The July 2021 edition of Jerome Powell’s post-FOMC press conference series produced no shortage of amusing soundbites, depending on your definition of amusing.

To reiterate, Powell isn’t a world-renowned virologist, nor is he an economist. Technically, then, he isn’t qualified to weigh in on epidemics or economics in any official capacity, which is a problem considering he’s Fed Chair during a pandemic.

He does have quite a bit of experience making policy, though, and his CV belongs in the dictionary next to the entry for “impressive.” That means he’s expected to know something about everything, even when there’s no obvious connection between his experience and what’s under discussion.

Small children expect their parents to have all the answers irrespective of the problem. We forgive them for being naive because they’re children. It isn’t clear why adults would expect a lawyer to know about pandemics, and we can’t excuse ourselves by pointing out that we’re toddlers. Nevertheless, we persist.

“Can you hear me?” a reporter from Reuters demanded, dialing into another virtual presser. “Yes,” Powell said, flatly.

“Can you speak to how the recent surge in COVID factors into the taper?” she asked. And just like that, Powell was a doctor. Again.

“It’ll have health consequences for many,” he ventured, before elaborating. “What we’ve seen is that with successive waves of COVID there has tended to be less in the way of economic implications. We’ll see if that’s the case with the Delta variety.”

I’m not sure “variety” is the right word, but… well, he’s not a doctor.

“It’s plausible that people will pull back from activity,” Powell mused, in an effort to provide something in the way of insight despite the impossibility of the Fed having come to some different conclusion than the rest of us when it comes to what impact the Delta variant may have on America’s recovery. “It might weigh on the return to the labor market,” he added. “We’ll be monitoring it carefully.”

Equally asinine was Steve Liesman’s question. At every, single press conference, Liesman reaches for the impossible. He habitually asks Powell to provide precise forward guidance above and beyond what’s in the statement, a ridiculous ask that can’t possibly be written off to a lack of experience in Steve’s case. On Wednesday, he took it a step further, asking Powell to provide specific numbers on what counts as “substantial” when it comes to the threshold for tapering and liftoff. That’s like a reporter at a Pentagon briefing asking the Secretary of Defense to provide the media with the exact coordinates of all forthcoming military activities during a war.

“Let’s talk about maximum employment. There isn’t a single number that we can target,” Powell responded. “I can’t give you a set of numbers — a numerical threshold — I can’t do that.”

Because he has a decent (if clumsy) bedside manner, Powell elaborated. “I’d say we have some ground to cover on the labor market side. We’re some way away from having had ‘substantial further progress’ towards the employment goal. I’d want to see strong jobs numbers.”

Nick Timiraos at least came up with a thoughtful question, even as he, like Liesman, effectively asked Powell to deliver a bombshell. “In your view, has the rise in inflation this year met the threshold of ‘moderately exceeding 2% for some time?'” Timiraos wondered. He was trying to extract the Fed’s FAIT formula. Again, a ridiculous reach.

Powell took the opportunity to throw the market a bone. “The guidance you’re talking about is the guidance for liftoff. It really isn’t relevant now,” he said. “We’re clearly a ways away from raising interest rates. It’s not something that’s on our radar screen. We’re not at all near that point or anywhere near that point now.” (So, you’re saying we’re not close?)

He dispatched Timiraos by noting that the timing of taper is data-dependent.

Pressed by FT on whether inflation risks are tilted to the upside, Powell said that (and I think the extended quote is useful here),

If you look at the latest inflation report… essentially all of the overshoot can be tied to a handful of categories. Each of those has a story attached to it that’s really related to the re-opening of the economy. We have a very adaptable, flexible economy and labor market. [Inflation risks] are probably to the upside in the near-term.

For (at least) the second presser in a row, he indicated that one way or another, there won’t be an “extended period of high inflation.” Either it’ll be “transitory” or the Fed will cut it off at the knees.

Of course, not everyone believes it’ll be that simple. For example, Bloomberg asked if the Fed is prepared to raise interest rates even if the economy isn’t at maximum employment in the event inflation remains too high. The same reporter wondered if the Fed would hike while it’s still expanding the balance sheet.

To that, Powell emphasized that in the Fed’s view, the juxtaposition between labor market slack and high inflation is temporary. “This is a very strong labor market,” he said. “We’re clearly on the path to a strong labor market. It shouldn’t take that long in macroeconomic time to get there.” (“Macroeconomic time” is like dog years, only in reverse.) He cited the disparity between vacancies and hires which is, of course, at a record high.

