Let’s talk bullish catalysts.

Or, if you like, we can call them “factors with the potential to suppress volatility in 2021.”

Generally speaking, Wall Street is upbeat on equities next year. It’s easy to lampoon that, but you probably shouldn’t. There are all manner of reasons why Wall Street is perpetually bullish on stocks, and critics are quite fond of pointing out all the “wrong” ones, where “wrong” usually entails suggesting that higher price targets are self-serving.

You can revel in that kind of thing if you like, but just don’t lose sight of the fact that, Japan notwithstanding, stocks generally go up over time. So, if your job is to predict the trajectory of something that, throughout history, has demonstrated a propensity to rise, it’s never a terrible idea to suggest that thing will persist on its trajectory. Sure, you’ll be wrong sometimes, and spectacularly so on occasion. But if history is any guide, and your career is long enough to capture a sufficiently lengthy timespan, odds are you’ll be right at least enough to have some claim on knowing what you’re talking about.

So, when you take a look at, for example, JPMorgan’s forecasts for the S&P in 2021, they’re hardly far-fetched. “We see the S&P 500 reaching 4,000 by early next year,” the bank’s Dubravko Lakos-Bujas wrote this week, in the bank’s 2021 equity outlook. “Our base case S&P 500 price target for 2021 is 4,400 with a range of 4,200 to 4,600,” he added. The bank expects 2021 EPS of $178. Consensus is $169, and Goldman’s estimate is $175, just to give you some context.

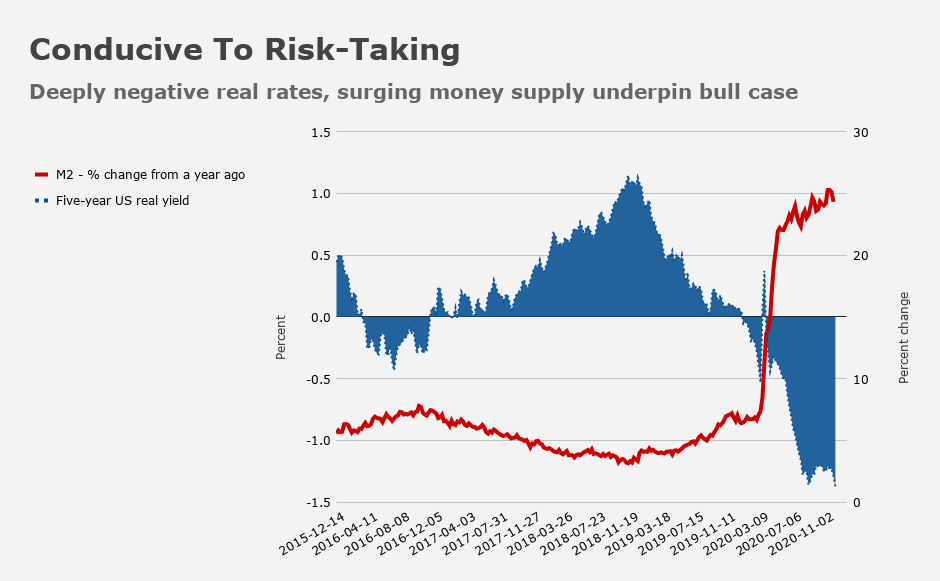

While (almost) nobody has been more vocal than me when it comes to cautioning on the risks of structural damage to the economy from the pandemic and the potential for the “scarring” effect and elevated corporate leverage to serve as a legacy drag on growth, never before have policymakers been as determined as they are now to keep things afloat on an ocean of liquidity.

“Liquidity and low rates are powerful tailwinds for equity multiples, especially in the US which is the home of a large number of Sustainable Income and Long Duration stocks,” JPMorgan’s Lakos-Bujas went on to say, adding that “while earnings and discount rate anchor valuation in the long run, ample liquidity and easy financial conditions can front run earnings and drive valuations above equilibrium for a considerable period.”

Take a look at the figure (below) which just illustrates the extent to which liquidity is abundant and the opportunity cost of not deploying capital out the risk curve is punitive.

If you want to fight that, go ahead. Just know it’s perilous.

But it’s not just central banks and vaccine hopes. As I’ve been particularly keen to emphasize, flow dynamics and the same market microstructure factors that are increasingly important when it comes to explaining equity moves, are also in play.

Lakos-Bujas’s well-known colleague Marko Kolanovic weighed in on that this week.

“In addition to these macroeconomic drivers of volatility, there are several quantitative/technical drivers that are also likely to put pressure on market volatility in 2021,” he said.

All of the drivers Marko mentioned are familiar to readers. The first is just that declining realized correlations can (and will) pressure index-level volatility. Dispersion can have a “netting effect,” if you will, something highlighted by Nomura’s Charlie McElligott, SocGen’s equity derivatives team, and plenty of others. So, if you think 2021 will be a year defined by a sustained pro-cyclical rotation as vaccine rollout helps economies return to “normal,” that shift could serve as a realized vol suppressant.

Beyond that, Kolanovic cited the gamma hedging feedback loop. “In rising markets, dealers’ exposure to index option gamma tends to be long [and] hedging long gamma exposure causes intraday mean-reversion, which in turn reduces realized volatility,” he wrote.

That’s the vaunted “gamma pin,” and it can persist for long periods of time. If volatility remains suppressed over those periods, it will create a latent bid from vol-sensitive strats, which will mechanically re-leverage in the absence of a new “shock.” (Until it all tips over.)

Finally, Kolanovic noted that the supply of volatility should be substantial. “Given that volatility selling suffered large losses in March, most volatility sellers reduced exposure or entirely stepped out of the market in 2020,” he wrote. “In 2021, we expect these sellers to gradually step back in.”

Obviously, the allure of selling vol to generate returns increases in a world where yield is scarce and central banks are determined to underwrite the carry trade, this time almost literally (as opposed to just tacitly, with forward guidance, during the low vol bubble of 2017).

And listen, folks. Before you go dismissing the sell-side as “permabulls” or otherwise deriding analysts for being upbeat about the prospects for risk assets despite what are sure to be lingering effects from the worst public health crisis in a century, just remember that almost all of the “brand name” luminaries (e.g., Stan Druckenmiller, Jeff Gundlach, etc.) you’re supposed to “trust” were wrong in April and May.

2020 has convinced me that the liquidity/momentum/passive regime has fully overtaken and rendered the prior regime of fundamental analysis close to irrelevant, at least until the perpetually-forestalled reckoning occurs. The good work Chris Cole and Mike Green have done on the risks inherent to passive overtaking active is important to understand. Chris uses a good metaphor of a sober man guiding a drunk friend home. Seems to me it’s abundantly clear that the drunk man is now stronger and will go wherever the hell he wants to, including off a cliff without warning.

Something that is hard to put a finger on makes me uneasy about this call which can be reduced to lazy momentum thinking–market is rallying, volatility is dropping–so it will continue. Again we are in the danger zone of extrapolating the past onto the future. It may turn out that way, but there seems a air of confidence about that outcome which could be misplaced.