I spent most of Monday going on about vol-sellers and whether they would or wouldn’t reengage to help stanch the bleeding in equities given the proximity of the September FOMC event risk.

As it turns out, they did. Brave souls, that bunch.

I jest. They’re not brave as much as they are conditioned. As Nomura’s Charlie McElligott put it, “the back-test on vol spikes tells you that you have under one day before the rally in spot.” That was a joke. And it was funny because it’s mostly true.

Fast forward to Tuesday and equities were indeed looking for gains.

“There is simply no way to overstate the power of the ‘reflexive vol sellers’ into another spike,” McElligott said, in a short note, the first line of which read “The vol event is dead…long live the vol event!”

He cited put sellers “directionally shorting ‘rich’ vols [on Monday] and ‘long sellers’ who monetized downside hedges by the close.” Ultimately, that set the stage for another “turnaround Tuesday,” albeit under a cloud of Evergrande uncertainty.

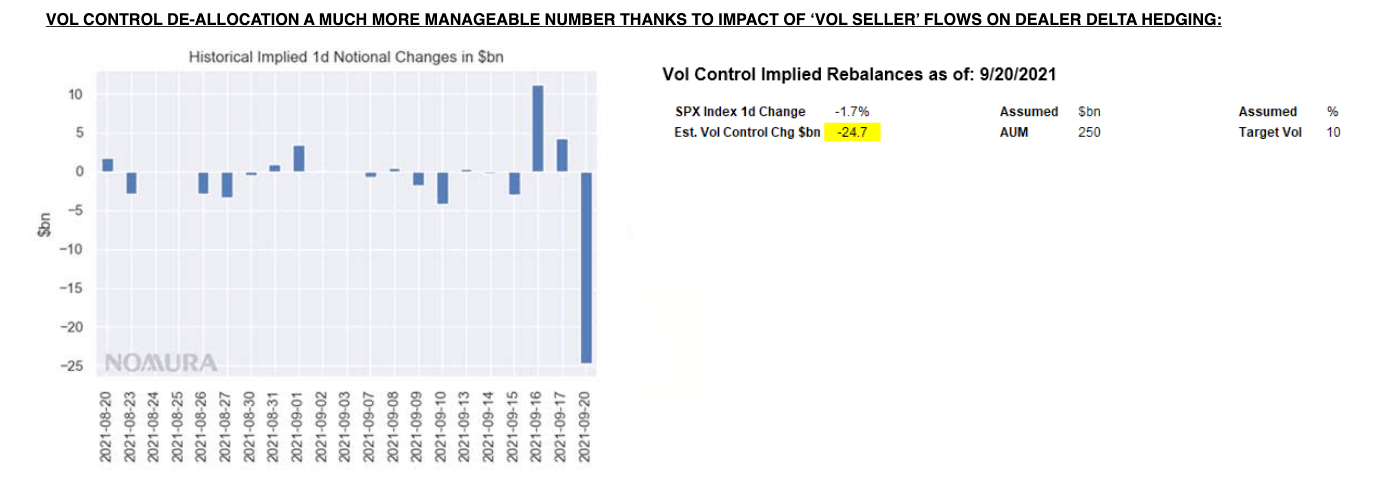

What’s especially notable is that the Pavlovian response (i.e., shorting vol into these now predictable single-session deleveraging events) helped mitigate the scope of potential delayed selling from the vol control crowd.

“That Delta buying in the late day was hugely important in reducing the absolute $ of systematic deleveraging ‘accelerant’ flows,” McElligott said Tuesday. “Only closing down -170bps in SPX then meant a much more manageable -$24.7 billion of Vol Control de-allocation in coming days, as opposed to what would have been a much more challenging -$62.9 billion to digest,” he added.

It also reduced the rebalancing burden on leveraged ETFs by around a third.

Meanwhile, on Nomura’s models, the aggregate CTA signal didn’t come anywhere near triggering.

None of that is to say markets have the all-clear signal. Or at least not if you’re inclined to worry about ongoing tension in the vol complex as manifested in extreme readings on myriad crash metrics.

“To our amazement [Monday], we saw confirmation of our repeated point that ‘the only thing that clears out all that ‘crash’ pricing in vol metrics is a crash,’ yet… we actually saw Skew steepen further despite incredibly high levels of both ATM Vol and Skew,” McElligott went on to say Tuesday. “That tells us that the Dealer ‘short Vol / short Skew’ problem still remains lurking in background.”

He added a cringe emoji.

You must be logged in to post a comment.