Is enthusiasm for one of most spectacular equity rallies in recorded history waning, or is it just summer? (It’s not officially summer yet, but it feels like it, at least from where I’m sitting.)

That’s an admittedly glib question. But some indicators suggest sentiment has, at the least, moderated, while flows data tells a similar story.

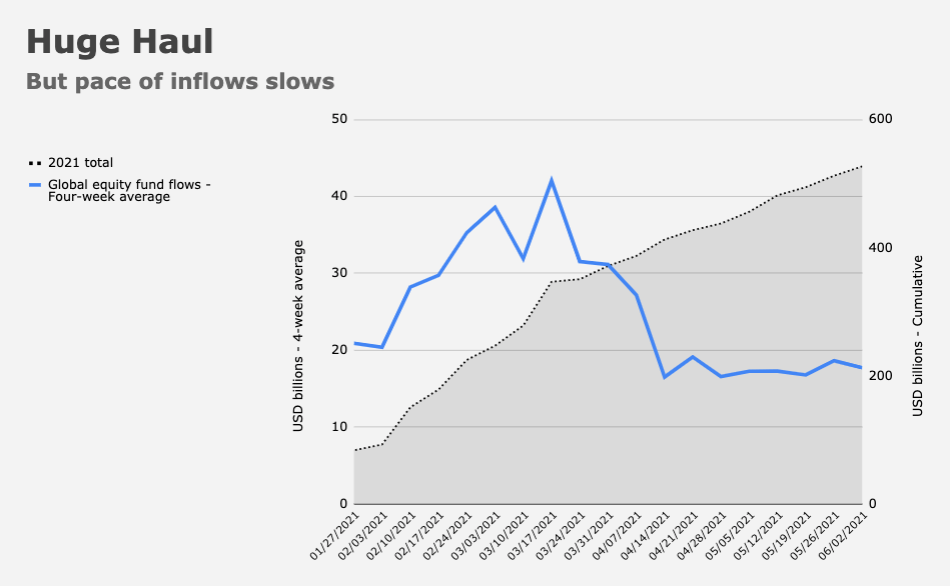

It’s no secret that inflows to global equity funds in 2021 have approximated a veritable tsunami. Last week’s $14.7 billion haul took the YTD total to more than $527 billion. However, the pace has slowed (figure below).

From a peak above $40 billion per week, the four-week average for inflows to stock funds has receded to less than $18 billion.

A look at domestic (i.e., US) equity fund flows tells a similar story. After peaking near $24 billion earlier this year, the four-week average is now less than $5 billion.

Clearly, there’s all manner of nuance. You can break the data down any number of ways. For example, last week saw the biggest outflow from tech since December of 2018 (the worst December for US equities since the Great Depression), while inflows into banks, materials and European shares were robust.

Lipper’s data showed another $385 billion fled high yield funds in the week through June 2. It was the fifth consecutive weekly outflow. Net flows to high-grade and junk funds were marginally positive as IG took in $1.72 billion (figure below).

“Back in December, if you asked the typical investor what the next big move would be for the S&P 500, two-thirds would’ve said ‘up’ [but] after two months of going-nowhere churn in the indexes barely half would say so now,” Bloomberg’s Lu Wang wrote, citing an Evercore ISI survey in which the proportion of respondents who said the next 10% move in equities would be higher was just 51%, down from 66% at the end of last year. Up or down is a coin toss now.

For his part, BofA’s Michael Hartnett described the bank’s pseudo-famous Bull & Bear Indicator as persisting in a “bullish holding pattern,” which he compared to the second half of 2017.

A Goldman sentiment indicator, which measures stock positioning across retail, institutional, and foreign investors compared to the past 12 months sat at just 0.4 on Friday. A reading over 1.0 indicates stretched positioning. It’s been months since the indicator was above 1.

“Much of the quiet in equity markets owes to the quiet in bond markets,” Macro Risk Advisors’ Dean Curnutt said. “It was only a month ago that stock markets were well catalyzed by upward movements in the ten-year yield and associated inflation breakeven level,” he added. “That has quickly settled down and markets right now are looking for [the] next catalyst.”

Indeed. And, as noted here on several occasions since Friday morning, it’s not entirely clear what that catalyst could be. May CPI is the obvious answer, but I’m not sure that’s going to do it. The monthly jump in the YoY core print for April was a 10-sigma event. And here we are rangebound on 10s. This week’s data docket should keep things a modicum of interesting, but as I put it late last week, “you need an actual, real catalyst to break the ‘stasis,'” as Nomura’s Charlie McElligott described the current drift in both rates and equities.

Still, there’s no shortage of ominous soundbites. Everyone is happy to hand out foreboding quotables. “There will be a reckoning,” Miller Tabak’s Matt Maley told Bloomberg, for the linked article (above).

There’ll be another Chicxulub Impact too.

Could the global minimum tax be a potential catalyst?

Glad you wrote this one H….I feel an awful lot like I am flying through the eye of a Hurricane , and it’s going to break in either direction SOON !