Generally speaking, a market that’s forward-looking is conceptualized as a good thing.

Forward-looking in this context is synonymous with what I’ll call “prescient efficiency.” It’s not just that equities (for example) price in currently available information, they also pull forward forthcoming information or, more formally, “expected future outcomes.”

Of course, markets are just collectives of people and headline-parsing algorithms, both of whom/which are fallible. People can miscalculate, misinterpret and act irrationally. Algorithms can also screw up, albeit for different reasons, some of which are related to the people who build them. (For our purposes here, I’ll leave aside that people can be conceptualized as algorithms too, raising a whole different set of questions about what it means when organic algorithms inadvertently impart their own deficiencies on the inorganic ones they create.)

As it turns out, making predictions about the future is hard (to paraphrase the old adage). The future isn’t knowable, but when we pull forward expected future outcomes by incorporating them into asset prices today, we effectively assume it is, or at least to some degree. The perils of that are obvious. If we’re not good fortunetellers, we lose money. In some cases, even future outcomes that seem like foregone conclusions turn out to be anything but. Take a look at GameStop or AMC, for example.

All of that is obvious. An under-appreciated risk, though, is that associated with correctly predicting the future and pricing assets to perfection in the here and now based on that correct prediction.

That’s arguably where we are at the macro level. That’s why you’re hearing so much recently about “peak rate of change,” whether in growth, profits, stimulus or even in anecdotal assessments, like those contained in BofA’s monthly Global Fund Manager surveys (figure below, for example).

What does this mean, exactly? Well, as Macro Risk Advisors’ Dean Curnutt put it in a recent note, it means that “‘As good as it gets’ is not all that good for a market that has pulled so much forward with regard to asset prices.”

That’s a concise way of conveying the point.

“In today’s mark-to-market world, everything is evaluated at the margin, in second derivative rate of change terms,” Curnutt went on to say, adding that “peak growth in both profits and the economy, coupled with peak central bank asset buying may leave investors clamoring for what set of goodies is to be distributed next.”

The irony (and Curnutt mentioned this explicitly) is that “goodies” in the form of stimulus are concomitant with economic downturns, which are often naturally accompanied by market drawdowns. That’s important when it comes to explaining why the “BTD” mentality has optimized around itself over time. We often speak about “BTD” derisively and also as though it’s somehow “unnatural.” But, as Curnutt wrote, “investors are the fortunate beneficiaries of monetary policy efforts to close output gaps [and] over time, a learning process is the result of these events, ultimately leaving asset prices higher than they otherwise would be in the absence of so generous a Fed.”

You could, of course, argue that the Fed shouldn’t be in the business of closing output gaps or, relatedly, that efforts to “smooth out” the business cycle are doomed to create ever large booms and busts. But I’d suggest that’s a different discussion. At the least, it’s a much broader discussion that requires us to move beyond how policy actually works and into a theoretical realm where policymakers adopt the strictest interpretation possible of the phrase “lender of last resort.” Lots of people say they want that. Few actually do. Bailouts are bad right up until you’re the one who needs bailing out.

One obvious risk when you consider all of the above is that monetary policy ends up “trapped.” The market has pulled forward robust growth, a V-shaped earnings recovery and trades on the assumption that the Fed will generally remain ultra-accommodative for the next two years (at least). If inflation persists, however, the Fed could be forced to choose between choking off the recovery with whatever counts as “aggressive tightening” in today’s world, or else risking the onset of “real” inflation and the un-anchoring of longer-term inflation expectations.

Recall that currently, the gap between year-ahead expectations and medium-term expectations is the widest on record according to some surveys (figure below, using The University of Michigan data).

If an inflationary mindset were to become entrenched, and the sky-high consumer assessments currently manifesting in the year-ahead outlook start to migrate to the longer horizon, the Fed may be forced into what would feel like an abrupt turn.

With everything priced off ultra-accommodative policy, that could be highly destabilizing. I’ve argued time and again that developed market central banks can never truly “normalize.” Curnutt wrote that “it’s nearly impossible to imagine a market-unfriendly Fed and that is indeed a large aspect of the risk.”

