Tech shares led gains on Wall Street Monday, and it’ll be no coincidence if growth stocks manage to rebound as breakevens come off recent highs.

The FANG+ gauge surged some 2.5% to start the new week.

Note that the index’s rebound over the past several sessions coincided with an easing in breakevens (figure below), which had reached 16-year wides.

Part of the story is commodities, and specifically China. Beijing is palpably concerned about the rapid rise in prices and is keen to do something about it.

A meeting between metal producers and the National Development and Reform Commission produced an amusingly forthright statement which grabbed a few headlines.

Beijing will “closely follow the trend in commodity prices, strengthen joint supervision of commodity futures and the spot market, show ‘zero tolerance’ for illegal activities, continue to increase law enforcement inspections, and investigate abnormal transactions and malicious speculation,” the declaration read.

China, the NDRC pledged, will “resolutely investigate and punish violations of the law, such as reaching agreements to implement monopolies, spreading false information, driving up prices [and] hoarding.”

That led to the usual debate over how much control the Party actually has. Regular readers know where I stand. China has a lot of control. It’s obviously true that Beijing can’t completely obviate the supply-demand imbalances currently bedeviling the global economy as the world tries to rebound from the worst downturn in a century. As demand increases, commodity prices should be expected to go along for the ride. And indeed they have.

It’s also true that China’s plans to reduce pollution are exacerbating price pressures. “That Beijing is also dealing with a problem partly of its own making is most evident in steel, where prices spiked to records after the government set targets on output curbs and ordered production to fall this year,” Bloomberg wrote. “Instead, output surged to record levels in April.”

But if Beijing says “Don’t do that,” anyone operating domestically caught doing whatever “that” happens to be, risks execution. It’s just that simple. I don’t pretend to know how the tension between i) economic trends Xi can’t control and ii) domestic activity he can, will sort itself out, but a directive from the Party is a directive. You either comply or you face the consequences.

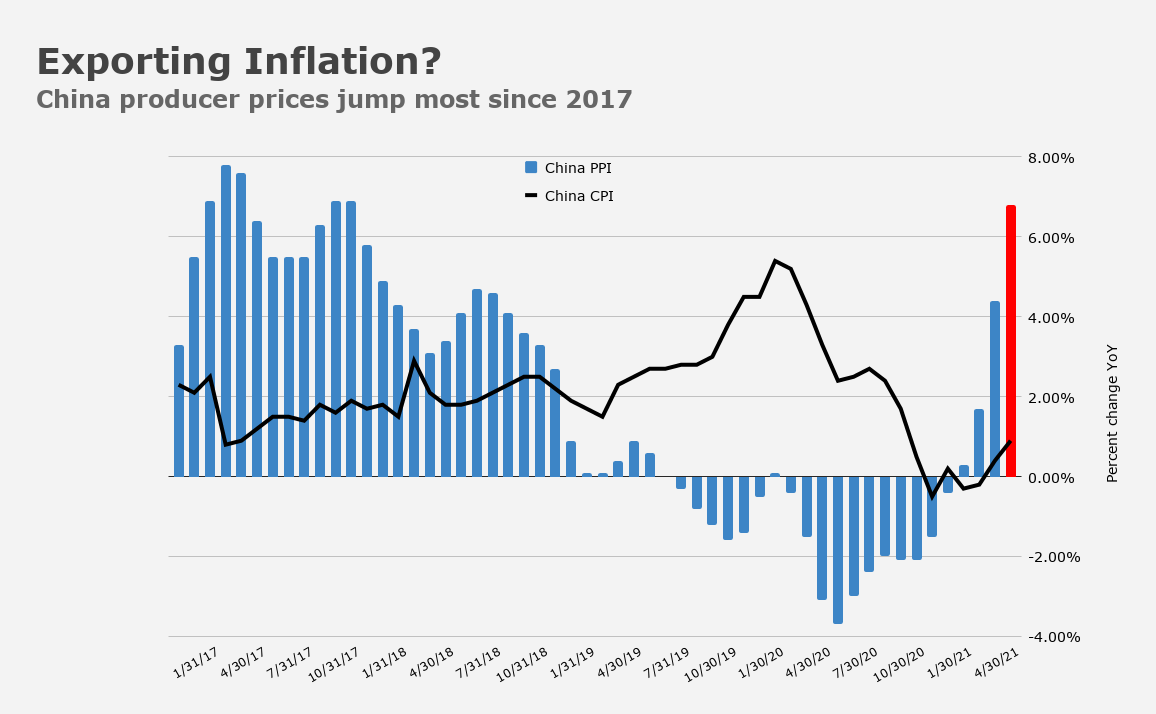

Recall that producer prices in China surged the most since 2017 last month (figure below).

In addition to concerns about exported inflation, there are also worries that higher factory gate prices could mean higher consumer prices domestically.

That would be bad news at a time when private consumption is still struggling to sustain a truly robust rebound (the figure below shows retail sales missing estimates for last month).

At the same time, Beijing is attempting to reboot the de-leveraging push, reining in credit growth even as market participants fret over record-high defaults.

Notably, copper ended higher on Monday, a development the media generally described as in “defiance” of Beijing’s express efforts to damp price appreciation.

SocGen’s Kit Juckes called the discussion around China, commodities and credit growth “more important” than the endless stream of cryptocurrency articles dominating the front pages this week.

“Chinese authorities are pointing verbal artillery at commodity prices,” he remarked, noting that when it comes to the yuan and commodities, “the former usually weakens when commodity prices fall, hardly surprising since commodity prices usually fall when the dollar’s strong.” The figure (below) illustrates the point.

But Juckes also wrote that in the event a slowdown in Chinese credit growth is perceived “as a harbinger of a weaker currency, plenty of people will extrapolate what it means for the dollar, and for the euro for that matter.”

Most of the above is just off-the-cuff musing (on my part), but I imagine this will serve as a handy article to reference in the future. It’s possible that policymakers are already spooked enough about inflation that efforts to lean against it could undermine assumptions around a commodities “supercycle” and possibly undercut a few pro-cyclical trades in the equities space too.

Late last week, in a note called “An Exceptional USD Needs A Hawkish Fed,” TD’s Mark McCormick said Jerome Powell and company are falling further behind other major central banks on the nascent normalization push. That “offsets some of the US economy’s strength since there’s a tug of war across drivers,” he added, in the course of suggesting that when it comes to a bounce in the dollar, “talk of talking about tapering probably won’t do the trick.”

That said, SocGen’s Juckes on Monday wrote that “concerns about China’s slowing credit growth, softer commodity prices, the ECB’s resistance to euro strength, and the possibility that the FOMC may get beyond talking about talking about tapering to actually doing something, are [all] dollar bullish.”

Just some talking points to ponder amid an inflation narrative which is almost sure to resurface above the fold once the crypto dramatics abate.