Outside of jitters about the durability of the US recovery in the face of surging consumer prices and the spread of the Delta variant, there’s no bigger concern for macro watchers than the prospect of a marked deceleration in China.

Admittedly, that opening sentence doesn’t tell you very much. After all, the economic outlook for the US and China is always top of mind, because those are the two largest economies on the planet.

But currently, each faces a unique set of circumstances, with varying degrees of overlap. Western observers are beginning to fret obsessively over Xi’s “zero tolerance” COVID policy, which manifested last week in the partial closure of the third-busiest container port on the planet after a single asymptomatic case was identified.

Read more: The Butterfly Effect

Headlines about an “isolated” China notwithstanding, the idea that global trade can somehow sustain a full recovery when Xi is quite obviously prepared to go to extreme lengths to stamp out flareups, is manifestly ridiculous. So goes China, so goes the ebb and flow of global trade and commerce. Hence the hand-wringing over the Party’s draconian approach to containment and authorities’ refusal to countenance notions about “learning to live with” COVID.

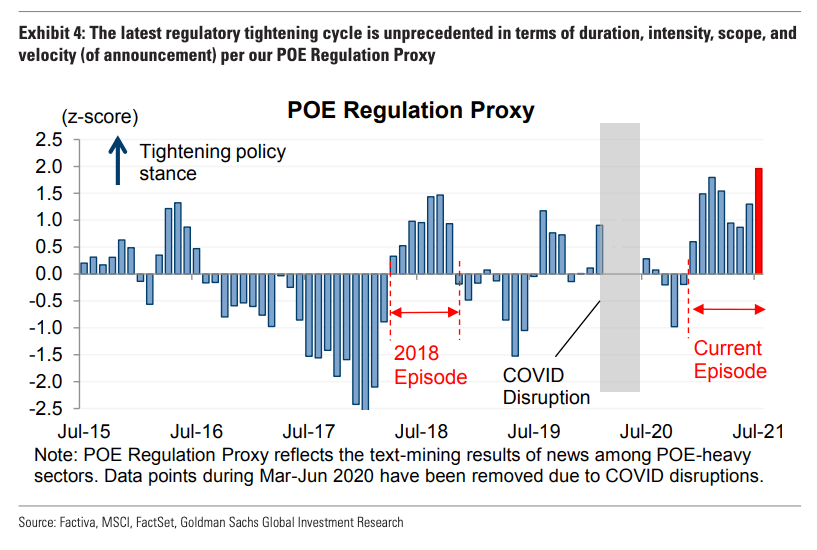

The recent outbreaks across the country came just as growth was poised to start decelerating in earnest. Beijing’s sweeping regulatory crackdown had already cast a pall over market sentiment, as did persistent nods to reining in property speculation. Credit creation was the slowest since February 2020 last month (figure below).

The pace typically slows in July anyway, but the figures were well short of estimates.

Expectations for additional easing on top of last month’s RRR cut are now building, and analysts spent the last several weeks reassessing the outlook for growth.

It’s with all of that in mind that China released activity data for July on Monday. The numbers missed across the board.

Retail sales rose just 8.5% YoY (figure below). That was well below the 10.9% the market expected. The low-end of the range was 10%.

Concerns about domestic demand haven’t really abated even as retail sales eventually caught up to the rebound in industrial output and despite robust imports. China’s trade data for July, out earlier this month, underwhelmed, but evidenced resiliency nevertheless.

July’s retail sales figures certainly won’t help allay fears of a slowdown. Nor will they do much to dispel the notion that Xi’s strict COVID policies and new outbreaks pose an additional threat to the world’s second-largest economy.

Industrial output for July rose 6.4%. Consensus wanted 7.9%. Fixed asset investment was 10.3% (versus an estimated 11.3%) and the surveyed jobless rate was 5.1%, a tick higher from June.

Subdued consumer behavior may limit the extent to which red-hot factory gate inflation can be passed along. So far, pass-through remains very limited, even as core prices are rising at the briskest pace in 18 months. Monetary policy will likely err on the side of caution, especially considering the latest virus surge and the economic ramifications of Beijing’s draconian containment protocols.

The PBoC rolled 600 billion yuan of medium-term loans on Monday. The rate was unchanged, suggesting the loan prime rate won’t be cut next week. 700 billion yuan in MLF came due this month. Citic Securities analyst Ming Ming said China may increase OMOs in the coming days in order to meet short-term liquidity demands tied to government bond sales and tax payments.

{kind=link}

{kind=link}