Lost in the whirlwind of inflation hysteria Wednesday was a notable downside surprise in China’s credit data for April.

Aggregate financing was just 1.85 trillion yuan last month, well below the 2.29 trillion consensus expected and near the low-end of the range.

New yuan loans were 1.47 trillion against expectations for 1.6 trillion (figure below).

This seemingly underscores Beijing’s commitment to reining in speculation and also the PBoC’s generalized aversion to a policy stance that risks exacerbating pockets of speculative excess.

As a reminder, the global economic cycle has become somewhat synonymous with China’s credit impulse over the years. Ironically, a pandemic that began on Chinese soil provided the impetus for a serious infrastructure push in the US. If Joe Biden’s fiscal proposals are enacted, it could mean that, at least for the next few years, the global economy will turn on the fiscal impulse in Washington rather than the Chinese credit cycle.

Early last month, reports indicated that Beijing instructed banks to maintain lending at around the same level versus 2020. If banks adhere to the PBoC’s guidance, the pace of credit growth would slow to a 15-year nadir (figure below).

Among other things, Chinese officials are concerned about speculation in the property sector. A series of directives aimed at curtailing such activity have met with mixed results.

April’s underwhelming credit growth figures are a reflection of the property crackdown and also reflect the impact of rising defaults, according to Nomura. Toss in the PBoC’s express intent to normalize policy now that the Chinese economy has recovered from the crisis, and you’ve got a recipe for a deceleration in credit creation.

That said, Nomura’s Ting Lu suggested that “room for a further slowdown in outstanding aggregate financing growth is quite limited as the PBoC needs to ensure that credit growth matches nominal GDP growth, which will surely be raised by higher commodity prices.”

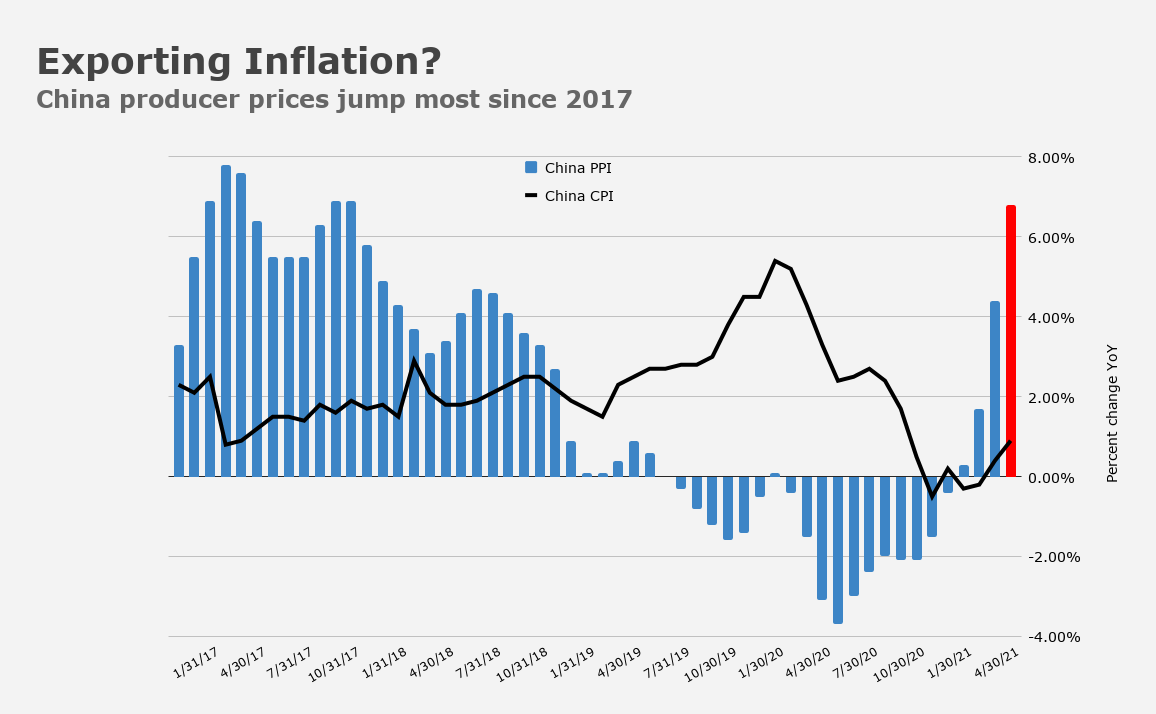

In the context of surging factory gate prices in China (figure below), slower credit growth could take some of the edge off global inflation worries. That’s a silver lining — I guess.

In addition to the headline misses on aggregate financing and new yuan loans, M2 growth in China missed by a mile, printing just 8.1% YoY for April against market expectations for 9.2%. It marked the most sluggish pace of broad money growth in nearly two years.

“The six-month pace of [total social financing] deceleration has picked up to somewhere close to that at the height of the deleveraging cycle back in 2017/18,” SocGen’s Wei Yao and Michelle Lam said. “This means that China’s credit impulse just turned negative.”

yep, as a large % of global growth and large economy, china’s credit impulse is key to watch and has abouta 6 month lag until it hits US PMI. Todays inflation reads were from China’s second large dose from 2020, late summer. In the US were trying to take the baton, but our stimulus is much more clunky and takes a while to get into the economy, except for the direct checks, which have already hit.

Theres a good chance we are seeing the ‘peak inflation fears’ right now. By July 4 were going to hope for 5% gdp in 2021…..and the ironic thing is, media says hoping to get to ‘pre-covid levels’…which were characterized by sub 2% growth and a Fed policy of pushing on a string.

I wonder how large a factor iron ore is in the Chinese PPI numbers. If the PRC authorities are looking to slow property investment, how much longer is the spike in iron ore prices sustainable?