“We’re not thinking about raising rates. We’re not even thinking about thinking about raising rates”, Jerome Powell said, in response to a question from CNBC’s Steve Liesman Wednesday.

The post-FOMC press conference was conducted remotely, as the Fed continues to observe social distancing protocol, even as the White House has never been keen on it for press events involving the president.

Powell’s performance Wednesday was easily passable, although the scope for missteps was fairly limited. The new dots show rates parked at the lower bound through 2022 and purchases of Treasurys and MBS will continue “at least” at the current pace ($80 billion and $40 billion per month, respectively) going forward, an acceptable outcome for markets, which were looking for clarity on QE.

Read more: Fed Puts A Floor Under Asset Purchases, Sees Rates At Zero Through 2022

Powell struck a decent balance between underscoring the downside risks and reiterating that over the long-term, the US economy will recover.

In that regard, he emphasized that while median projections for this year, 2021 and 2022 obviously reflect the impact of the pandemic, the longer-run outlook for the labor market and potential growth remains mostly unchanged.

“[It’s] way too early” to downgrade longer-term projections, Powell said, noting that he certainly hopes he doesn’t have to change his own forecasts to reflect structural damage.

He was keen to perpetuate the characterization of COVID-19 as akin to a natural disaster – a kind of one-off shock, from which the economy can recover and which shouldn’t be allowed to cost people their jobs or force the permanent closure of businesses.

“You don’t want to see businesses fail due to the pandemic”, he remarked. “They didn’t do anything wrong”, Powell said of the 20+ million people who recently lost their jobs. “This was a natural disaster. We gotta get them back to work”.

The Fed chair tiptoed around the May jobs report, calling it good, but noting the road back is long. The next few months, he said, will be important in discerning what the real story is for the recovery. He described the better-than-expected jobs numbers as illustrative of how uncertain things really are.

Powell was pressed repeatedly (at least twice anyway) about his opinion on the need for another virus relief package from Congress. As discussed here at length on Tuesday, some Republicans are leaning in the direction of citing the May jobs numbers (alongside gains on Wall Street) in contending that further aid may not be necessary.

Although Powell was careful to emphasize that the Fed does not presume to dictate fiscal policy to Congress, there was no ambiguity about what he believes personally. More fiscal stimulus is necessary.

Asked specifically about the proposed extension of extra unemployment benefits provided by the federal government, he demurred. “I wouldn’t try to give Congress specific advice on that”, he said. “We’re happy to give advice if people ask for it, but probably not publicly”.

One person who wasn’t shy about “giving advice publicly” on Wednesday was Steve Mnuchin, who seems to have found an (extremely) unlikely niche as the champion of stimulus for down-trodden Americans. It was Mnuchin, you’re reminded, who bridged gaps between Democrats, Republicans and the White House in order to get trillions in relief to families and businesses.

“I do think the economy is going to rebound significantly, but there is still significant damage”, Mnuchin told the Senate Small Business and Entrepreneurship Committee on Wednesday.

He got much more explicit. “We’re going to use all of our fiscal tools” and get “this economy to where it was”, he went on to declare, adding that “I definitely think we are going to need another bipartisan legislation to put more money into the economy”.

Again, it is difficult to find the right words to express how surreal it is that Mnuchin emerged as the man spearheading a full-throated, around-the-clock effort to spend endless trillions in order to bail out Main Street. Prior to joining the Trump administration, Mnuchin was the antithesis of Main Street savior.

Of course, nobody should be duped into believing Steve suddenly found a benevolent streak. Rather, he is simply the only member of the current administration who has a claim on any kind of credibility. That means that in a crisis, he accidentally comes across as rational and effective, not by comparison to other rational and effective people, but certainly relative to Trump’s cabinet and also to lawmakers who years ago decided that legislating isn’t actually part of their job description.

Treasury said Wednesday the deficit for May was $398.8 billion, nearly double the red ink from a year ago. April’s gap ($738 billion) was obviously a record. Needless to say, this isn’t the time to fret over spilled red ink, but it’s worth a mention on a day when the fiscal stimulus debate was front and center.

