Jackson Hole isn’t the only thing on the docket in the new week.

Jerome Powell’s remarks are most assuredly the focal point, but market participants (those whose emails aren’t currently bouncing “Out of office” replies back to senders anyway) will be treated to a smattering of potentially useful data, including existing and new home sales, personal income and spending figures for July and the final read on University of Michigan sentiment for August.

All of that should be a modicum of interesting.

After overheating on its way into orbit, some wonder if the flaming-hot US housing market is now poised to burn up upon reentry. Housing starts disappointed last week, homebuilder sentiment is at a 13-month low and affordability questions are top of mind.

Read more: US Housing Conundrum Persists Amid Sky-High Prices

It’s hard to see this week’s numbers altering the broader macro narrative, but the housing market encapsulates the pandemic. The rush to the suburbs reflected angst over cramped city life in the post-COVID world, which in turn raised questions about the downtown, urban ecosystems that support so many jobs. Now, those ecosystems appear as fragile coral reefs, bleached (figuratively and literally) by the virus, their fate uncertain.

At the same time, record-low mortgage rates reflected Fed largesse, while the boom and subsequent bust in lumber prices (figure below) was a stark illustration of how supply/demand imbalances can play out in dramatic fashion over short windows.

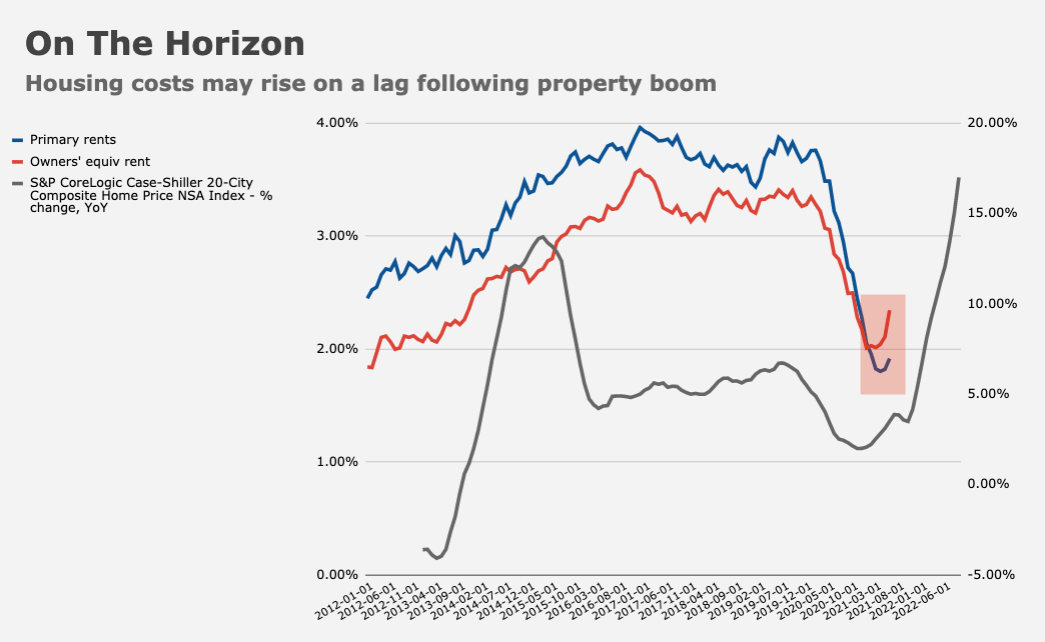

Finally, the surge in home prices (and not just in the US) is perhaps the most poignant illustration of the pandemic’s inflationary side.

Many expect to see follow-through to key inflation gauges on a delay (figure below), but I’d just note that while such things make for good analyst notes, the inflation is already here for anyone looking to buy a home.

It’s possible prices could collapse going forward. Some say that isn’t likely given still robust demand, but recent data pretty clearly suggests affordability is starting to chip away at sentiment.

Speaking of sentiment, the final read on the University of Michigan survey will be closely scrutinized. Recall that the headline gauge abruptly cratered to a decade low in the preliminary read, causing considerable consternation among market participants. Long story short, consumers are concerned about the Delta variant and inflation.

BofA downgraded their outlook for the US economy last week, citing a “speed bump.” “We are allowing the data to speak,” the bank’s Michelle Meyer said, noting that Q3 GDP growth is “currently coming in at 4.5%, leaving annual growth to slip to 5.9% this year.”

She called the Delta variant “a large reason for the soft patch,” citing a “pullback in spending on leisure services.”

Meyer noted that weakness in consumer spending flagged by BAC aggregated credit and debit card data (the light blue line in the figure, above) was “confirmed by the Census retail sales report for July.”

And that brings us neatly to the forthcoming update on personal income and spending. Last week’s lackluster retail sales report seemed to underscore burgeoning jitters among consumers, consistent with the Michigan survey. Government data on income and outlays (the first monthly read of the third quarter) will ostensibly shed more light on the situation. If it’s similarly downbeat, we may have a problem.

For what it’s worth, BofA didn’t strike an overtly dour tone. “Once the Delta threat is reduced and this COVID wave subsides, we should see the return of pent-up spending for leisure services,” Meyer remarked. “Our baseline is that this is a speed bump due to the interaction of Delta and supply-side constraints [and] all signs point to strong underlying demand.”

So, I suppose we could say any pause in cabin fever-induced spending is merely “transitory.” Like everything else these days.

“Once the Delta threat is reduced and this COVID wave subsides, we should see the return of pent-up spending for leisure services,” I’m sorry but if you own a hotel, a spa, a theme park, or other similar leisure time attraction, the revenues lost to COVID will not be recouped from “pent-up demand.” Capacity cannot be expanded to accommodate that which was “missed.” Leisure services are a perishable commodity and lost sales can never be recouped. One can get back to “normal” perhaps, but what was lost is lost for good.

+1

Also, imo it’s very optimistic to expect the current Delta-induced Covid wave to subside.

So far way too many vaccine-hesitant folks are doing their best to make sure Covid is here to stay