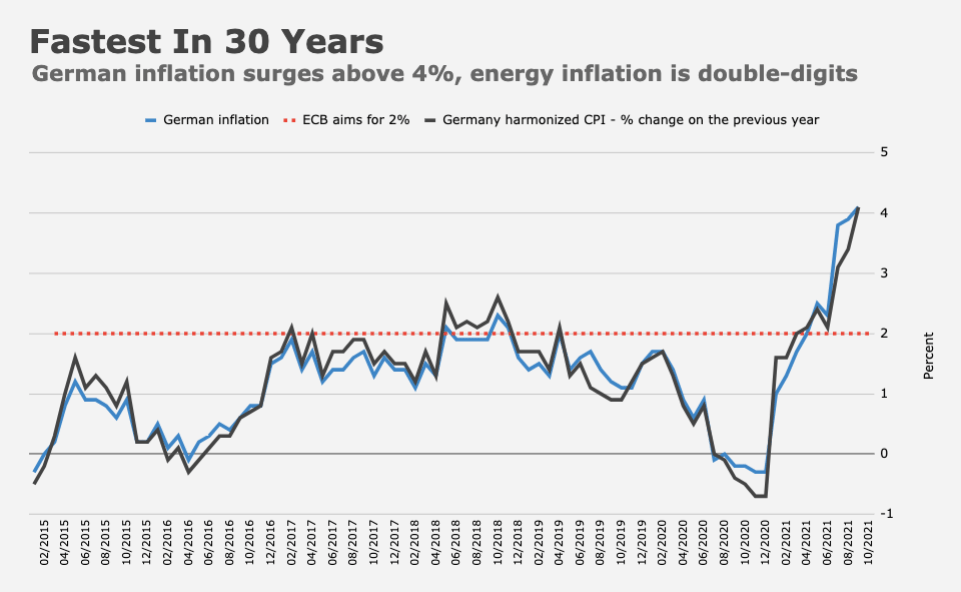

Anyway, I digress. Inflation rose 4.1% in September, the Federal Statistics Office said Thursday. That was the swiftest pace in almost 30 years (figure below).

Energy prices rose more than 14%, a dubious encore from August’s 12.6%, July’s 11.6% and June’s nearly 10% increases.

“There are a number of reasons for the high inflation rates, which include base effects,” the government said, mentioning the temporary value added tax reduction as well as “additional factors,” including CO2 pricing and “crisis-related effects, such as marked upstream price increases.”

You should note the difference in the rate of acceleration between the two lines in the chart. Constant-weight domestic prices rose much less (from 3.9% to 4.1%). It was HICP inflation which surged (from 3.4% in August to 4.1% this month).

Inflation in France and Italy also rose in September, separate data out Thursday showed. There too, the culprit was energy. The bloc-wide gauge is due Friday.

Like the Fed, the ECB generally insists the spike in inflation will prove transitory.

I suppose all I’d note — and I mention this frequently — is that when it comes to central banks’ “transitory” talking points, the loudest laughs tend to emanate from critics who, for years, counted themselves as deflationists.

The juxtaposition between, on one hand, the implicit suggestion that policymakers are wrong and that inflation is set to surge in advanced economies and, on the other, critics’ previously held views that the developed world will be forever mired in a deflationary quagmire due to a confluence of familiar dynamics, is only reconcilable to the extent sundry comedians can articulate the reason for that juxtaposition.

Too often, though, it’s clear that shrill critiques of central banks’ view on the likely duration (no bond pun intended) of price pressures are motivated purely by derision for its own sake.

Has technology ceased advancing? Is the automation push likely to slow? Are demographic trends improving in developed economies? Is there not now vastly more debt than there was pre-pandemic?

If the answers to those questions are “no,” “no,” “no” and “yes, there’s much more debt,” then you’re basically left with four arguments for inflation:

- Supply chains will never be the same post-pandemic. Globalization, just-in-time, etc. are antiquated concepts. National security concerns will drive an on-shoring push and the demise of specialization will invariably push up prices.

- Underinvestment in fossil fuels will lead to a crisis in a world where sustainable energy and renewables aren’t yet ready to take the baton.

- Too many mouths to feed and climate change will invariably lead to food shortages, driving up prices.

- The combination of easy monetary policy and fiscal largesse will turn the dollar, euro and yen into the bolívar.

So, there you go. There’s your manual. I’ve done the hard work for you. If you want to argue for an inflationary spiral, those are your talking points.

Lacy Hunt begs to differ, though. The excerpt (below) is from Hoisington’s latest economic outlook (from July).

The current economic growth and inflation rates of 2021 will be the highest for a very long time to come. The main obstacle to a return to sustained growth in the standard of living, extreme over-indebtedness, was dramatically worsened by the multiple rounds of fiscal stimulus which has caused the temporary improvement in economic growth and inflation in the second quarter. No pathway out of this trap exists as long as the overreliance on debt remains the only tool of monetary and fiscal policy. The situation is no different in Japan and Europe. Thus, while long Treasury yields can increase over the short run, the fundamentals are too weak for yields to stay elevated. More debt does not cure a subpar economy mired in a debt trap. Our view is that the trend in long-term Treasury yields remains downward.

Say what you will, but at least he’s consistent.

It is hard to argue with Lacy Hunt. He has been on this DebtGDP vs lower real yields arguement for 30-years and has proved more right than wrong. However, if looking for it is different this time, there is a new development that just could prove him wrong. If labour share of GDI bottoms out and goes higher, this correlates well with R-star and by extension real Treasury yields.

For sure your “residual” arguments in support of inflation strike me as dead on. While #3 still owes some apologies to Malthus, at some point he will (have) be(en) right. Argument #2 is as yet a stealth problem which will really start striking us in earnest in five years or so.