“The bull case is ambiguity,” one popular strategist said this week.

I like that characterization of the current macro conjuncture.

It may no longer be the case that the risks are “skewed to the downside.” Indeed, you could plausibly claim the risks are now “more balanced,” as policymakers are fond of putting it. But really, nobody knows. The macro narrative is just one giant tautology: We can’t know what we don’t know. Not about frictions in the US labor market, not about how long inflation will remain elevated, not about the trajectory of the Chinese economy, not about the proliferation of the COVID “Delta” variant and not about much else either.

As long as nobody knows, the Fed (and other central banks, if they choose to avail themselves) has plausible deniability. BofA’s Michael Hartnett summed up the bull case in a dozen words: “We don’t know… Fed don’t know… Fed don’t tighten… market go up.” Ambiguity, he said, equals more liquidity.

Admittedly, I’m not enamored with “wow ’em with big numbers”-type analysis (as I’ve described it previously), but the color in this week’s edition of Hartnett’s “Flow Show” series does help underscore the rather overt nature of monetary financing in the US. I think it’s important to underline that dynamic, albeit for different reasons than most observers would cite for calling attention to it.

The Fed, Hartnett observed, is “spending $336 million every 60 minutes buying bonds” while the US government is spending $875 million every hour this year.

Dance around it as you see fit, but if you think spending must be “funded,” the bottom line is that we’re engaged in a ridiculous circular funding scheme. The US government is the sole legal issuer of US dollars, but we’ve decided we have to somehow “source” dollars from without. Sometimes, that involves issuing “debt” which we then buy from ourselves via a bank intermediary with dollars we created. It’s manifestly silly.

Even sillier is the extent to which the people who lampoon monetary largesse are, almost as a rule, aghast at the idea of simply printing money with no offset. As if that’s somehow sillier than the idiotic process by which we conjure currency to buy an interest-bearing version of the same currency from ourselves, in order to “justify” expenditures denominated in — wait for it — the same currency. Just to prove how insane we really are, we later pay ourselves interest in that currency too.

Do me a favor: Read the preceding paragraph again. We may one day look back on that arrangement as one the most mind-bogglingly ridiculous (not to mention pathologically inefficient) schemes modern humans ever came up with. If you presented that plan to a middle school student who knew absolutely nothing about economics or monetary policy, she’d surely laugh on the way to asking why the government wouldn’t just print money and spend it.

In any case, US CPI is annualizing nearly 10% and core CPI almost 11% (figures below, from BofA).

There’s too much demand and supply is constrained, which is leading directly to price pressures. That’s an observable fact. But it’s important to note that both sides of the equation are hopelessly distorted by the pandemic.

Demand isn’t just robust “because handouts,” as it were. It’s robust because, for nine months, nobody was allowed to go anywhere or do anything, colloquially speaking. And supply chains aren’t merely swamped with demand, they’re trying to recover from what might fairly be described as the biggest shock since globalization became “a thing.” Think about this: Virtually overnight, the world was forced to sort out the implications of a head-on collision between “Just In Time” and a pandemic, all set against a trade war between the world’s two largest economies.

“We hear repeated missives that supply chains are about to be made more ‘resilient,’ but you don’t move from ‘just in time’ to ‘just in case’ just like that – and with just the right amount of inflation,” Rabobank’s Michael Every said this week. “You just don’t. And that’s before ‘just’ politics gets involved.”

If you want to talk about the spike in inflation, those are the dynamics that matter. Brushing all of that aside in favor of an explanation that imagines a (notoriously uninformed) citizenry with a few thousand extra dollars and a newfound understanding of policy dynamics, rapidly adopting an inflationary mindset which is translating into price pressures is, frankly, laughable.

The two explanations aren’t mutually exclusive, of course. They can co-exist and indeed, they overlap. The point is simply that without knowing when and, perhaps more importantly, how myriad pandemic distortions both on the demand and supply side will resolve, we’re compelled to default to a shoulder shrug.

