It’s easy to make inflation jokes these days. They write themselves.

But the punchlines feel cheap. Not “contrived,” exactly, just too obvious to be funny, let alone clever.

On Thursday morning, for example, I referenced one of the anecdotes from June’s ISM manufacturing survey on the way to delivering the following eye-roller:

The bottlenecks persist. The Fed says “transitory.” The Nonmetallic Mineral Products folks say “no end in sight.” But what do they know? They’re not PhDs.

Ba dum tss.

That kind of thing plays great on social media (and with “audiences” in general) but it’s vacuous. For executives in industries currently beset with labor shortages and supply chain issues, it doubtlessly feels like there’s “no end in sight.” And for that industry (or that firm), getting back to “business as usual” may indeed take quite a while.

But policymakers are concerned with the bigger picture. While it’s tempting to lampoon them for being out of touch (especially when you juxtapose their habitually benign assessments with “on-the-ground” takes from industry sources), don’t forget that it’s virtually impossible to be objective when you’re running a business. Today’s problems always feel like they’ll last forever. Assurances from a panel of technocrats are small comfort.

Don’t misconstrue my point. The anecdotes scattered across PMIs and media coverage are more than anecdotes this time. It’s not just “Bob in Wood Products” who had a hangover when he filed his survey responses this month. The figure (below) is indicative of business conditions across the US. Supply chain disruptions are real, and they’re pervasive. The same is true of labor shortages.

But before we summarily dismiss the PhDs for being dangerously aloof in their Ivory Towers, it’s worth parsing the actual numbers to determine how much hand-wringing is really warranted from an economy-wide, macro perspective.

Of course, that’s precisely what everyone has been doing for the past three months. But to say the jury is still out on what’s been variously billed as the macro question of our time (i.e., “Is it transitory?”) would be to woefully understate the case.

In a new note, Goldman’s Ronnie Walker took a fairly straightforward approach. First, he noted that if you look at the average annualized inflation rate since the start of the pandemic, core inflation is actually running at ~2.4%, still above the Fed’s target, but well below the 3.4% YoY print from May.

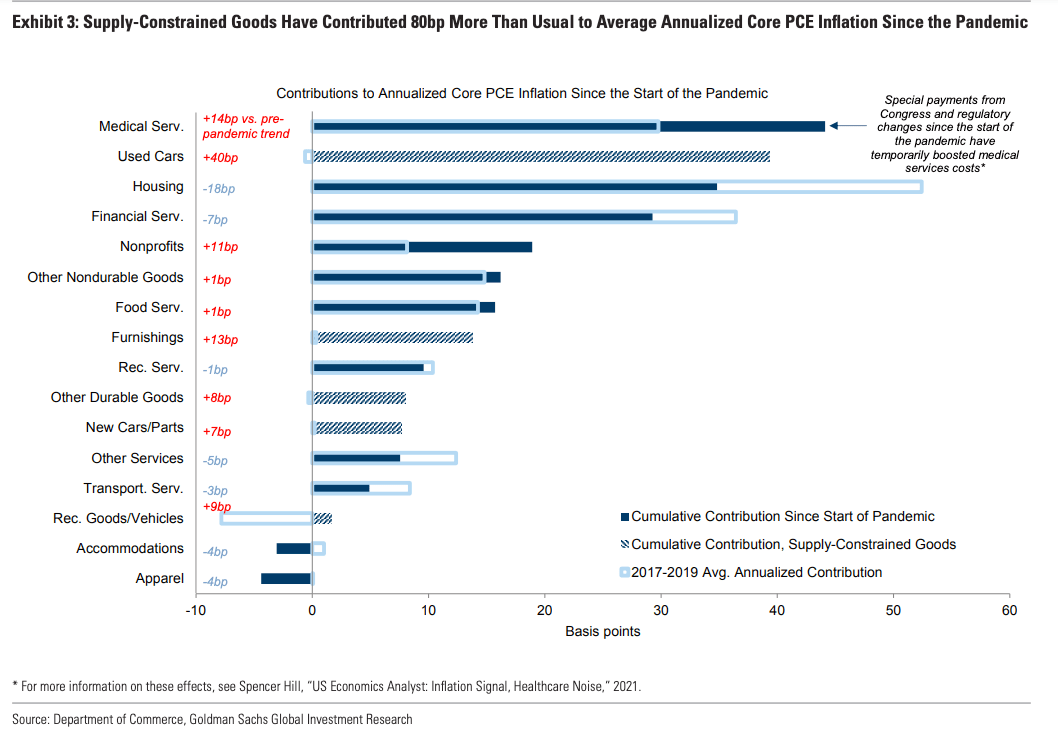

The crucial bit came when Walker took the average annualized inflation rate for what Goldman called “particularly supply-constrained goods categories” and combined them with their category weights in order to “show the component-level contributions to average annualized core PCE inflation since the start of the pandemic.”

The key point, from Goldman, is that “supply-constrained goods have contributed almost 80bps more than usual to average annualized core PCE inflation.” 40bps of that is attributable to used cars alone (figure below).

As the bank went on to write, “if the supply-constrained categories were instead running at their pre-pandemic rates, core PCE inflation would have averaged a more moderate +1.6% since the start of the pandemic.”

Admittedly, this process is vulnerable to that old joke about “If you omit all the bad things, everything is great.” But the overarching point is that if you take the annualized rate over the course of the pandemic (to smooth out the base effects), then look through the distortion from what everyone agrees are unsustainable surges in certain categories (obviously, used car inflation won’t annualize 27% forever), simple math suggests the inflation situation is nowhere near as harrowing as you might be inclined to believe.

That said, Goldman offered a caveat. “We expect a pickup in inflation in slack-sensitive categories like shelter, where average annualized inflation during the pandemic has been softer so far,” the bank said, adding that when considered with an expected return to trend for the categories currently overshooting, the net effect should be YoY core PCE that bottoms at 1.6% midway through next year, “before reaching 2% at end-2022.”

The average annualized rate, the bank said, “should remain modestly above 2% throughout.”

How convenient.

Ba dum tss.