The pro-cyclical rotation finally came.

For years, fleeting bouts of outperformance from perennial laggards (e.g., value shares) proved to be just that — fleeting.

It was the rotation that never truly played out — always “burgeoning” and “nascent,” never “durable” and “sustainable.”

To be sure, there’s no guarantee this time will be any different in that regard. After all, an epidemic is still killing thousands of people each and every day around the globe, and lockdowns aimed at curtailing the spread and minimizing fatalities continue to choke off economic growth, at least in western economies.

What’s unfolded since early November is still a manifestation of optimism more than it is a reflection of the real world. It’s “hope” (predicated on vaccines and the promise of fiscal-monetary cohesion) versus “reality” (mass joblessness, overwhelmed healthcare systems, and, in the US, lines at food banks).

But this time around, the rotation has traction. That doesn’t mean it can’t lose its footing, it just means it hasn’t yet.

For example, the Russell 2000 continues to trounce (and I do mean trounce) big-cap tech. Small-caps have outperformed the Nasdaq 100 by a larger margin in 2021 so far than they did in November.

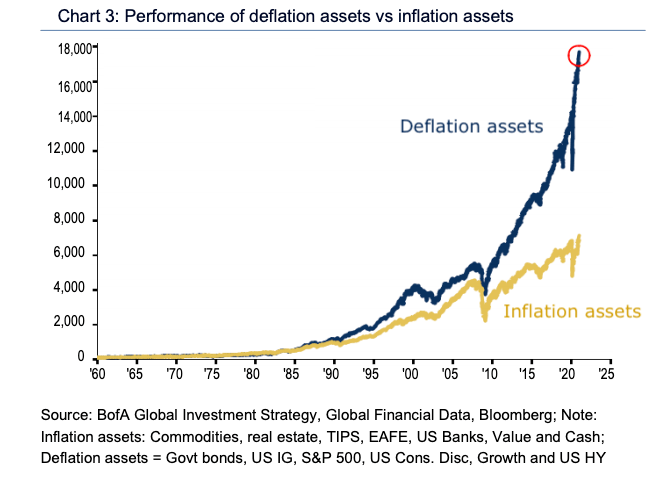

This marks a sea change from the trade that accompanied the “slow-flation” macro environment that’s dominated for the past decade. But more than that, the juxtaposition with the first eight months of 2020 could scarcely be more stark.

Remember: The pandemic exacerbated trends that already favored big-cap tech and other secular growth favorites. At the same time, the deflationary impulse from the COVID lockdowns again underscored the case for bonds, despite record-low yields.

By August, the situation was extreme. One of the most poignant visualizations is always just the growth versus value comparison (figure below).

So, is the shift durable this time around? Will vaccine rollout eventually meet expectations, reviving growth and catalyzing a turbocharged boost in the second half of 2021 as, for example, accumulated savings and stimulus money suddenly gets spent into a US economy that’s once again “safe” to engage with?

Well, those are the multi-trillion-dollar questions. Some people are betting on it, that’s for sure.

Consider that last week, energy shares enjoyed their second-largest inflow ever, at $3.6 billion. At the same time, BofA flagged the third-largest inflow to TIPs on record, and the sixth-largest haul for emerging market stocks.

The bank’s Michael Hartnett reiterated the narrative outlined above. “Lots of secular inflationary trends coincide with vaccine/reopening/supply catalysts,” he said Thursday, describing what it’s probably safe to call the “consensus” narrative.

He also mentioned the rise in breakevens in the US, on the way to noting that “inflows to bank loans and outperformance of bank stocks versus bank bonds corroborate [the] regime change from deflation to inflation assets.”

Still, it could all turn out to be a false dawn — on multiple fronts.

The structural deflationary forces in place prior to the pandemic have not gone away. And it’s not exactly as if technology will somehow become less important going forward. In the same vein, one can’t help but think that all antitrust probes aside, tech companies will continue to attract flows and investor interest, while “old” energy, banks, and cyclicals struggle to adapt to a world that arguably left them behind years ago.

Besides that, it’s worth at least considering if markets have already priced it all in. “2021 GDP and EPS prints will be historically strong, but by spring, [the] ability to beat expectations will likely diminish,” BofA’s Hartnett went on to say this week.

In 2020, a “dire” macro environment “caused abnormally fabulous returns,” he remarked, before cautioning that in 2021, it may be the case that “fabulous macro will cause disappointing returns.”

Oh, irony — you’re such a cruel master.

We may have a big supply issue with vaccines. I can not make real sense of it. Any help out there.

In my relatively small Colorado ski town, last week 400 vaccines were available for 70+, locals only, and it was reported that over 4,000 called in to get a vaccine.

I’d say we have a serious shortage.

Hope we get this rolling before mutations make the vaccines ineffective.

I am in my 50’s and have absolutely no idea when I will be able to get poked, let alone twice.

I’m confident that Biden and his team will get vaccines and rapid testing squared away. It’s supply chain and logistics for delivery. If you don’t deny science and logic, smart people who put effort into it will get it done. Trump’s team denied science and spent most of their effort talking, not working. I’m pretty sure when I was young most of us were taught that nothing great is achieved without great effort. What changed and turned that into ‘do no work, just lie’.

This article speaks to the value of a diversified portfolio that you rebalance once in awhile.

Logistics may seem to be the issue but mostly it is paralysis among the huge number of decentralized political units who have been assigned responsibility for determining distribution priorities and how to form the line. Make no mistake there is politics in this, even with lives at stake. Only 45% of Republicans are interested in the vaccine and where they are in charge, in my area at least, there seems to be less urgency attached to the distribution process. Missouri state government has completely abandoned its responsibility and seems to feel no pressure to improve the situation.

The valuation of Russell 2000 is… interesting, to say the least. My understanding is these companies are losing money in aggregate, but I don’t have the most updated nor forward looking figures.