Over the past two weeks, the assumption that the meme stock mania ended in the first quarter of 2021 was called into question.

Most obviously, a comically ridiculous rally in AMC (accompanied by an equally hilarious effort on the company’s part to capitalize) suggested that the factors which contributed to, for example, the Hertz saga, the summer 2020 tech melt-up and the GameStop fiasco, are still in play.

But it’s not just AMC. Clover Health took off this week, propelled by some of the very same factors.

Clover encapsulates quite a few of the trends associated with the post-pandemic market environment. Other than in passing, I’m reluctant to mention Chamath Palihapitiya in these pages. Suffice to say he represents a lot of what I’m steadfastly opposed to. Palihapitiya is a walking contradiction who’s fooled nearly everyone (including and especially himself) into believing that the various narratives he spins are somehow compatible. The loudest one in the room is usually the weakest one in the room in one way or another. And he’s pretty loud.

Part of Palihapitiya’s legend is bound up with that brashness, but there’s an inferiority complex buried in there, something he sometimes attributes to discrimination. Personally, I find his various “origin stories” (tales that help to explain how he came to be who he is) unconvincing. Everyone who’s ever achieved anything at all mythologizes themselves. I’m certainly no exception. And all origin stories are hopelessly embellished. Mine especially. But Palihapitiya’s personal anecdotes and self-aggrandizing have less explanatory power vis-à-vis his massive fortune than his CV. And that’s what I find somewhat unsatisfying. If you read his résumé, it’s not difficult (at all) to come to the conclusion that he’s a billionaire. You don’t need the anecdotes. Or the pitch. Or the legend. And he’s constantly pitching. And constantly telling the legend.

In any event, that’s a tangent. He’s as irrelevant to me as I am to him, the only difference being I’m compelled to know something about him by virtue of his celebrity and he’s not compelled to acknowledge my existence. I’d have it no other way.

For our purposes here, the important part is the Clover connection. “Before June, Clover saw its value split in half, with the once-hot market for companies brought to the market via SPACs… cooling off amid increased regulatory oversight,” Bloomberg wrote, adding that “the outspoken Palihapitiya has remained undaunted.”

