Activity in the world’s second-largest economy slowed again in August, closely-watched data out Wednesday showed.

Retail sales in China rose just 2.5% YoY last month (figure below), barely matching the lowest estimate from 35 economists. Consensus was looking for a 7% increase.

This is a familiar tale. Concerns about domestic demand haven’t abated, even as retail sales eventually caught up to the rebound in industrial output after lagging in the initial stages of the country’s recovery from the pandemic. August’s huge miss won’t likely be greeted well by markets.

There’s quite a bit of concern that China’s strict adherence to a “zero tolerance” COVID policy will impair consumption, and Xi’s ongoing regulatory crackdown likely isn’t doing much to bolster sentiment, even as the commitment to “common prosperity” ostensibly bodes well for Chinese consumers in the long-term.

Industrial output came up short for August too. Production rose 5.3% YoY. Consensus was looking for 5.8%.

Fixed asset investment was 8.9% and the surveyed jobless was steady at 5.1%

The numbers for August marked a second consecutive month of underwhelming activity. The fresh read on China’s burgeoning slowdown came on the heels of PMIs which showed the services sector contracting (figure below).

Both the official gauge and the Caixin index are below the 50 demarcation line for the first time since February 2020. That telegraphed a poor read on consumption, although I’m not sure too many expected the headline retail sales print to come in as wide of the mark as it did.

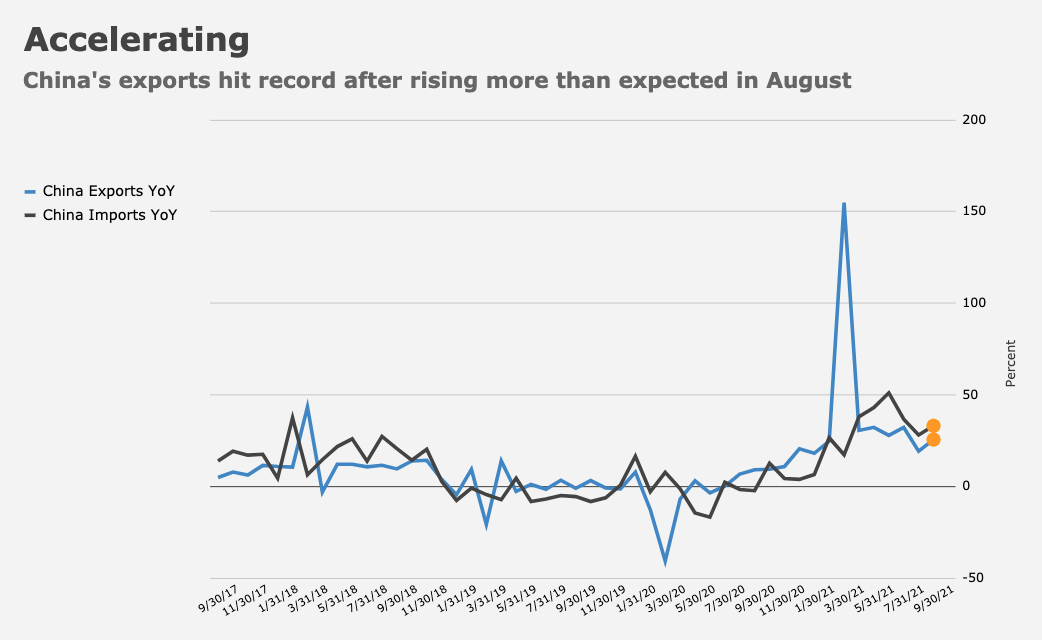

It’s not all bad news. Recall that trade data for August was robust, and as I’m fond of reminding folks, Beijing is no stranger to precarious juggling acts involving competing priorities and imminent, overlapping crises.

That said, authorities currently face a particularly perilous tightrope walk. Efforts to clean up the property sector are perhaps the most vexing issue outside of virus containment, and the Evergrande saga is rapidly approaching a rather unceremonious denouement.

“Markets may have become so focused on the recent regulatory storm that they ignore the elephant in the room: Beijing’s unprecedented curbs on the property sector, which makes up one-quarter of China’s economy,” Nomura’s Ting Lu wrote, in a widely-circulated note late last month. “In a sense, this could be China’s Volcker moment, considering Beijing’s strong willingness to sacrifice some near-term GDP growth for taming home prices and diverting financial resources out of the property sector,” he added.

The broad credit impulse turned negative earlier this year, which doesn’t bode particularly well, and there’s rampant speculation around the PBoC’s next move following July’s RRR cut.

For what it’s worth, 82% of participants in the September vintage of BofA’s Global Fund Manager survey expect China to ease (figure below).

Opinions vary on what tools the PBoC will use. OMO rates and LPR haven’t been cut in 16 months, and most analysts seem to think targeted easing measures are more likely than a broad-based approach.

On Wednesday, the PBoC conducted 600 billion yuan of MLF, matching maturing funding. The rate was unchanged.

{kind=link}