GameStop and some of its Reddit-fueled compatriots may have collapsed, but that hasn’t necessarily derailed the trade in speculative or otherwise risky investment styles, and I don’t just mean Bitcoin.

As noted here on Monday afternoon, the Russell 2000 was the big winner of the six-day surge in US equities. Small-caps were up some 10% over that stretch.

Obviously, the gauge has benefited from the pro-cyclical lean in markets since November, but it has a quality problem which is getting progressively worse over time. Specifically, the weighting of lower-quality companies in the index is the highest going back at least to the financial crisis, according to SocGen’s Andrew Lapthorne, who last week observed that the trend was well established before the GameStop drama. (Not surprising given the economic backdrop.)

Read more: The Problem With The Russell 2000

In a new note out this week, Lapthorne observed that even as the WallStreetBets frenzy crumbles, “the surprise is that… performance in these speculative investment styles has held up quite well.”

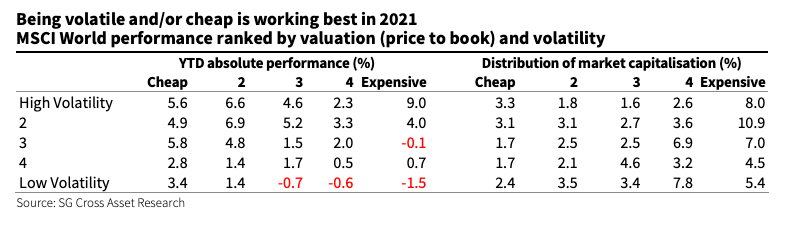

Indeed, when it comes to what’s worked in 2021, “being volatile and/or cheap” have been winning attributes. Conversely, the worst places to be (so far, anyway) are low volatility shares that came into the year expensive.

I hesitate to use the figure (below) because it’s apples to oranges in many respects. But it makes the point utilizing a readily accessible vehicle. Sometimes, it’s worth committing “chart crimes” if they better convey a dynamic versus a more technically “correct” visual.

Again, that’s not the best comparison, but it’s poignant, and that’s what I was aiming for.

Those steeped in the narrative will note that generally speaking, expensive, low volatility shares are synonymous with the yearsold “duration infatuation” in rates or, as Lapthorne puts it, “the companies that had done very well as bond yields fell.”

Now that the narrative has changed, curves are steepening, and breakevens are breaking out (even as nominals are rangebound), expressions tethered to the bond bull are faltering, especially by comparison to some red-hot pro-cyclical trades. In fact, those names aren’t just underperforming, they’re “losing money in a rising market” as bonds sell off, Lapthorne went on to say.

Now that the narrative has changed, curves are steepening, and breakevens are breaking out (even as nominals are rangebound), expressions tethered to the bond bull are faltering, especially by comparison to some red-hot pro-cyclical trades. In fact, those names aren’t just underperforming, they’re “losing money in a rising market” as bonds sell off, Lapthorne went on to say.

Whether (and to what extent) this can persist is really the question right now.

The above is couched in pretty specific terminology, but it’s really just a microcosm of the broader debate about whether reflation is here to stay, whether earnings have truly turned a corner, whether bond yields can continue to rise, and, at the 30,000-foot level, whether the global economic recovery is upon is, just around the corner, or merely a mirage that will disappear the moment we reach out to grasp it.