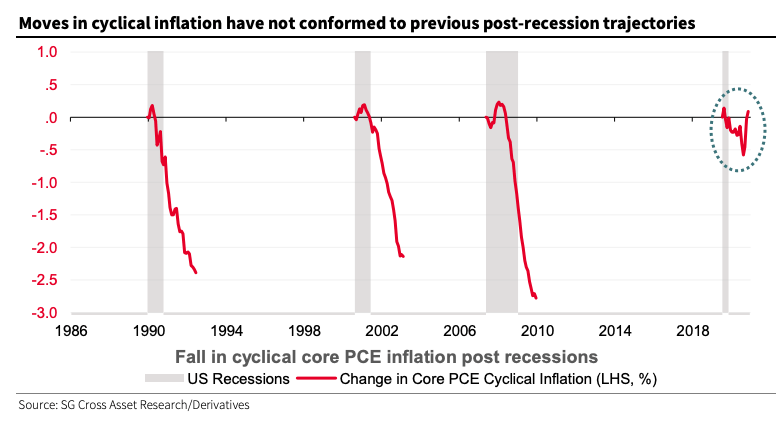

SocGen’s Jitesh Kumar noted recently that “a combination of timely monetary/fiscal support has managed to interrupt the ‘cycle’ in the US.” For example, he pointed to the cyclical component of PCE (derived by the San Francisco Fed).

“While cyclical PCE inflation saw a sharp decline in each of the previous three recessions, this was not the case during last year’s recession,” he remarked, explaining the figure (above).

Meanwhile, the CBO’s output gap estimates have undergone dramatic revisions.

“The old estimates suggested a new long cycle, as the output gap was not expected to be positive even as far out as 2030… in stark contrast to the latest estimates of a +2.5% output gap in Q3 next year,” Kumar wrote, adding that “if realized, this would be the highest output gap level since 1973 and would be consistent with a 3% unemployment rate!” The exclamation point is in the original. The figure (below), illustrates the point.

In the same note, SocGen’s derivatives team went on to say that “combined with the high level of inflation, this would suggest that both mandates of the Fed would drive them to hike rates sooner.”

“We suffer from the limitations of our imaginations,” Macro Risk Advisors’ Curnutt said, adding that,

Inflation risk today feels like subprime risk in early 2007. Then, the systemic financial sector leverage was in plain sight and the math around the implications of negative HPA on mortgage securities was well appreciated. But CDS on Wall Street dealers traded at 25bps anyway. Today, the consequences of inflation – through what it may mean for the Fed and for interest rates – and through the stock/bond correlation channel are well discussed and appreciated. But they aren’t priced.

I’ll leave it there.

I really would like our dear host to discuss the CBO output gap projections more. Also – I hadn’t looked at an output gap graph in a while and was a bit surprised to find out FRED graph had a positive output gap in 2018/2019.

Sure, the economy wasn’t doing badly and unemployment was relatively low… but, iirc, wage growth was still fairly meek and the labor participation rate still well below historical averages… in those conditions, it feels strange to say the economy had no more spare capacity… unless the industrial/service sector output capacity has been destroyed in recent years/the last decade?

There are times when simplification becomes an asset in devising a workable forward strategy or revealing an exit door that is not obvious. I appreciated the complexity and mystery of all this but did find myself seemingly trapped between a Yogi Berra quote or two and my legendary chainsaw that could run backwards. One thing for sure is the near future will bring even more than just one or two surprises that none of us anticipate. Glad the weekend is over !!

Two thoughts: 1) a guy named Werner Heisenberg (name sound familiar) was the first to propose that there is a limit to how well one can specify the position and momentum of a particle (e.g. an electron). One implication is that attempting to measure the position and momentum of the particle interferes with the properties of the particle. Applying this to markets, you can imagine that the act of forecasting the future behavior of markets interferes with that behavior. (Yeah, comparing electrons to markets is worse than comparing apples to oranges). 2) Isn’t it widely stated that the Fed and Treasury will tolerate or promote inflation in order to inflate away the national debt? And widely believed that this is the only way to manage the debt? (neglecting the MMT arguments for the moment)

Nice.

I agree, I thought inflation was the plan all along. It’s just finally showing up. I guess we need to decide if it is only supply constraints, or real wage pressures. We have to remember this disruption was epic in its intensity and duration. Wierd things will happen as the dust settles.