The Fed may have threaded the proverbial needle this week, but the follow through suggested tension between the “new” reaction function and markets.

In simple terms, it’s going to take some getting used to, where “it” means the Committee’s commitment to engineering a period of realized inflation overshoots and eschewing rate hikes even as the economy heats up.

Jerome Powell’s remarks on Wednesday had a kind of “we’re serious about this” feel to them, and you could pretty easily argue that’s not yet priced into bonds. At the same time, it’s not obvious the market believes the Fed. 2023 will likely remain a point of irritable contention.

As noted Wednesday, there’s a risk in staying behind the market. Rushing to catch up could be destabilizing, even if you’re just “bridging the gap,” so to speak.

Of course, trying to parse and otherwise reconcile shifts in individual dots with the distribution of the accompanying economic projections is a fruitless exercise in tasseography. Even if you think you’re adept at divination, the fact is, forecasts are just guesses. And as Powell was keen to remind journalists during the press conference, it’s a fool’s errand to mischaracterize the dot plot. But everyone mischaracterizes the dot plot, in most cases on purpose. The result is an endless effort to “reconcile” market pricing and analyst forecasts with the Fed’s “guidance.” But the only real “guidance” is the outcome-based language in the statement. Because that’s not specific enough for markets (or analysts or journalists), an unhealthy dot obsession develops, and the Fed feeds it every three months.

The bottom line: The Fed doesn’t know where rates are going to be in two years and neither do market participants. It’s just the blind leading the blind, only because the Fed is often a slave to market pricing, it’s not always clear which blind man is in the front and which one is trailing behind.

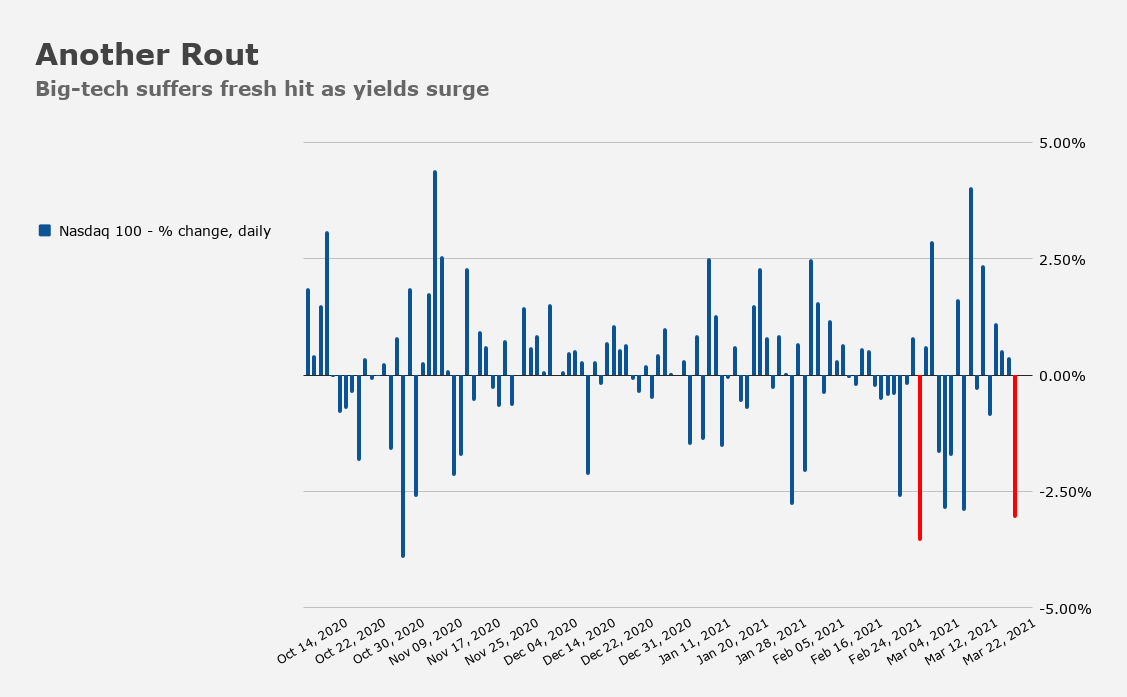

Treasurys sold off Thursday, and that weighed on tech. The Nasdaq 100 had its worst session (figure below) since February 25, the day of the disastrous seven-year sale.

Some folks likely experienced a little “diversification desperation” which is not uncommon when the dollar is buoyant, as it was on Thursday.

With bonds distraught and equities beset, there was nowhere to hide. Full disclosure: The figure (below) is crudely constructed and strips away any and all nuance, so it should be considered for illustrative and entertainment purposes only. But it helps make a broader point — namely that bonds may become a source of risk going forward as opposed to being a hedge.

If bonds also become a source of volatility, then you’re left to ponder what good they are. That is, if something doesn’t perform, increases volatility and yields next to nothing, why do you want it? Of course, if money is free and you can lever up, the calculus changes, but that’s a story for a longer article.

Recently, investors could count on energy shares to cushion some of the blow on days when tech underperformed. But not Thursday. Energy stocks were under severe pressure as oil went into a veritable death spiral, collapsing almost 8%.

“The oil market feels toppy,” PVM’s Tamas Varga said, calling the string of daily losses “not without precedent [but] an unusual phenomenon.”

I could be wrong, but I’d venture that’s not just “fundamentals.” Yes, there are stubborn concerns about vaccine rollout in Europe and Paris is headed back into a partial lockdown, but whenever the bottom drops completely out for crude, you can almost guarantee forced selling and mechanical unwinds of some kind were in play. Dollar strength obviously didn’t help.

“The jury is still out whether the current weakness is just a healthy correction triggered by a series of negative developments,” PVM’s Varga went on to say, adding that “immediate demand concerns caused by the stuttering rollout of vaccinations, halting the use of the AstraZeneca inoculation in several European countries and introducing tougher restrictions in France and in Italy as cases keep rising put oil bulls on the defensive.”

Whatever the case, crude’s losses added to the “nowhere to hide” feel on Thursday, as did a lackluster day for gold which was also hurt by rising US yields and a stronger greenback.

I’ll leave you with a non sequitur, albeit one that counts as a sign of the times. Lamborghini just had its most profitable year ever. During the worst public health crisis in a century, “an ideal model mix and the growing customization of products pushed profitability to the highest levels,” Stephan Winkelmann said, on a private video call earlier this week.

Now that’s bullish. If you know the badge.

This article makes a case for reducing risk by raising cash in portfolios

I went for a walk through a nearby shopping center, and parked there was a bright red monstrosity, a hulking vehicle reminiscent of a Humvee crossed with a Mercedes SUV, but with ultra-low profile tires and gold wheels. I looked more closely and saw that it was a Lamborghini, the ugliest Lamborghini ever made, I reckon. Do young boys sit in class idly drawing pictures of these SUVs, the way we drew pictures of the Lamborghini Countach when I was young? I guess Lambo and Porsche and Ferrari know their markets…and I reckon also that there are more people around now who have more money than they know what to do with.