After some catch-up selling in Asia, markets calmed a bit on Wednesday.

Tuesday’s rates-driven dramatics served as a rather poignant reminder of how quickly things can go awry when the world’s most important stocks are tethered so closely to bond yields and the curve.

It was clear from the starting pistol that this week might be a test of tech’s resiliency in the face of a burgeoning bond rout. Whether retail investors and sundry dip-buyers will forgive and forget may be largely irrelevant if bonds don’t settle. Thankfully, yields fell back on Wednesday and tech attempted a rebound.

The Nasdaq 100 has logged a pair of 2% declines in September (figure above).

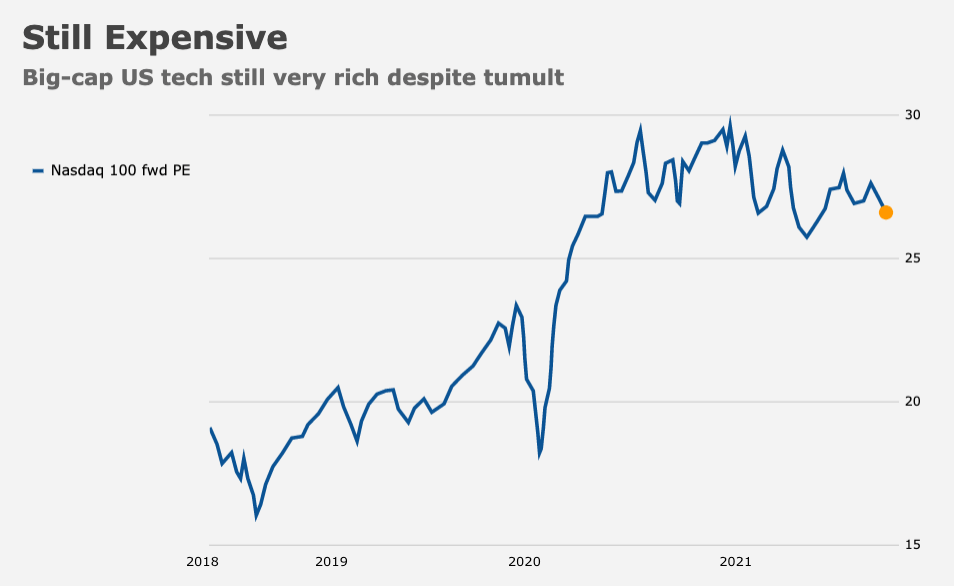

US tech is derating. Albeit slowly. At 26, we’re well off this year’s highs (~30) but consider that the Nasdaq 100 traded at ~18X at the depths of the pandemic plunge and at ~16X during the mini-bear market that played out in Q4 of 2018 (figure below).

As ever, this is mostly just a guessing game in the near-term. I’m famously averse to Warren Buffett quotables, most of which are so nebulous that they could just as easily apply to walking across the street as they could to markets, but it’s always refreshing when he and Munger reiterate that they have no idea where stocks are going over the short run. The point, which often goes unspoken, is that if they don’t know, neither do you and neither does anyone else.

But that doesn’t stop folks from trying. Take RBC, for instance. Lori Calvasina is worried that a decline in asset manager positioning in US equities along with a “sharp and sudden bearish turn” in retail investor sentiment, presages something bad. “A decline in positioning in S&P 500 contracts contributed to the move, meaning investors pared general US equity exposure not just specific trades,” the bank said, referencing last week’s action. “Even with last week’s dip, institutional investor positioning remains quite elevated relative to history, suggesting the stock market remains vulnerable to bad news on fundamentals.”

Earnings season is coming up, so there could indeed be some “bad news on fundamentals,” notwithstanding the extent to which corporate America has blown the proverbial doors off this year (figure below).

On the other hand, Bernstein’s Mark Diver and Sarah McCarthy shrugged off last week’s outflow from global equity funds (the first of 2021), noting that such outflows aren’t unusual in September and typically come on the heels of a large inflow the previous week.

That would certainly fit with the last two weeks’ data. Recall that investors poured more than $51 billion into stock funds just prior to the “anomalous” $24 billion exodus. We’ll get a fresh read tomorrow evening.

Read more: Madness! Stocks Suffer First Outflow Of 2021

It’s also worth keeping in mind that financial media is a business, just like almost all media. It’s not necessarily designed to inform, but rather to entertain. I try to emphasize that at regular intervals, especially during selloffs.

“Headline writers and those who dabble in adjectives… put their best tools to work when tragedies strike and markets shudder,” Bloomberg’s Ven Ram wrote Wednesday. “So it should come as no surprise that with both the Nasdaq Composite and the S&P 500 hurtling down with multi standard-deviation velocity on Tuesday and Asian stocks going along for the ride overnight, the best epithets have been at work.”

Meanwhile, the BOJ bought ETFs for the first time since June on Wednesday. The Topix fell 2%, prompting Kuroda to step in with 70.1 billion yen in stock purchases.

Meanwhile, the BOJ bought ETFs for the first time since June on Wednesday. The Topix fell 2%, prompting Kuroda to step in with 70.1 billion yen in stock purchases.

Who needs a CB Put when you can have a plunge protection team actually buying? What they need to do now is YOLO it by adding buying of single name short dated Calls on all components of the index…