All’s well that ends well. For those fortunate enough to own equities, that is.

If, on the other hand, you’re Joe Everyman or Plain Jane, and thereby comprise the 90% of Americans who together own just 11.5% of the stocks (familiar figure below), Friday’s monster rally on Wall Street was immaterial at best and totally irrelevant at worst.

What’s not immaterial (or irrelevant) on Main Street are higher consumer prices. And this week was all about inflation.

For market participants, the “inflation scaries” (as TD put it) subsided by the time the weekend rolled around. Rates were calm, and 10-year US yields ended just 5bps cheaper than they were a week previous.

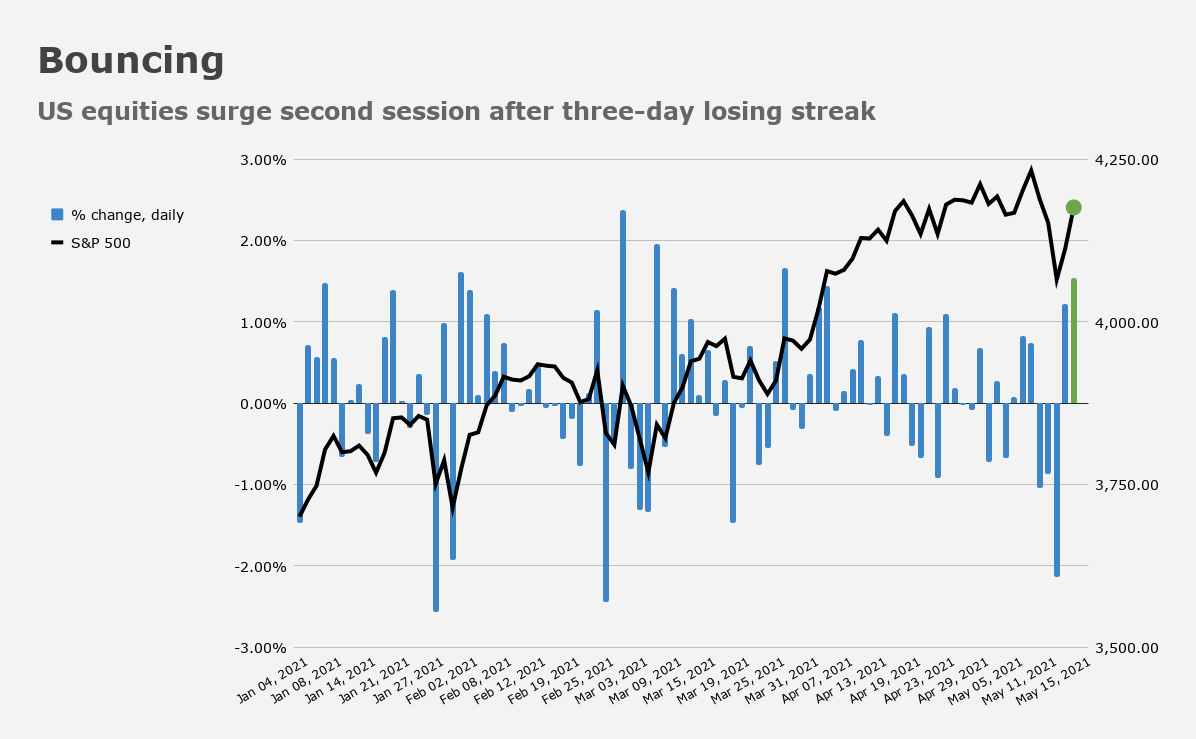

Stocks, meanwhile, surged in one of the best sessions of the year. The two-day gain for the S&P was nearly 3% (figure below).

Big-tech jumped more than 2% Friday. More narrowly, the FANG+ gauge rose almost 3%.

There’s a method to this madness. Sort of. After a multi-session purge, systematic positioning was “cleaner,” Nomura’s Charlie McElligott wrote, noting that sell triggers for trend followers are now well away from spot, while vol control had “little sell-flow left.”

Days of buy-sider net down “created fodder for a squeeze higher,” McElligott went on to say, adding that “equities vol selling into richness… is helping Dealers get less short Gamma in SPX / SPY [with] rich Vols offered aggressively into the move higher in spot, part of the trader ‘conditioning playbook,’ and a major reason why market snapbacks come so furiously in this day and age.”

Friday’s mammoth gains represented just such a “furious snapback.” But it wasn’t enough to save the week (figure below).

To be sure, there was a palpable sense of relief as the last hours of the work week melted away. Friday was everything Wednesday wasn’t. Stocks were sharply higher (versus sharply lower), gold was sharply higher (versus sharply lower), bonds were calm (versus weaker) and the dollar was lower (versus higher).

Despite the inflation jitters, Fed speakers are likely to remain steadfast in their contention that price pressures will prove transitory. Roll your eyes if you like, but when it comes to credibility, one could scarcely conjure a more ridiculous scenario than officials panicking at the very first sign of the realized inflation they explicitly said they wanted to stoke.

Sure, credibility will suffer if “transitory” turns out to be the wrong adjective, but nothing (nothing) undermines credibility more than the perception that the people who are supposed to be in charge are panicking. And an immediate about-face would certainly convey panic.

“The disappointing US employment report broadened expectations for the Fed’s monetary policy to remain accommodative for longer, then came the massive upside surprise on CPI,” SocGen’s Adam Kurpiel, Jorge Garayo and Ninon Bachet wrote Friday. “In that context, the June FOMC meeting will kickstart tapering discussions, but it’s hard to expect anything conclusive at this stage – perhaps some nuances and cautiousness.”

For SocGen, tapering hints “will most likely come no earlier” than Jackson Hole. There’s quite a bit of data between now and then. One might plausibly ask whether, by the time the Fed gets the “progress” it wants to see, it’ll be too late to stop it from “progressing” into something harmful. In other words: One wonders if the genie has left the bottle.

“Fiscal and monetary stimulus is peaking, and the acceleration in wages is ominous,” BofA’s Michael Hartnett remarked, suggesting that’s “a catalyst to simultaneously raise interest rates and cut corporate profits.”

“Inflation causes recessions,” Hartnett said, flatly. “That’s why policymakers have historically tried to control it.”

Everyone was waiting for the Fed to announce that they were thinking about talking about tapering, raises, and such – and here the market went and made the announcement for them.

Overshoot they may, but a man must admire that sort of economy of expression. The market once again gets its turn at writing the script.

A lot of the time, it’s a self-correcting mechanism. Which I guess is why so many people prefer it to a planned economy.

Acceleration in stock prices — not ominous

Acceleration in real estate prices — not ominous

Acceleration in commodity prices — not ominous

Acceleration in wages — ominous

“Acceleration in wages — ominous” For whom, exactly?

“Wall St.”, “the Market”, or shareholders. Consider the opposite condition: deceleration in wages. Who does that benefit?

I wonder if this announcement had anything to do with market action yesterday? Are we moving into yield curve control?

https://www.newyorkfed.org/markets/opolicy/operating_policy_210513

Nah. That was expected. They’ll keep doing that to make sure QE is lined up with the evolution of the UST market.