“Firm US growth and rising bond yields may keep the greenback supported over the short-term,” Goldman said, in the course of throwing in the towel on a six-month-old short dollar call.

The bank described it as a “tactical retreat” following “a choppy few months.”

Such are the perils of dollar shorts. There are myriad ways to make what’s often described as a “structural” bear case against the greenback. Typically, that effort entails hand-wringing over deficits (plural) and pointing to the dollar’s diminishing global status. On that latter point, note that “diminishing” is a relative term. The latest IMF data showed the dollar’s share of global currency reserves fell below 60% in the fourth quarter. That made for great headline fodder and it also produced a compelling visual (below).

Note, however, that the poignancy of that chart is heavily dependent upon one’s ability to manipulate the y-axis. Although most media outlets did include the figures for the dollar’s competitors, they didn’t generally show you the “other” chart.

It’s one thing to mention the numbers, but another to display them. The figure (below) gives you some context. This is a glacial process.

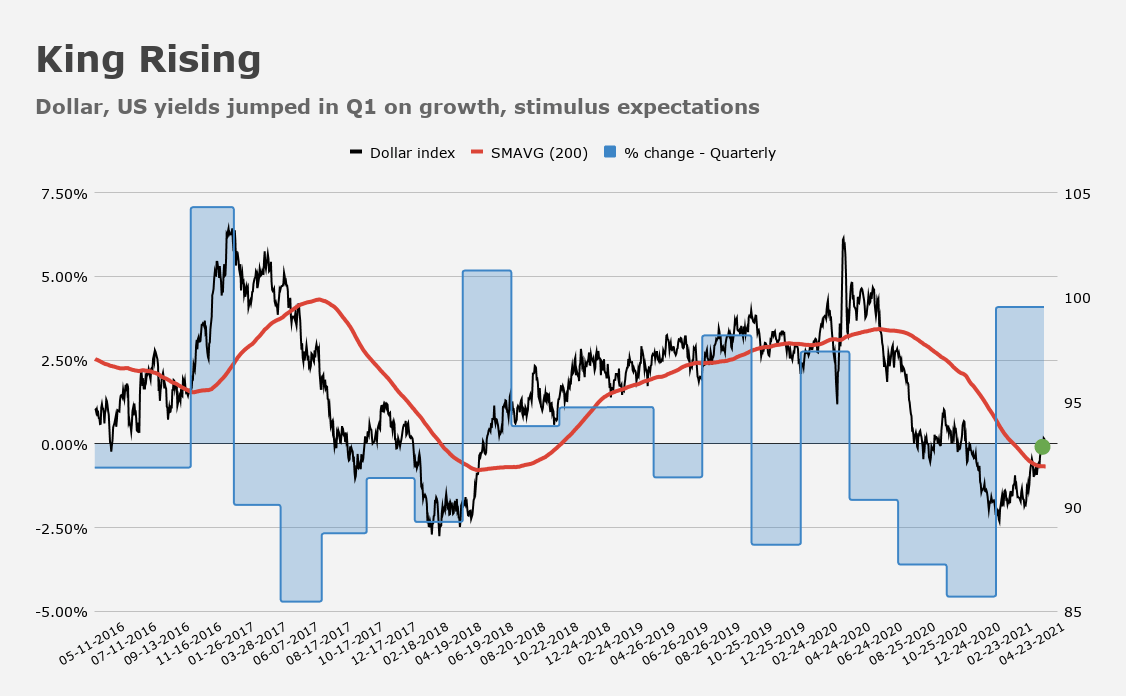

The dollar is coming off a good quarter. As US yields rose, rate differentials threatened to swing back in favor of the greenback. Further, the prospect of ongoing fiscal stimulus and an attendant economic renaissance prompted some to rethink bearish dollar bets.

As Bloomberg put it last week, “the climb in US yields relative to major peers helped to drive a surge in the dollar that ran counter to many expectations for 2021 as the currency turned from a prime haven at the height of market turmoil in March 2020 into a bet on US economic supremacy.”

Again, the dollar has a tendency to annoy forecasters by exhibiting various manifestations of a “heads I win, tails you lose” dynamic. There are multiple iterations of that. The Bloomberg quote describes but one of them.

Usually, elements of irony are present. For example, the same stimulus that ostensibly argues for dollar weakness on deficit and debt concerns pushed up yields and boosted growth expectations during the first quarter. Again, “heads I win, tails you lose.”

Another Bloomberg piece recognized this pseudo-quandary. “For investors scouring the currency universe for opportunities, America’s massive economic stimulus efforts and the staggering deficits they’ve produced, far from being an albatross for the dollar, have turned into a boon,” an article published late last month read.

Expectations for economic divergence almost invariably precipitate wider yield differentials, which in turn telegraph monetary policy divergence (even if Fed tightening is still years away). This can offset the perception that higher taxes and wider deficits are a reason to avoid US stocks and dollar-denominated assets.

“The rub here is that while the US does look exceptional, COVID normalization over time means the rest of the world will converge,” TD’s Mark McCormick said Monday.

“The USD level has now outstripped the pickup in non-US growth expectations,” McCormick went on to write, adding that the bank’s “view to start the year was partly based on the enormous gap between the green and black lines, indicating that the USD was too weak relative to the global outlook.”

Now that the gap has not only closed, but seemingly overshot, TD said there could be “room for a USD pause in the interim.”

But what comes after that? Remember: Doomsday debates about a prospective “dollar collapse” are largely pointless discussions. If the dollar really did “collapse,” the entire global financial system would implode too, while trade and commerce would grind to a halt, at least for a while.

Outside of that, a weaker dollar is generally a good thing. The world can become a very unfriendly place when the dollar surges. The corollary is that when the dollar is surging, something is usually wrong. Just ask March of 2020.

there are few things that could go wrong, wonder which one is linked to the ongoing green back rise?

Ugh, FX.

I can’t forecast FX and have never found a source of reliable forecasts.

I’m sure some can forecast FX, but I’d guess their work is very proprietary.

For investors sharing my plight, I think a sensible approach is simply to treat FX sensitivity as a random risk factor and control your exposure to that risk. Basically, try not to bet on the USD either long or short – focus on less enervating ways to make money.

Another is to keep casuality in mind. Does the world become unfriendly because USD rises, or does USD rise because the world becomes unfriendly? If you believe it is mostly the latter – granting that reflexivity means it has to be a little of the former too – then it is easier to keep one’s sanity.