It probably won’t surprise you to learn that SocGen’s Albert Edwards isn’t surprised by the bond rally which, to let the financial media tell it, remains a total mystery.

“The collapse in the economic surprise index… together with the increasing threat of imminent tapering – which usually leads (perversely) to falling bond yields – leads me to think that the US bond market rally is actually wholly explicable,” Edwards wrote, in a Thursday note.

US 10-year yields hovered around 1.20%, some 55bps off the 2021 highs (simple figure, below).

I suppose I’d note straight away that there really was no “mystery” behind the recent decline in long-end yields. Market participants have debated this for months and the explanations are by now pretty clear.

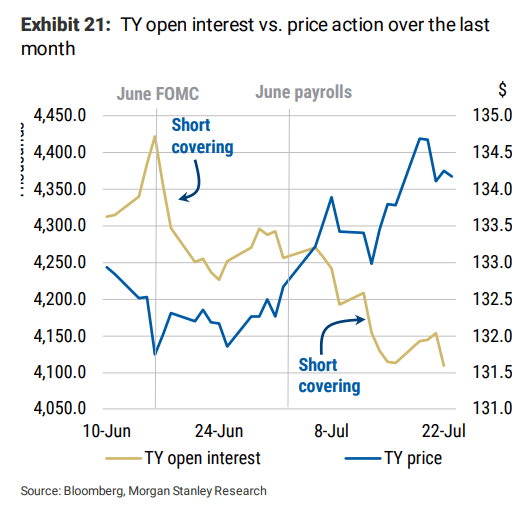

Positioning unwinds were a big part of the story post-June FOMC, but the price action was mistaken for a growth scare. The Fed’s hawkish pivot prompted some to suggest that a policy mistake might be afoot. The idea, generally speaking, was that the Fed was poised to abandon average inflation targeting at the first sign of the very “overshoots” they explicitly said they were prepared to countenance. That, in turn, raised the specter of preemptive tightening, prompting the market to bring forward the expected drag on medium-term growth.

The veracity of that narrative was questionable. The curve was already flattening and in all likelihood, the knee-jerk reaction to June’s hawkish pivot simply tipped the proverbial dominoes leading to a prolonged positioning washout/squeeze, which then turned the “growth scare”/”policy mistake” stories into self-fulfilling prophecies. The spread of the Delta variant provided a plausible macro justification for the price action.

“We think positioning has magnified the decline in yields and has been one of the key reasons why Treasury yields broke their range to the downside,” Morgan Stanley said.

“US real yields remain parked near all-time lows, as nominal yields have ground lower on the big multi-month, bull-flattening squeeze of shorts and duration underweights, but against breakevens staying parked at multi-year highs effectively since late March,” Nomura’s Charlie McElligott wrote Thursday, adding that “the longer USTs stay firm in this new ‘lower yield’ range, we continue seeing the positioning landscape shift.”

CTAs, for example, are “capitulating out of legacy ‘shorts’ into outright ‘longs’ in EGBs,” Charlie went on to say, before describing “massive covering in bellwether 10-year USTs.”

Nomura’s CTA model showed the aggregate net exposure across G-10 sovereigns is back to January levels (figure above).

We also now know that the dramatic surge in yields at the beginning of the year was probably attributable (at least in part) to Japanese selling. So, Q1’s bond selloff wasn’t all “reflation” optimism and fiscal stimulus. The bond market, for all its purported prescience, often lies.

Read more:

All of that said, there are now very real concerns about what the rapid proliferation of the Delta variant might mean for growth.

“From event cancellations to consumer behavior, there are growing signs the Delta variant risks slowing the pace of the US economic recovery,” Bloomberg wrote, in a Thursday piece which cited BofA’s Michelle Meyer, who said the bank’s internal debit and credit card data shows spending “decelerated meaningfully” last week.

At the same time, more companies are delaying plans to bring employees back to the office, with BlackRock and Wells Fargo among the latest firms to announce changes to their timelines.

Eventually, what was a “false optic” growth scare could become real indeed. “The recent plunge in real yields to new record lows in both the US and Europe is screaming that all that is cyclical is not as healthy as the central banks and equity market would have us believe,” SocGen’s Edwards said Thursday.

Even if you include soft data, “economic surprises have now turned negative, fully supporting the bond rally,” he declared, in characteristically emphatic fashion.

Commenting on the eve of July payrolls, BMO’s Ian Lyngen and Ben Jeffery wrote that “the uptick in COVID cases linked to the Delta variant has complicated the matter of interpreting the data.” They added that “while the current episode wasn’t a complete reset to April 2020 in terms of dismissing the dated fundamental information, it will create a ‘pocket of irrelevance’ for Q3 data as the outlook readjusts to a delayed path of the resumption of normality.”

And what of the taper? Well, Edwards reminded folks that yields can fall when QE is unwound “because the ‘risk-on’ uplift to assets and the economy wanes once QE stops.”

The Fed will talk about talking about tapering for a decade, and most will believe them, just like we believed Yellen’s BS for a decade.