US equities are getting a helping hand from a familiar place.

“Systematic Vol Control is a big deal right now, acting as a surrogate buy flow,” Nomura’s Charlie McElligott said, in a Wednesday note.

The ongoing, “background” bid (if you will) has stepped in at a time when the vaunted gamma “pin” lost some of its pull, McElligott remarked, on the way to noting that vol control was in for $3.7 billion Tuesday, the biggest one-day buying impulse in nearly a month.

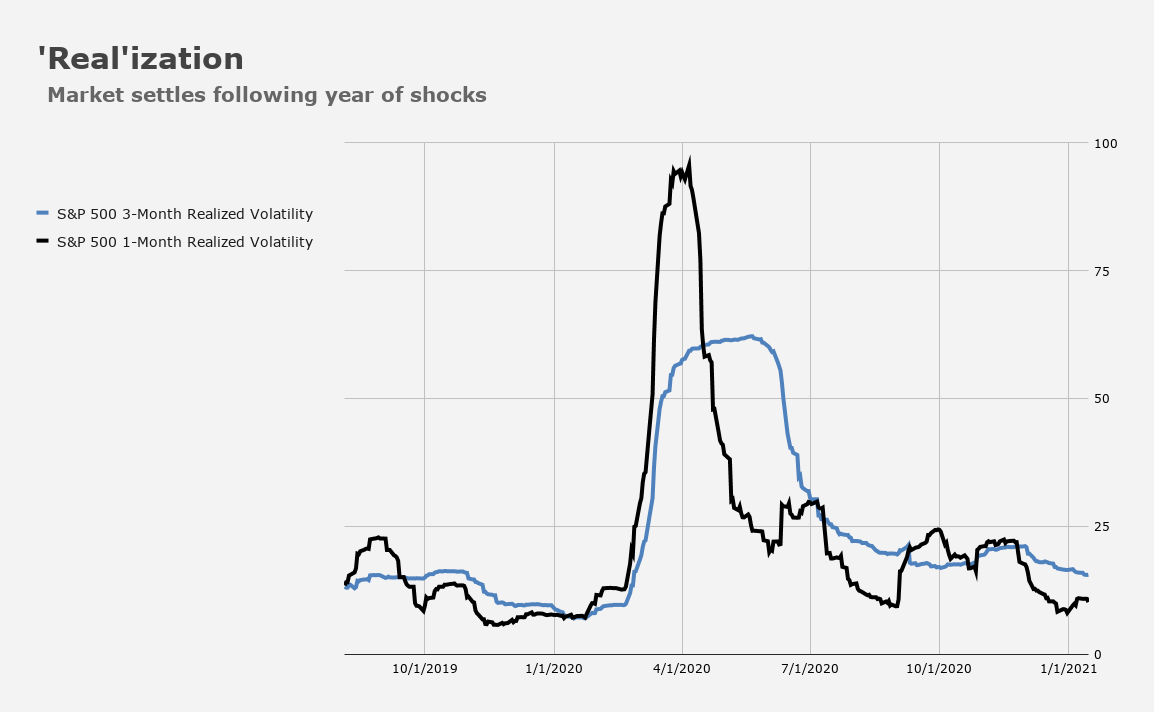

These flows are mechanical. As realized grinds lower (figure above), the exposure toggle is dialed up.

On Nomura’s model, vol control’s overall allocation to equities is still low, sitting in just the 41.5%ile going back to 2011. That, McElligott remarked, means there’s “room to buy more.”

How much more? Well, that depends on how well-behaved the market is (and that’s where the circular nature of vol-sensitive flows comes in), but assuming the S&P averages a daily move of 0.5% over the next couple of weeks, the “potential add” from vol control strats would be in excess of $40 billion in US equity futures. If the same average range were to persist for a month, that would more than double, with vol control buying of more than $96 billion.

Last week, Goldman’s Rocky Fishman looked at a subset of the systematic investor universe, on the way to contending that, at least as far as the handful of managed vol funds he analyzed were concerned, the re-allocation that unfolded across Q3 (and almost surely in Q4) meant that those funds may not have much gas left in the tank in terms of capacity to underpin the rally.

“Even with vol quite high in September, the drop from the peak was enough for managed vol funds to return to 62% long equities at the end of Q3, helping to fuel the strong global equity rally,” Fishman wrote. “In our view, the funds have likely re-allocated further in Q4, leaving very little remaining re-allocation flows to support markets as we enter 2021.”

Remember: This discussion isn’t really amenable to uniform treatment, something Fishman explicitly addressed in his latest. That is: Asking “who’s right?” or “who’s wrong?” when it comes to whether vol-sensitive strats have scope for additional re-leveraging isn’t a question that’s easy to answer and it may not even be a question that makes much sense. It hinges on what you mean by “vol-sensitive investors.”

With that in mind, I’d simply quote one of McElligott’s greatest hits in closing:

In a more qualitative ‘top down’ sense… we are all subject to the same risk-management parameters. [From] CTA flows [to] other systematic vol-control funds which use realized volatility as the toggle to manage positions / exposure / leverage [and] even traders who view themselves as ‘fundamental’ or discretionary are in the same boat as ‘momentum’/ ‘negative convexity’ players. We ALL operate under frameworks which allow for greater leverage deployment into trending markets, and, conversely, dictate de-grossings into ‘VaR-events.’

You must be logged in to post a comment.