Over the years, one becomes almost completely desensitized to macro data billed ahead of time as the “most important read on [fill in the blank] since [fill in the blank].”

This is an admittedly off-the-cuff assessment (which is always perilous when what you’re saying is at least partially amenable to quantification), but I’d suggest that when it comes to the macro, it’s almost never the ones you expect that “get you,” so to speak.

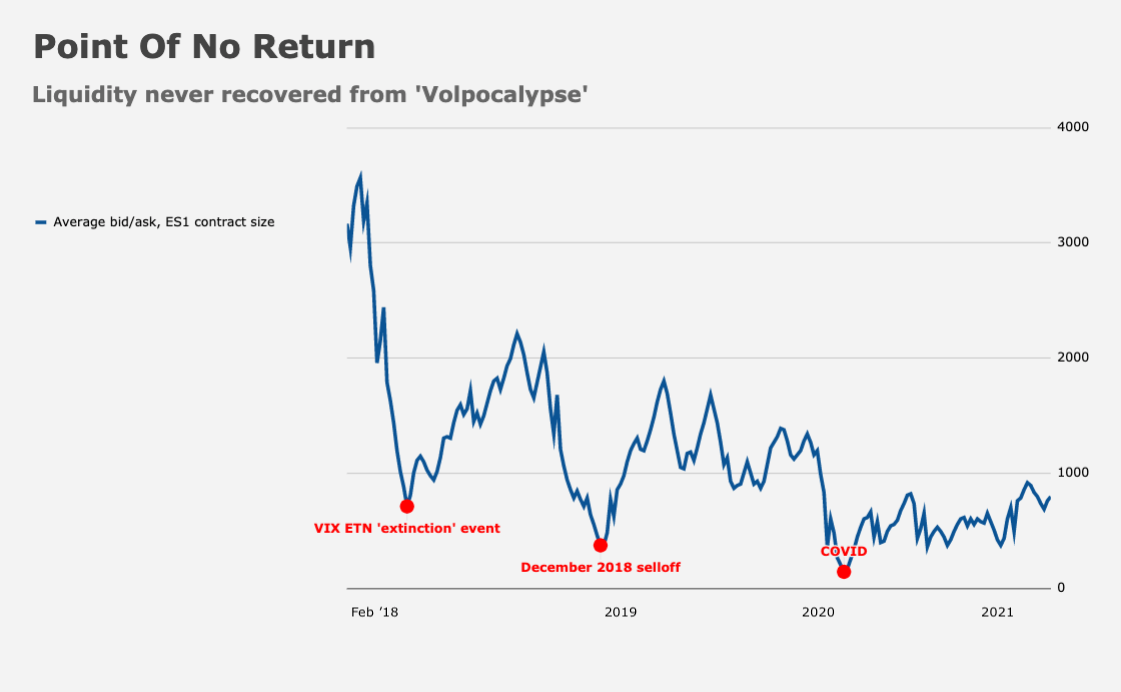

For example, in hindsight, it’s easy to understand why the above-consensus average hourly earnings print that accompanied the January 2018 nonfarm payrolls report was destabilizing. And the prospect of an AHE overshoot did have markets nervous that week. But I don’t remember anyone explicitly suggesting that a hot read on wage growth might dynamite the Jenga tower teetering in the VIX ETNs (figure below).

That’s not a perfect example because, again, there actually was quite a bit of consternation at the time around the possibility that data overshoots could make the incoming Fed Chair (Jerome Powell was just beginning his tenure) even more inclined to rate hikes at a time when the Trump tax cuts risked overheating the economy.

Then, as now, yields were rising, stocks were perched near record highs and market participants were concerned that strong data could force the Fed’s hand.

The point is just that headed into that fateful jobs report, you’d have had a difficult time finding someone willing to suggest that the market was staring down “the most important AHE print in at least a decade” and that an upside surprise might collapse the short vol bubble on the way to blowing up the entire VIX complex.

You’re reminded that market depth still hasn’t recovered from that event (figure below).

I bring this up for obvious reasons. May CPI, due Thursday, was touted not just as the most important read on inflation in recent memory, but in fact as a kind of defining, make or break moment for the entire global economy.

Another upside surprise might suggest the US has entered a high inflation regime, with implications for the viability of the current policy mix, characterized as it is by an experiment in almost overt monetary-fiscal coordination. A cool print, on the other hand, could bolster the Fed’s “transitory” narrative at a critical juncture — the June policy meeting is on deck and the White House is pushing an ambitious domestic agenda over shrill inflation warnings from Republicans and some Democrats.

A rather glaring supply/demand imbalance in the labor market is ammunition for Joe Biden’s critics. Another scorching inflation print would doubtlessly be cited by the same detractors as evidence that policy is headed in a dangerous direction. Infrastructure negotiations are predictably fraught. The data needs to cooperate for there to be any hope of bipartisanship when it comes to additional big spending.

Meanwhile, Treasurys are in the midst of a counterintuitive rally, which makes this all the more amusing. 10-year yields dropped below 1.50% on Wednesday and 30-year yields hit multi-month lows. “Investors appear to be backing away from the reflation trade precisely at the moment of greatest risk that the realized data catches up with expectations,” BMO’s Ian Lyngen and Ben Jeffery said.

10-year breakevens are down markedly from the highs (figure below).

“Inflation was not limited to COVID-impacted sectors [in April], which we took as a signal that supply constraints were more pervasive than originally believed,” BNP remarked, adding that in their view, there’s “more room for inflation to run in [those] sectors, while we could also see a slower but more sustained upward momentum in other categories.”

I’m inherently biased against the notion that May CPI is “make or break.” For one thing, the Fed isn’t going to react to May’s data. Two hot prints wouldn’t make a trend. Two would be more of a trend than one, but it’s not going to prompt policymakers to hit the panic button, especially when their stated goal is to engineer above-consensus inflation (that seems to still be lost on too many market participants — they are actively, openly, explicitly trying to get inflation to overshoot their target for a sustained period.)

More to the point, though, it would take a lifetime to catalogue all the ostensible “make or break” prints that have come and gone without making or breaking anything, and it’s no accident that the more hype a given data point receives ahead of time, the less it seems to matter when it finally comes in. After all, the longer everyone spends obsessing over something and tweaking their positions, the less scope for things to go haywire.

And yet, because of the interplay between monetary and fiscal policy and the extent to which both are unquestionably at inflection points in the US, you’d be remiss to completely ignore the potential for a game-changer to come calling, if not this week then sometime soon. Like the AHE print that toppled XIV in 2018, it’ll probably be something tangential — perhaps not the one that everyone flags ahead of time as the live grenade. (Ironically, AHE could very well be a land mine again given the current environment.)

While the hype around CPI may prove to be just that, there’s no denying that the stakes are extraordinarily high for fiscal and monetary authorities. If this experiment goes wrong, we likely won’t get another shot at it until something else comes along and forces the issue. Unfortunately, as we saw in 2020, events that force the issue usually aren’t pleasant.