Personal incomes fell less than expected in April, data out Friday showed.

Incomes dropped 13.1% last month as the impact from stimulus faded (figure below). Consensus saw a 14.2% decline. The range, from five-dozen economists, was -18.4% to -8%.

Personal spending rose 0.5%, in line with estimates, while real personal spending dropped 0.1%.

“The decrease in personal income in April primarily reflected a decrease in government social benefits,” the BEA said.

On the consumption side, current dollar expenditures on services were $112.6 billion, offset by a $32 billion decrease in spending on goods.

Happily for an economy that lives and dies by its services sector, the government noted that “the largest contributors to the increase were spending for recreation services and for food services and accommodations.” Those are the sectors that need to come back for the recovery to be sustainable.

The figure (above), shows the fading impact of social benefits.

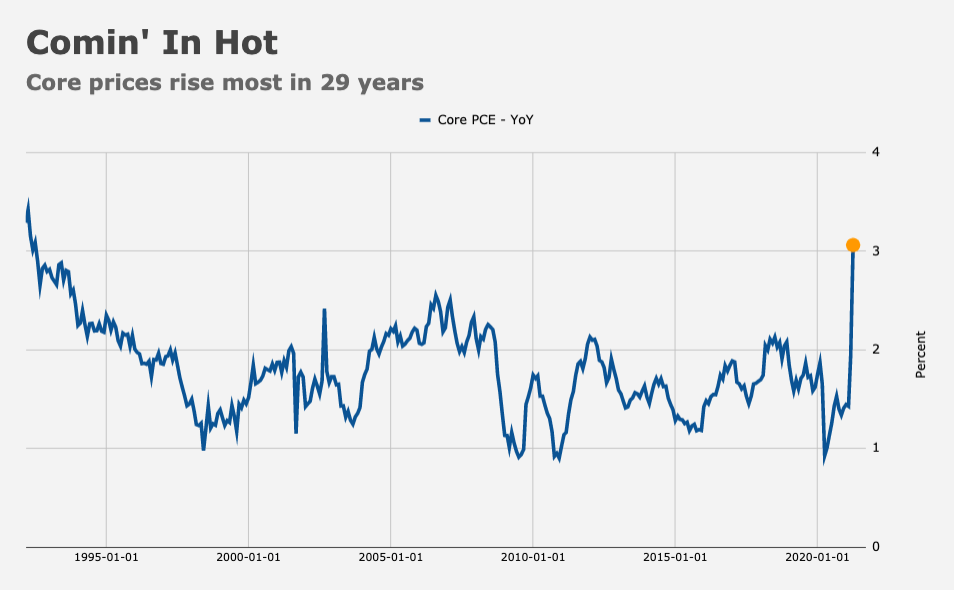

Of course, the headlines Friday will tout the largest increase in core PCE since 1992 (figure below). And, yes, I buried the lede, as I’m wont to do.

This was expected. Both the YoY and MoM gains (3.1% and 0.7%) were hotter than consensus, but economists were looking for 2.9% and 0.6%, so the actual prints weren’t wildly out of step. Headline PCE rose 0.6% MoM and 3.6% YoY.

“Sure, there are base effects, but [core PCE] has risen more than 1% in the last two months alone, so the current inflation dynamic is very real,” Bloomberg’s Cameron Crise wrote, adding that another plunge in retail inventories “augur[s] an ongoing mismatch between demand for goods and the supply that retailers have in stock.”

What you should keep in mind is that despite all the hand-wringing, everyone (including the people doing the hand-wringing) knew inflation was going to surge. So, lampooning the Fed’s “transitory” narrative is, for now, absurdly disingenuous.

Commentators, analysts and economists spent months explaining why prices were set to explode higher and also why the surge was likely to prove fleeting. I can cite countless such articles in the mainstream media, and you probably can too.

Now, the very same people purport to be surprised by the very same jump they predicted.

Sillier still is the notion (implicit in quite a bit of the color you might come across on a daily basis) that the Fed has somehow already been proven wrong in their “transitory” assessment.

It may well be that prices move higher in a sustainable way and that the Fed is caught behind the curve, forcing a quick policy pivot. And it may well be harder to rein in inflation than policymakers think. And sure, it’s possible that inflation spirals higher. Crazier things have happened (I’m told Donald Trump was president once, for example).

But remember: It is by definition impossible to say whether something is “transitory” until you have data spanning several months. That, in turn, means most of what you read about the inflation story in the here and now is purely for clicks, eyeballs and entertainment.

Would you have clicked on this article if the title was “Personal Incomes, Spending Mostly As Expected” instead of “Since 1992”?

I click on all Heisenberg articles.

Me too

In a world gone mad, yer so bad

I thought the bold print was the title of the Art Graphic.