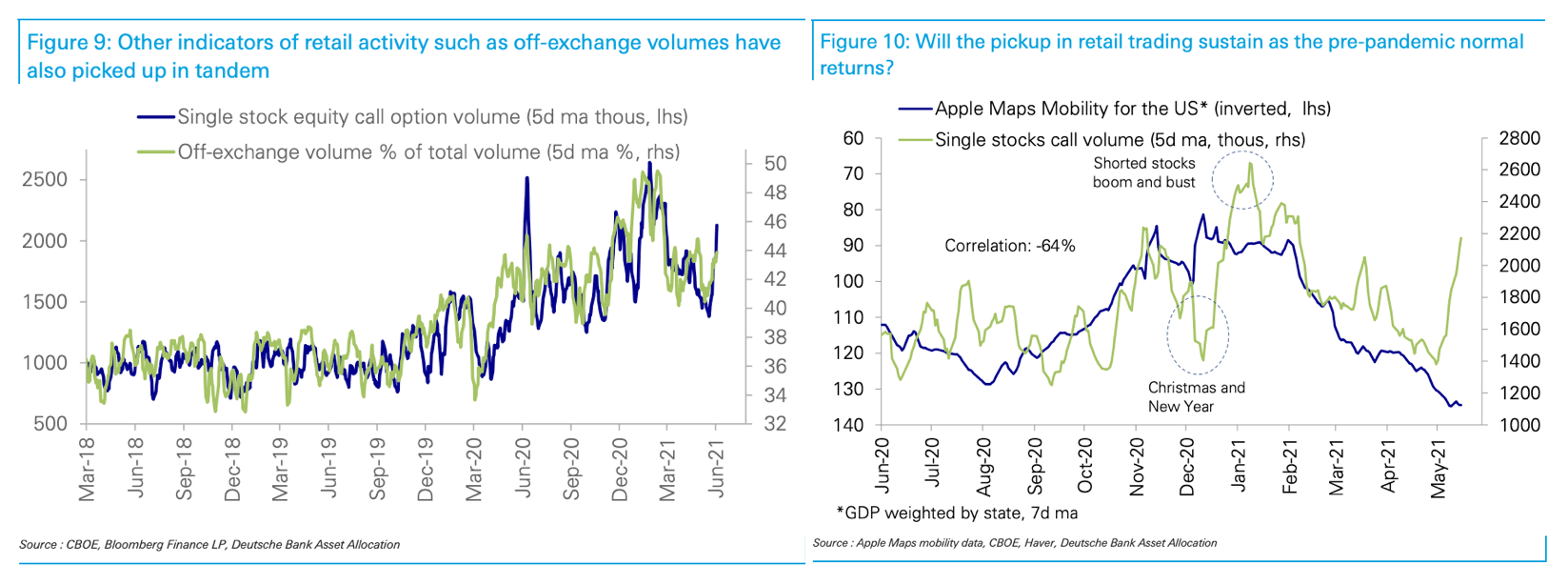

The above is critical context for the various metrics, measures and parabolic charts demonstrating that, very much contrary to my suggestion from the May 26 article linked here at the outset, the retail mania is alive and well.

Consider, for example, that Deutsche Bank’s measure of consolidated equity positioning is back in the 95th percentile. “The jump was driven largely by discretionary investor positioning and in particular a sharp increase in call volumes, which have previously been a good indicator of retail activity,” the bank’s Parag Thatte wrote.

Note on the right (charts above, from Deutsche) that the spike in single-name call volume is now detached from a measure of mobility.

“Indicators of retail involvement had been closely and inversely tied to measures of re-opening and mobility, which have continued to move higher,” Thatte went on to say, adding that “a key question going forward is whether the very recent pickup in retail trading sustains as the pre-pandemic normal returns, especially with an increasing return to offices, or the fading since the January highs resumes.”

Apparently, the absence of new stimulus checks, the resumption of sports (and sports gambling), the re-opening of bars and a return to work aren’t spoiling the retail investor party after all.

At the risk of coming across as unduly paternalistic (and some would say any paternalism is misplaced when it comes to talking about what other folks should and shouldn’t be allowed to do with their own money), some kind of common sense regulation or speed bumps designed to short-circuit the kind of dynamics that lead to reckless speculation by the retail masses may be necessary if these episodes don’t abate.

For one thing, it’s collusive, and while I certainly understand the populist appeal of letting everyday people engage in the same kind of activity that insiders and hedge funds engage in (almost as a matter of course), the inescapable reality is that a large percentage of the people who get swept up in these manias can’t afford to lose the money.

You could, of course, say the same thing about gambling in general and about playing the lottery, but at least there, most people understand that the odds are long.

Even if retail investors have gained a vastly better understanding of the playing field (they learned how to weaponize gamma, for example), they don’t seem to fully appreciate the extent to which engineering 3,000% rallies in controversial companies, many of which need capital, isn’t something that happens in a vacuum.

It’s not as simple as “sticking it to the shorts” or basking in headlines about some fund manager who, courtesy of Reddit, just had his (or her) worst month ever. For every “fat cat” who gets eviscerated in one of these episodes, another one gets a windfall.

Worse, everyone on the “other” side of this equation (from hedge funds to the C-Suite) is now in on the joke and keen to play the game. That means retail investors who get free popcorn on Wednesday get diluted on Thursday.

“The returns that we’ve generated—you can’t B.S. those,” Palihapitiya told The New Yorker, for a piece dated May 31.

“In March, he sold the entirety of his personal stake in Virgin Galactic, worth some two hundred and thirteen million dollars,” the same article noted, adding that “he might have needed the cash: A few months earlier, he’d reportedly acquired a seventy-five-million-dollar private jet.”

You crack me up Mr. H……in a good way!

Look at the debt! From zero to hero! Rights issue repays the debt. Now that is a return. Some people (distressed debt traders?), quietly, are making a killing in the background. Which makes the whole thing ironically amusing. I guess you may be able to tell whose next by looking at CC/CCC debt with small equity floats and short positions. Go to the moon and back Reddit