BofA’s Hartnett went on to note that inflation has usurped COVID as the No. 1 tail risk among fund managers polled for the bank’s monthly survey. “Candidates for the next ‘fear’ [include] Fed impotence (not omnipotence), fiscal cliffs, recession [and] yield curve inversion,” he wrote.

Sticking with “fear,” Hartnett summed up the bear case in 15 words: “Pandemic, Price, Positioning, Policy, Profits equals negative Q4 GDP, equals negative Q3 credit and stocks.”

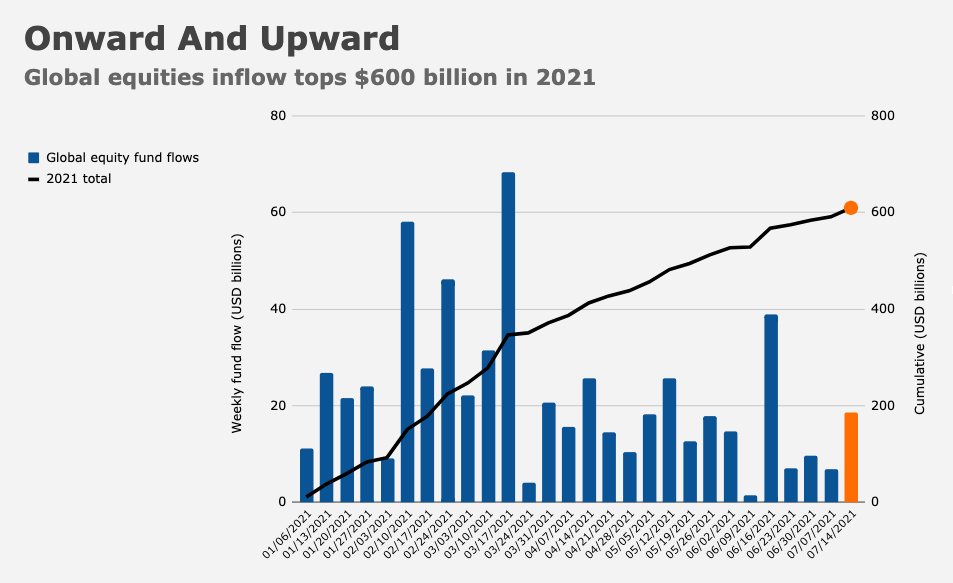

In the latest weekly reporting period, global equity funds took in $18.7 billion, the most in a month (figure below).

The total for 2021 now exceeds $600 billion.

BofA’s “Bull & Bear Indicator” is at 6.4, easing towards neutral after nearing “extreme bullish” territory in February.

The bank’s private clients have a 64.9% allocation to stocks. That’s an all-time high.

My go-to adjective for the process of how we fund our national budget with self borrowing-and then pay for that privilege- is……“ludicrous”!

It does seem to me that the US is well suited to grow ourselves out of this imbalance with some “intelligent immigration”. Our country should be able to dig deep, remember our roots (immigration) and get on with it.

I have some completely awesome first generation immigrants in my life, via my kids. Out of 8B people in the world, we should be able to find a 50M or so, that we can welcome and even provide a path for citizenship. Immigrants are fantastic at opening a little entrepreneurial business.

My two cents.

There is a lot of uncertainty and distraction. Inflation!? Bond yields?! Stimulus?! Covid?! Crypto?! Memes?! What does it all mean? What will the next data point bring? What is going on?

Step back and look at the big picture:

– Cyclical sectors rolling: energy, materials, heavy industrials.

– Secular sectors turning up: tech, discretionary, healthcare.

– Small caps rolling.

– Large caps turning up.

– Yield curve de-steepening.

– Value rolling.

– Growth turning up.

This is how markets act when the economic cycle is transitioning from early-cycle to mid-cycle.

Sure, each phase of an economic cycle used to take years rather than months. But we live in a speeded up world, I guess. Maybe trillions of dollars in stimulus acts like NOX in a “The Fast And The Furious” hotrod.