Recep Tayyip Erdogan is irritated. At grocery stores.

“Markets are turning upside down with products collected by these five market chains,” Erdogan told reporters this week, while in the US for the UN General Assembly.

“If they act more fairly, citizens will be able to buy groceries at reasonable prices and producers will also get their money earlier,” he seethed, warning that if Turkey’s largest chains didn’t correct their behavior, the Trade Ministry would take “measures.”

He didn’t specify the measures, nor did he name the chains, but markets got the message. Shares in BIM Birlesik Magazalar AS, the nation’s largest chain by market cap, fell 2% Friday (figure below). The second-largest, Sok Marketler, fell more than 3%, as did Migros Ticaret AS and CarrefourSA Ticaret Merkezi AS.

It didn’t take long for the government to make good on Erdogan’s threat. On Saturday, Trade Minister Mehmet Mus ordered inspections.

“Considering the applications and complaints submitted by our citizens regarding the exorbitant price increases in basic food and necessities, audits are carried out by our Provincial Directorates of Commerce regarding whether exorbitant price increases have been made in 81 provinces and whether there are any violations of the Price Label Regulation,” a notice posted on the Trade Ministry’s website said, adding that the government will examine “a wide range of products from eggs to milk, from pasta to rice, from vegetables and fruits to cleaning materials in the five big chain markets operating all over the country and having the most widespread network.”

To be sure, Turkey is hardly the only country experiencing higher food prices. But, as ever, Erdogan isn’t helping matters. On Friday, the lira fell to a new record low (figure below), following a “surprise” Thursday rate cut from Sahap Kavcioglu.

Kavcioglu, you might recall, was installed as central bank governor in March after then governor Naci Agbal delivered a 200bps rate hike. It was a bridge too far for Erdogan, who famously adheres to an “unorthodox” view on rates, FX and inflation.

In Erdogan’s mind, the cure for inflation is easier policy and lower rates. Suffice to say that approach hasn’t served the currency particularly well. Periodically, the lira careens lower, pushing Turkey to the brink of crisis, only for Erdogan to step in at the last minute with some palliative remedy which EM watchers invariably (and inexplicably) accept — only to be made fools of months later when Erdogan reverses course. SocGen’s Phoenix Kalen calls it “a vicious infinite loop.”

That’s precisely the cycle that played out over the past 10 months. Agbal, Kavcioglu’s hawkish predecessor, replaced Murat Uysal in November, during a hasty shakeup designed to restore market confidence amid a steep decline in the currency. Uysal, who took over for Murat Cetinkaya in July of 2019 after Cetinkaya failed to slash rates fast enough to appease Erdogan, delivered a total of 1,575bps worth of easing during his first 14 months on the job. That pleased Erdogan, but by November of 2020, the situation had become untenable. The lira was mired in its longest weekly losing streak since 1999. Something had to change.

Agbal managed to deliver 875bps worth of tightening during his short-lived tenure, and he may have gotten away with the final hike in March had it not been twice the size of the move markets expected. That it was accompanied by a (very) hawkish policy statement was the last straw for Erdogan.

Kavcioglu kept rates unchanged for his first five meetings, but Erdogan’s insistence on lowering borrowing costs while simultaneously bringing down inflation meant that it was just a matter of time before the central bank was forced into another rate cut on the (patently absurd) premise that easing policy would ameliorate price pressures in an emerging market which has lost virtually all credibility when it comes to central bank independence.

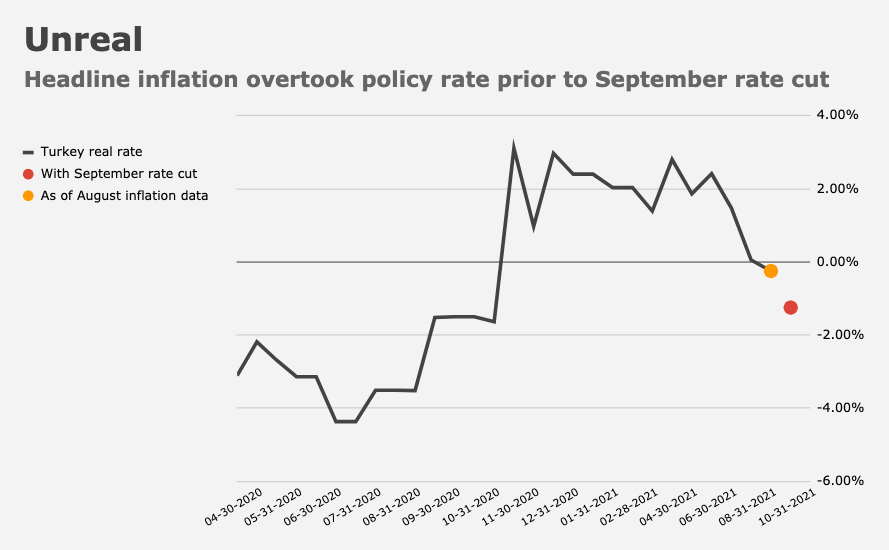

And, so, Kavcioglu cut rates by 100bps this week. As usual, “experts” were shocked. Out of nearly two-dozen economists polled, 22 predicted no change. That, despite Kavcioglu essentially pre-announcing the move weeks ago by shifting the bank’s focus to core inflation, which removes food. Happily, core is much lower than headline inflation, which is running at a harrowing 19.25% (figure below).

