Over the past several months, there’s been no shortage of banter about extremes in various “crash” metrics.

And no shortage of bad, but unavoidable, jokes, either. Things are “all skewed up,” for example.

There are a variety of talking points to choose from, and they’re all related. The uncomfortable juxtaposition between, on one hand, the high relative cost of hedging drawdowns and, on the other, subdued realized vol, is a continual source of consternation, as is seemingly insatiable demand for left-tail versus de minimis interest in “crash-up” expressions. Colloquially, these kinds of conjunctures create scary optics.

In a new vol outlook piece dated this week (how timely), SocGen’s Vincent Cassot and Jitesh Kumar pondered a market “climbing a ‘skew’ed wall of worry.” (Like I said, the jokes are unavoidable.)

Among the questions they asked: “Is a lack of supply or excessive demand responsible for extreme skew?” and “Are the extraordinary investment returns over the past six quarters adding to the demand for hedges?”

This might sound esoteric to some “everyday” investors, but at least until you go drilling “too far” down, it’s actually a pretty pedestrian debate, replete with readily-accessible (i.e., easy-to-grasp) concepts.

For example, Cassot and Kumar noted that based on their math, “the left tail [currently] adds a little under 4.5 vol points to the VIX, while the right tail contributes almost nothing.” The figure on the left (below, from SocGen) illustrates the point.

The figure on the right (above) just shows the relative cost of hedging.

As noted here on countless occasions, regulatory constraints are a big part of this discussion, or at least on the supply side. It’s a risk management issue. “There is substantial anecdotal evidence of banks regulating balance sheet access… especially after the blow-up of some high-profile funds last year and early this year,” Cassot and Kumar wrote, before noting that “a general aversion to asymmetrical downside risk” also plays a role.

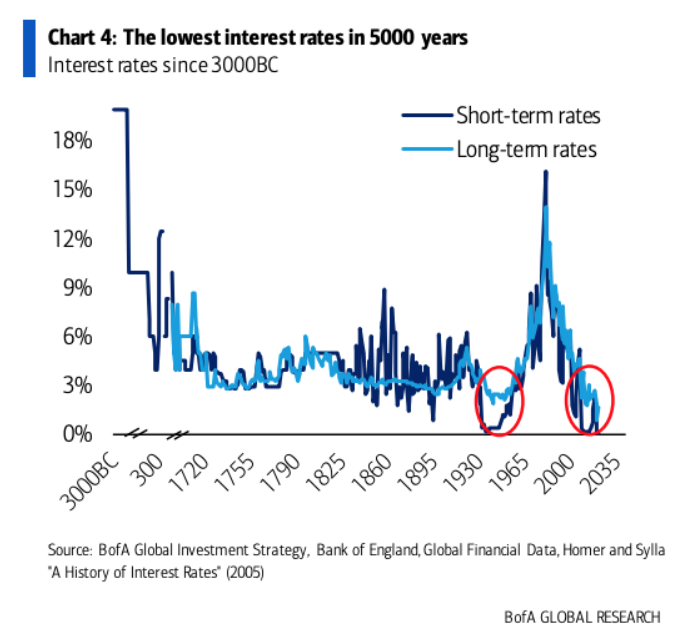

Meanwhile, factors impacting demand include high pension funding ratios, increased participation from retail traders in the options market, a quest for alternatives to bonds as hedges with yields at 5,000-year lows (literally) and the stunning equity rally off the March 2020 pandemic panic nadir.

On the latter point, you might be wondering how the current situation compares to the post-GFC period. Cassot and Kumar produced scatter plots showing YoY returns for US equities versus the cost of hedging and, more germane, the relative cost (figures below).

While they noted that the 2009 rally “also saw a sustained higher level of put prices… the relative cost of downside to upside hedges does appear quite elevated this time around.”

There are a number of takeaways from Cassot and Kumar’s latest outlook piece. It’s nearly three-dozen pages long, and this certainly isn’t an attempt to summarize it or even to hit all the proverbial high points. Rather, the point here was simply to highlight some additional color on a hot topic.

If pressed to pick one key point, I’d quote from Cassot and Kumar’s introduction, where they wrote that, in their view, widely-discussed extremes seen across various metrics as investors look to protect capital are the result of a supply-demand imbalance “rather than a fundamental change in investor outlook.”

Oh, and they also wrote that their models continue to suggest that realized vol will fall. “Higher implied volatility levels will likely provide opportunities to sell the expensive level of skew/convexity,” they said.

If you’ve been paying attention over the past several months, that probably sounds quite familiar.

{kind=link}

H-Man so when are extremes not extremes? And if your portfolio is getting hammered, that is an extreme event. Does that change your sentiment? I guess it depends for how long and how much the portfolio gets hammered. It would appear that an “extreme event” drives the bus like Covid when vol shot through the roof. So when they say vol will fall in the near future, I guess that is right unless an “extreme event” shows up. There are a few of those on the radar.

Great as always. I have been thinking about this skew view of positioning the last couple of weeks. Upside calls on the SPY into year end are just too cheap compared to puts, everyone buying crash down protection makes taking the other side attractive. If one believes JP Morgan’s target of 4700 by year end is a possibility, a call spread or even a calendar spread using that target into December/January offers a ridiculously good risk reward right now, at least it did yesterday when I placed my bet.

If you were a real man you’d do what we used to call risk reversal trades! Sell puts to finance your call purchases. When the skew is extended, you can buy closer strike calls using what you earn from your put sales.

Interesting though, wasn’t the skew in reverse not long ago? Weren’t calls in higher demand? That struck me as being more strange.

The current skew is interesting, but rational. In my ancient mind, anyway.