I wouldn’t say the data calendar is “heavy” in the new week, but there’s enough to keep things interesting.

Obviously, May CPI is the marquee print in the US. It’s easy enough to parrot the boilerplate narrative that says an encore to April’s scorcher could rekindle the bond selloff, but barring something truly extraordinary, the more likely fallout from another hot print would be scattered bets on a faster taper and the usual smattering of trades suggesting some market participants are keen to pull forward the first rate hike.

10-year yields are stuck in a sideways drift and vol has come down (figure below). With another NFP miss on the books (and no meaningful revision to April’s jobs letdown), it’s hard to imagine policymakers saying anything definitive about a taper timeline, let alone hinting at an accelerated schedule for hiking rates. The first six months of 2021 went by pretty fast — don’t let it be lost on you that Jackson Hole isn’t that far off. And neither is the September meeting. Clearly, the Fed would rather just wait it out. It would take a blistering run of data over the next several weeks to meaningfully change their penchant for “patience.”

“10-year yields have drifted to 1.55%, leaving the market in a position of bullish equilibrium – i.e. comfortably distant from the 1.77% peak to absorb any reopening concession and/or higher-than-expected core-CPI print without challenging the more constructive outlook,” BMO’s Ian Lyngen and Ben Jeffery said, adding that “the outright level of rates doesn’t sufficiently reflect a collective capitulation of short[s], leaving ample flexibility for yields to challenge the recent lows without the necessity of another fundamental trigger.”

The market will need to absorb $120 billion across 3s, 10s and 30s, while JOLTS, NFIB, claims and the preliminary read on University of Michigan sentiment for June are also on deck. Recall that May’s Michigan surveys betrayed palpable consumer consternation around the year-ahead outlook for prices (figure below).

“We’re seeing some inflation but I don’t believe it’s permanent,” Janet Yellen said, following the G-7 finance meeting in London over the weekend, where officials developed a framework that may serve as a template for a partial rewrite of the rules governing the global economy. “At least on a year-over-year basis [we’ll] continue to see higher inflation rates through the rest of the year — maybe around 3%,” she added.

Elsewhere, the ECB will update its economic forecasts and traders will listen for hints about the accelerated pace of PEPP purchases.

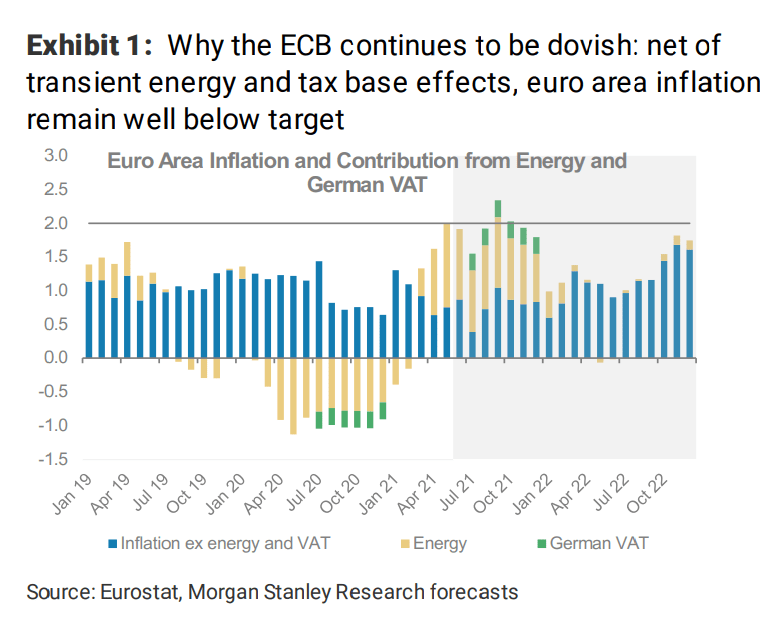

Inflation is technically at target (figure below), but I emphasize “technically.” It isn’t sustainable. Generally speaking, there’s much less in the way of concern that inflation in Europe will take off and not recede than there is in the US.

“With the strategy review not on the agenda until autumn, and decisions on what replaces PEPP also not likely until then, we see the ECB’s key focus at the June meeting as being on the pace of PEPP purchases: Should it buy a bit more, the same or less than the ca. €80-90 billion/month it currently buys?” Morgan Stanley wrote, in its preview.

“With a robust reopening under way, we don’t expect an increase, but we also see strong reasons for expecting no taper,” the bank said, citing tighter upstream financing conditions, risks to the recovery, a weak medium-term inflation outlook and “an absence of commentary from more hawkish members of the Governing Council” in the face of vocal doves.

The figure (below, from Morgan) speaks for itself.

Finally, UK monthly GDP is due Friday. As Bloomberg noted, “Health Secretary Matt Hancock said Sunday that it’s too early to say whether the June 21 opening can go ahead as the government continues to weigh the threat of a potential fresh wave of the pandemic.”

The Guardian provided a bit more color. “The transmissibility of the Delta variant, first identified in India, has been seen as a central factor to the decisions over whether to remove most remaining restrictions in England in a fortnight, with the decision due to be made later this week,” an article published Sunday read. “Estimates [say] the Delta variant could be anywhere between 30% and 100% more transmissible than the so-called Alpha variant first identified in Kent.”

I’d be remiss not to mention Bitcoin, which is grappling with all manner of competing headlines, including reports of Weibo shutting down crypto-related accounts (presumably in keeping with China’s reinvigorated crackdown), plans in El Salvador to make the coin legal tender and, naturally, more tweets from Elon Musk, who found himself on the receiving end of threats delivered via a painfully silly video in which Anonymous spent what felt like an eternity reading excerpts from mainstream news articles critical of Tesla. At one point, the video showed a clipping of a Wall Street Journal article. The paywall nag was visible.