“It’s not timely for us to be thinking about raising interest rates right now,” Powell went on to say, adding that it’s “not ideal” to hike rates while monthly purchases are ongoing (outside of reinvesting the proceeds from maturing assets), as that amounts to tightening and easing simultaneously.

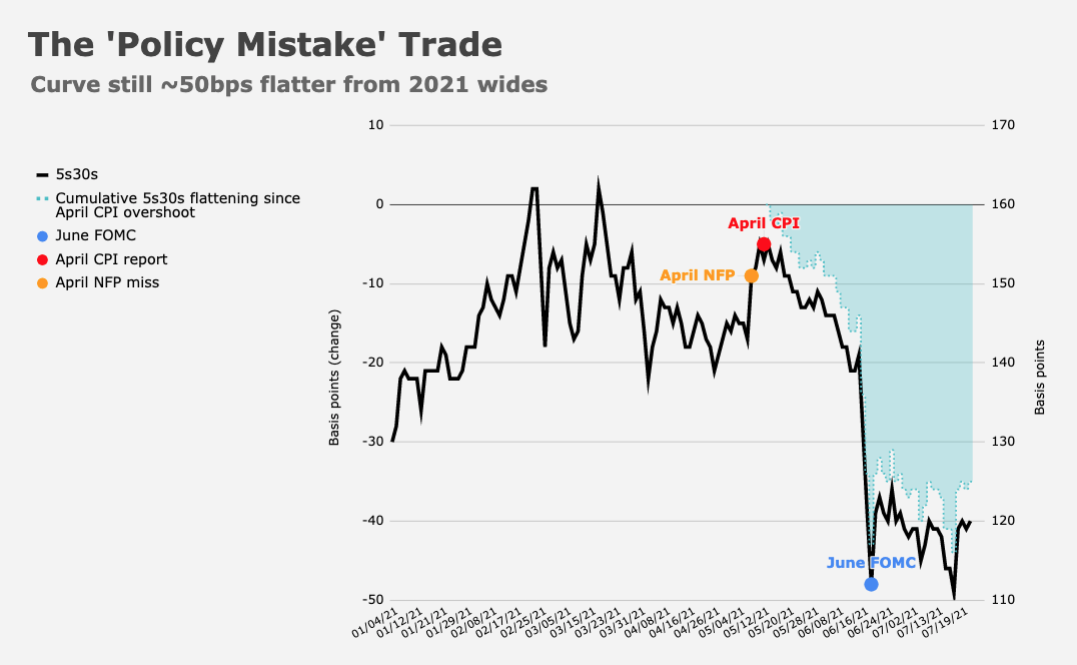

He was asked about market pricing which suggests some already fear the Fed might over-tighten. In other words, he was asked about the flattening in the curve since the last meeting and the possibility of a policy mistake. He said there’s no consensus when it comes to explaining the bond rally, but cited “sentiment around the spread of the Delta variant” and “so-called technical factors, which you can’t explain.” “I don’t think there’s anything in that that challenges our framework,” he remarked.

Asked about the “multi-speed” recovery around the globe, Powell slipped into ad hoc remarks about the virus. It was funny. Or, as funny as something can be in the context of a horrific global tragedy.

“As long as COVID is running loose out there, no one is safe,” Powell said. “There’s no reason these strains can’t keep coming,” he added. “One more powerful than the next.”

Who needs the CDC when you’ve got the Fed?

Read more: Fed Shuffles Words Around. Flags ‘Progress’ In QE Language

{kind=link}

“Macroeconomic time” is like dog years, only in reverse. 🙂

But I can’t believe you passed up an opportunity to make an analogy to “tightening and easing simultaneously.” Lay-up.

Powell is doing a pretty good job under trying circumstances. Interesting that the fiscal bills were not topic 1. They would be for me.

Why doesn’t someone ask Chair Powell whether 2% GDP growth isn’t just a function of a 2% annual inflation rate. Not a crazy thought, right? In which case the U.S. economy, in terms of real productivity, hasn’t grown at all since 2008.

slow claps

mfn: In my mind your conclusion is not far off. I have always felt that expected long run growth should be roughly 1+pop gr x 1+ infl. rate. So if inflation is 1.5-2.0% and population growth is something under 1.0% then my growth expectation would be 1.015 x 1.01 = 1.025 or 2.5% (to 3.0%). That seems about right. In real terms, 1.0%, ignoring inflation.