Those old enough to remember “vol-pocalypse” (so, anyone over three, which covers all institutional investors, at least half of Wall Street and around a quarter of Robinhood users), might recall that the implosion of the VIX ETN complex was preceded by an unprecedented stretch of market calm.

That prolonged quiescence is enshrined in market lore as “the short vol bubble.” Janet Yellen was the sponsor. The poster child was a former Target logistics manager famously profiled in The New York Times.

The trade unraveled on February 2, 2018, after the above-consensus average hourly earnings print that accompanied the previous month’s nonfarm payrolls report stoked inflation fears and underscored forecasts for multiple rate hikes just as Jerome Powell took the reins at the Fed. The bubble burst the following Monday. February 5, 2018, was a day that will forever live in infamy (figure below).

Analysts and investors conjured that episode on multiple occasions this year as bond yields rose and inflation concerns raised the specter of Fed tightening. The analogue wasn’t perfect, but it served its purpose.

Inflation is obviously top of mind and the reaction to the Fed’s hawkish pivot in June (i.e., the bull flattening in the curve and the unwind across various cyclical expressions in equities) was a reminder of how sensitive the market is to the notion that price and wage pressures in a hot economy could compel the Fed to tighten, even as “tighten” is now such a relative term as to be mostly meaningless.

There’s now another parallel with 2018. As Goldman wrote Friday evening, “there have been 179 trading days since the last 5% S&P 500 pullback.” The average is 94. The bank’s David Kostin noted that “this stretch… now ranks as the 15th longest period without a 5% decline in the last century.” More germane for our purposes here, it’s also the longest stretch since the 404-day run leading up to vol-pocalypse (figure below, from Goldman).

Viewed through that lens, we were due for a session like last Monday — and perhaps a few more in close proximity. Instead, we got a quick run back to record highs.

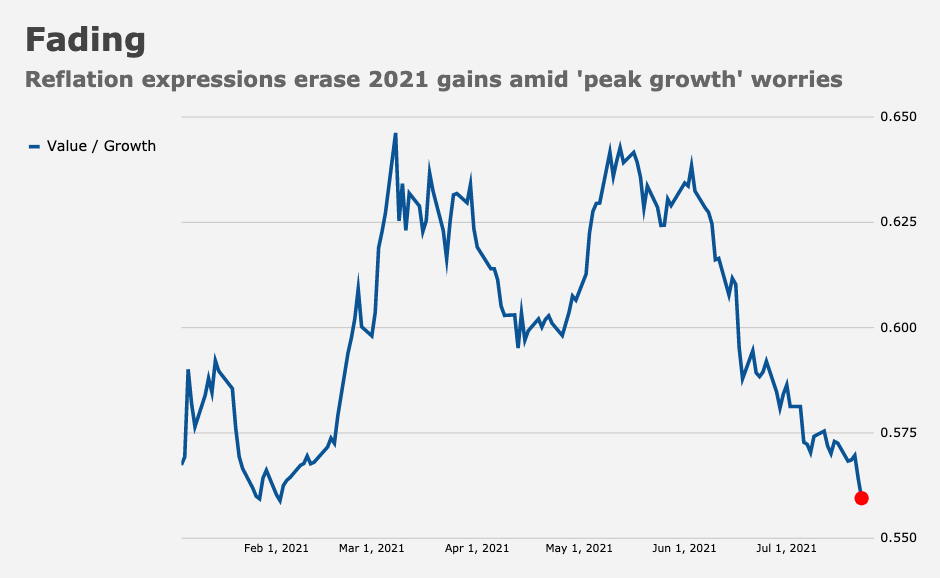

While it’s tempting to suggest the market is “ignoring” the perils inherent in the rapid proliferation of the Delta variant, that’s actually not the case. Bond yields, after all, are down ~50bps from YTD highs. And that’s bled over into equities, where various manifestations of the reflation trade have erased the lion’s share of their gains, if not in absolute terms then certainly in relative terms.

“Most of the risk premia and rotations linked to reflation have reversed YTD gains – cyclicals vs. defensives had a large setback and both value vs. growth and Russell 2000 vs. Nasdaq have reversed YTD gains, with US 10-year real rates nearing their YTD lows again,” Goldman’s Christian Mueller-Glissmann wrote, in a separate Friday note.

Although the rebound in stocks from Monday’s swoon helped some reflation trades find their footing, “the thrill is gone,” so to speak (figure above).

The irony is that mega-tech benefits in an environment characterized by falling bond yields and growth concerns. Because mega-tech comprises such an outsized share of benchmarks, a defensive tilt in equities can perversely manifest in record highs for the “broad” market, with the scare quotes there to indicate that “broad” is a misnomer.

“Facebook, along with Microsoft, Apple and Alphabet… have comprised ~55% of July’s S&P 500 gains, about two-thirds if Amazon is included,” Bloomberg’s Heather Burke observed on Friday.

And there’s more irony. “The gap between the S&P 500 earnings yield and the current 10-year US Treasury yield equals 364bps, above its 30-year average of 278bps and 19bps wider than it was two months ago,” Goldman’s Kostin remarked, on the way to reminding folks that the bank’s 4,300 year-end S&P target “embeds a forecasted 10-year yield of 1.9%.” If you keep the modeled growth and risk premium constant and insert a 1.6% 10-year yield instead, you end up with a model-implied fair value of 4,700 for the index.

“If our growth forecasts are correct, the recent market pessimism makes equity valuations appear even more attractive relative to bonds,” Kostin said.

This leaves one to ponder an almost comical scenario where equity investors can’t lose unless there’s another global lockdown. If growth worries persist, weighing on yields, keeping the curve predisposed to bull flattening and bolstering the fortunes of the same secular growth names that dominate the indexes, stocks hit records. If, on the other hand, bond yields rise and the reflation trade comes back as growth fears abate, stocks rise too, in a trade that’s part catch-up and part relief. “Although the S&P trades at a record high, some cyclical and virus-exposed pockets of the market remain underwater, creating an opportunity for tactical investors,” Kostin wrote. Goldman’s US Reopening basket, for example, is down 12% since the start of last month.

And don’t forget that mega-tech is all set to report their quarterly compendium of unfathomably large numbers. “With earnings on deck, tech’s domination has room to expand even more next week should FANG and friends post big earnings beats,” Bloomberg’s Burke went on to write, in the same short piece mentioned above.

[Insert lazy, generic ‘What could go wrong?’ punchline]

Subscriber since 2018, this is my favorite sentence of yours yet:

“And don’t forget that mega-tech is all set to report their quarterly compendium of unfathomably large numbers. ”

It’s just the use of language I’m celebrating here, nothing message specific.

I try

“ [Insert lazy, generic ‘What could go wrong?’ punchline]”

That was a great punchline I am still chuckling

I am also a fan of H’s use of language. He is an excellent writer which I am happy to say even if we disagree on a lot of things. One point I thought he might have missed was that ahead of the Vol Apocalypse, the Fed made substantial changes to their Severely Adverse Scenario relative to the 2017 version which might have sent shivers down the spines of those in charge of risk and possibly motivated them to buy a lot of VIX or downside protection so that they might escape the watchful eye of regulators when they reported their exposure on this survey.