“On the one hand, the fact that a few day traders could cause such disruption is a little scary because it’s emblematic of the excess leverage and lack of two-way risk embedded in financial markets,” Morgan Stanley’s Mike Wilson wrote, in his latest.

He was, of course, referring to the GameStop saga. And he’s right. It is “a little” scary. It’s also “a lot” absurd.

As I put it last week, we’ve come a long way in a dozen years. I’m “old” enough to remember when “systemic” meant Lehman. Now, we’re using “systemic” in the same sentence as “GameStop.” It speaks to the media’s penchant for hyperbole, but also to the inherent fragility of modern market structure. Everything is merely metastable. An avalanche waiting for a skier’s scream, as Deutsche Bank’s Aleksandar Kocic put it years back.

But, as Wilson also noted, greed is a powerful thing. And it will overcome in the absence of forces strong enough to suppress it. “It looked like equity markets were finally ready to have their first meaningful correction in months, with most major averages falling 3-5%,” he wrote, of the tremor that accompanied the multi-standard deviation moves associated with the Reddit crowd’s offensive late last month. “With equity markets roaring back last week, it appears that greed once again has the upper hand over fear and the bull market is ready to resume in earnest,” he went on to write.

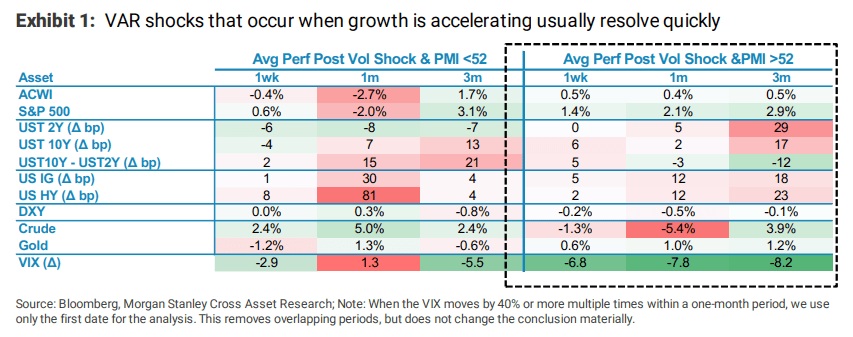

You might be wondering what usually happens after VaR shocks like that witnessed late last month. I’d note that this is becoming harder and harder to backtest because thanks in part to the fragility mentioned above, these events are becoming more and more anomalous over time. You can’t really “backtest” for a 13-standard deviation factor quake, for example. How many 13-sigma events do you imagine you’re going to find?

Wilson cites Morgan’s cross-asset team, which looked at VaR shocks during “growth acceleration phases” which is what the bank says we’re experiencing now, economically. They define such phases as periods when the ISM is above 52.

“With the ISM near 60, a quick resolution of January’s drawdown makes sense, particularly with the larger version of the COVID relief bill looking more likely,” Wilson remarked, commenting on the table (above, from Morgan). “It’s hard to imagine the ISM falling below 52 with so much stimulus and a reopening of the economy right around the corner,” he added.

As you’re likely aware, Joe Biden’s stimulus plan would be the second-biggest in American history, next to the CARES Act.

Wilson’s take came with a kind of pseudo-warning. “The other takeaway is that VaR shocks are more likely when financial market participants are over-levered and have no fear,” he wrote.

In many respects, that describes the situation as it stands now. Despite a still elevated “fear gauge” (and I despise that moniker for some reason, although I’ve never known why), one certainly doesn’t get the impression that market participants, as a group, are feeling circumspect. BofA’s “Bull & Bear Indicator,” for example, is teetering on the brink of flashing a sell signal, which indicates excessive bullishness.

“Investors should be prepared for equity vol to remain elevated as we transition from early- to mid-cycle and backend rates move higher,” Wilson went on to remark. “This is normal and fits with our narrative for US equity markets since last fall.”