It was as predictable as it was laughable.

Stocks ended the week mostly unchanged, making geniuses of dip-buyers, vol sellers and retail investors, whose Pavlovian instincts were rewarded yet again.

US equities brushed aside the Evergrande drama and found plenty to like in what some still insist was a “hawkish” September Fed meeting.

This week will go down as yet another piece of confirmatory evidence in favor of the notion that “BTD” is no longer just a derisive meme about retail bagholders. Rather, it’s a (mostly) infallible strategy that manifests in a variety of ways, some of which go well beyond plowing $5 billion into SPY, QQQ and mega-cap tech, as individual investors apparently did.

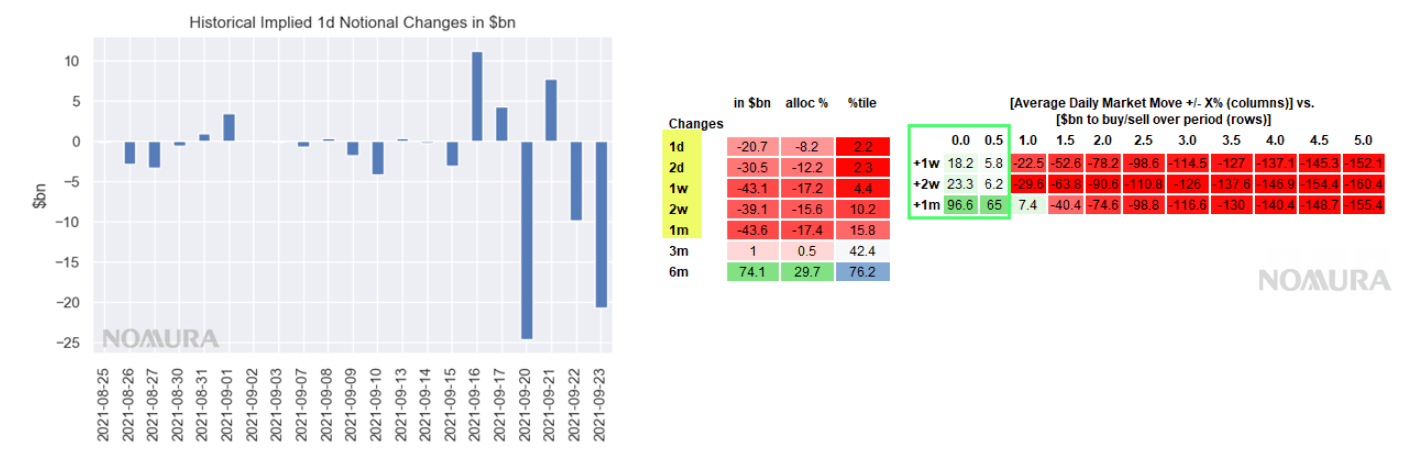

The rebound from Monday’s pullback may have been even more impressive were it not for lagged deleveraging from the vol control universe, which mechanically pared exposure as trailing realized moved higher (figure above) after the fireworks.

“The continued ‘overhead resistance’ into what has been an otherwise fierce rally this week off the lows has been systematic Vol Control supply,” Nomura’s Charlie McElligott suggested on Friday.

On the bank’s estimates, there was nearly $21 billion for sale on Thursday and more than $43 billion over the past week (figure on the left, below).

So, what happens now? Well, if we focus strictly the “mechanics,” so to speak, and assume the forthcoming political battles (stateside) and credit event (in China) don’t trigger another “shock down,” we may end up back in the “hamster wheel,” as McElligott put it.

Given recent events, I could scarcely conjure a better way to close the week than the following two bullet points from McElligott’s Friday note. This is the “hamster wheel” in his words:

- ”Short vol” as a yield enhancement / risk premia strategy which gets Dealers “long gamma” and helps insulate market from selloffs, pins rVol at brutally low levels where we don’t see price swings and inherently then allows for large build-up of exposure and leverage particularly within the target vol / risk control universe…ultimately sees the Op-Ex cycle as a “vol expansion” opportunity as supportive vanna- and charm- dynamics drop and “gamma” is unclenched, then opening the “window for movement” that can further be fed into by macro concerns (“hawkish” Fed, China Evergrande, pandemics, Bitcoin headlines, Trump Tariff tweets etc) in conjunction with “accelerant flows” (long gamma flips short, delta de-risking, CTA trend / Vol Control deleveraging)…

- But as the second-order flows wash out, we have been trained then to “harvest” rich vol by selling it—along with monetizing downside hedges with the quickness—which creates delta to buy, stabilizes, then rallies, the market off the lows in a vacuum, which then means higher prices feed lower vols as dealers get back some of that short gamma from options sellers, which in conjunction with spot rallying again “insulates” the market from further price swings—and ultimately, as vol resets lower, systematics vol control / target vol are then signaled to re-allocate / re-leverage…back up we go

Taken together, those two bullet points neatly summarize the interplay between modern market structure, macro and policymakers.

Headed into October, any stabilization that sees spot settle back into a ~50bps (for example) channel for daily moves could see vol control reengage meaningfully (see the table on the right in the visual above).

Stocks aren’t terribly likely to realize a 0% daily change for a month, so taking the more plausible scenario wherein daily changes are around 0.5%, vol control could re-allocate to the tune of around $65 billion.

I found this on the internet, must be true?

“Hamsters are full of energy and can run up to 9 miles in a day, so a wheel is essential to keep them happy.”

Surely the physicists that have been hired onto Wall St have modeled all of this. I honestly couldn’t tell you the difference between gamma and an unclenched vol (or vole?), but one would expect that the anticipation of the dip-buying opportunities (an oscillatory pattern) would get built into the strategies of the big players, and all of the options expiry excitement will be pulled forward and incorporated into the algorithms, and this particular oscillation will get smoothed out. But someday there will be a breakout event. Something will happen that reinforces, rather than opposes, the monetary forces that have been applied to generate an artificially smooth graph out of what should be an inherently noisy system. When that happens–well, it might get loud (maybe as loud as Jimmy Page, Jack White, and the Edge combined).

Of course they’ve modeled it. Vol control, CTA, etc. are systematic strats. The algos you’re talking about are embedded in the structure. On top of that, algo market making can exacerbate the situation because they tend to retreat in the face of turmoil, very much contrary to what HFT proponents contend. That can lead to diminished liquidity, wider bid/asks and more dramatic swings, which in turn increases volatility. Volatility is inversely correlated to market depth. So all of these vol-sensitives are selling into a thinner market that gets thinner the higher vol goes. Algos are part of the problem.

ultimately sees the Op-Ex cycle as a “vol expansion” opportunity as supportive vanna- and charm- dynamics drop

I know what gamma and vol and option expiries are. I don’t know what vanna and charm dynamics dropping mean in terms of market structures? Can someone explain?

Ah! https://www.youtube.com/watch?v=-RhSCoElB9Y&ab_channel=KeyPaganRush