“The extraordinary conditions, especially due to the pandemic, increase the importance of core inflation indicators,” Kavcioglu explained, during a speech in Ankara earlier this month.

“Globally, when monetary policy stance is determined, core indicators excluding transitory factors emanating from areas outside monetary policy’s influence are taken as the basis,” he added, tacitly suggesting that CBT has the leeway afforded to developed market central bankers when it comes to determining what “counts” while assessing inflation.

Of course, Turkey is an emerging market. And really, that’s beside the point. The problem is Erdogan and the accumulated credibility deficit built over the past three years, a period during which Turkey has had four central bank governors. To put it bluntly, the country would likely be on governor number five as of this weekend had Kavcioglu not cut rates this week.

“To be clear, what have not been transitory have been the pronounced deterioration in inflation expectations since the spring of 2020, the lack of reserves ammunition to support financial stability and the lack of progress on de-dollarization,” SocGen’s Kalen wrote. “Now compounding the situation are deeply negative real rates and the diverging paths in monetary policy stances between Turkey and many other emerging market counterparts,” she added. “Throw in Turkey’s volatile politics, and the relative comparisons grow ever more unattractive.”

Switching the bank’s focus to core inflation allowed Kavcioglu to claim the policy rate isn’t below the inflation rate. August’s data, out just days before Kavcioglu made the change, meant real rates in Turkey were negative again (figure below).

Incorporating September’s cut, real rates are the most negative since Agbal took over for Uysal.

“Admittedly, the hawkish rhetoric of the past several months had gained Kavcioglu some credit, pushing us and others to defer the date of when the first cut was expected,” TD’s Cristian Maggio said. “In our case, we’ve been repeatedly postponing the beginning of the rate cut cycle since the new governor’s appointment in March, with our last forecast round pushing the timing back to October,” he added, noting that “contrary to the CBT hopes, the grip of inflation never eased during the summer… leaving the MPC with very few options but hold and hope.”

Yes, “hold and hope.” But Erdogan isn’t a patient man. And Turkey isn’t a democracy.

“The issues now are centered on the collapse of credibility in the monetary policy framework, as market participants are likely to attribute [the rate cut] to the heightened political pressure being exerted on the CBT to enact a rate cut,” SocGen’s Kalen went on to lament. “The central bank appears to have succumbed to President Erdogan’s demand for an interest rate cut by September.”

Indeed. I suppose all I’d say is that EM watchers would do well to remember Maggio’s assessment from March. “Monetary policy in Turkey is not set up to control inflation — it is a pure function of the pro-growth inclinations of the government,” he wrote, adding that,

It also responds reactively (and usually with a strong lag) to uncontrolled currency weakness. Which means the implicit mandate of a CBT governor is not to achieve 5% inflation, but to make sure that the credit impulse remains in place, while avoiding a collapse of the Turkish lira.

Following this week’s move, Maggio had one question: “Let’s be honest, who’s really surprised about the surprise cut?”

The lira is on track for a ninth straight year of depreciation.

Possible (black swan) turkey shortage in UK?

“Supermarket shelves of carbonated drinks and water were left empty in some places and turkey producers have warned that families could be left without their traditional turkey lunch at Christmas if the carbon dioxide shortage continues.”

The UK situation is certainly interesting, the political narrative, from both sides , is one of COVID related supply chain disruptions, whereas in fact it’s really due to Brexit.

One need look no further than Northern Ireland as evidence , part of the UK , but still inside the EU for trade . Northern Ireland is not having the same supply difficulties as the rest of the UK.

Another example of political stupidity and populist leaders harming their own populace

Spot on. And it’s not just the UK suffering from populist fueled supply shortages. The biggest unreported financial story of the year is how the deranged former president spent 4 years destroying the American connection to the global supply chain.

Thanks for that.We here in the U.S. are privileged to watch from the cheap seats (we hope) what happens when you don’t have a respected printing press and a leadership with some modicum of rationality.

We are all still in the midst of an epic pandemic crisis, even though many among us have heads deeply rooted beneath shifting sands. The concept that global economies are snapping back into pre-Covid trends is hogwash. All anyone has to do is look at Florida, Texas, Idaho, et al, etc and look at the fact that a massive amount of unvaccinated people are piling up every day -=- as-if, this is normal. In most states, hospitalization are declining, while most people ignore the spikes in death rates. I can’t help but think the GOP is losing voters and that Covid is reshaping demographics (for the better?). Looks like a long dark road ahead everywhere — kinda like whack a mole with hydra heads … party on Wayne.

“We are in a time of CO2 shortages once again, with shortages on the West Coast, the Midwest, and the Mid-Atlantic and Northeast,” Rushing told gasworld.