Powell insisted Wednesday that the Fed isn’t perpetuating inequality. At this juncture, there isn’t much utility in arguing the point – he and critics are talking past each other.

Powell is emphasizing the necessity of the Fed stepping in to avert a calamity that crashes the economy, pushing everyone down a rung (or two), leaving the middle-class poor and the poor destitute.

Critics, on the other hand, argue that Fed policy has, for at least a decade, inflated the value of the assets concentrated in the hands of the rich, thereby widening the wealth gap.

Both Powell and critics are correct (read more here).

The problem for Powell (and developed market central bankers more generally) is that we don’t know what would have happened in the absence of Fed intervention in 2008/2009. Likewise, we’ll never know what would have happened had the Fed let the world burn in March.

What we do know, though, is that the rich are getting richer, and the poor poorer. Over the past several weeks, the US reached a reckoning, where inequality of opportunity and racial injustice triggered massive street protests. As The New Yorker put it recently, “reality has endorsed Bernie Sanders”.

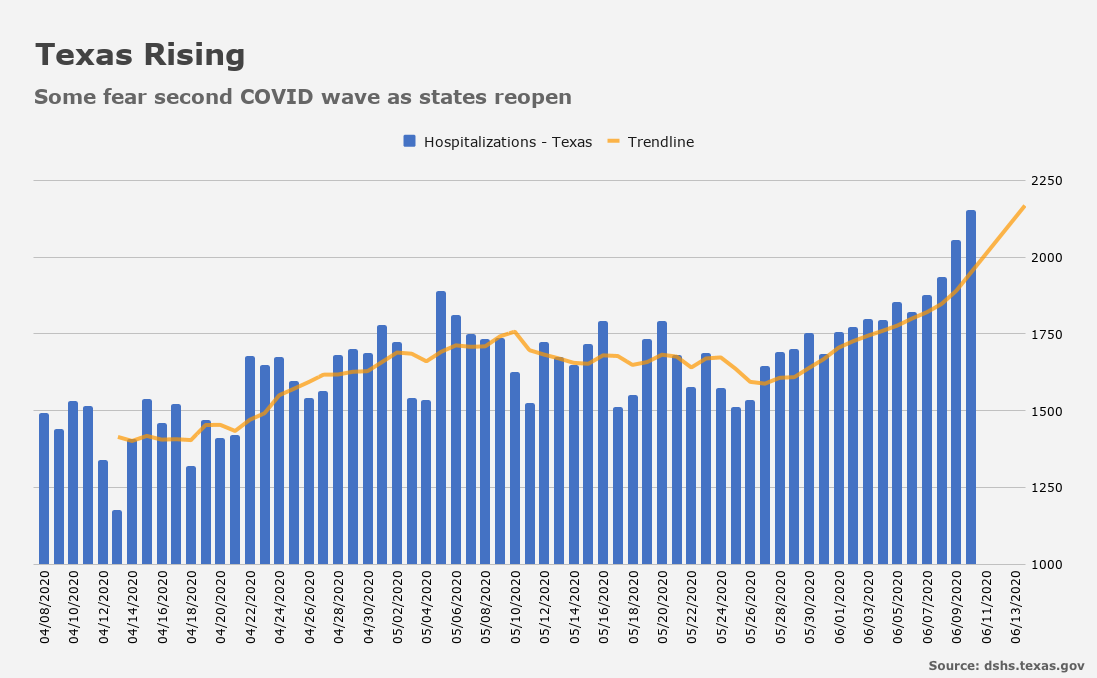

Meanwhile, the virus appears to be mounting a comeback of sorts.

Hospitalizations in Texas rose more than 6% Tuesday, to 2,056. That was the highest since the beginning of the pandemic. The figure looks to have jumped again on Wednesday.

Hospitalizations in California are running at the highest in weeks, and have risen in nine of the last 10 days.

Commenting on COVID-19, Anthony Fauci (remember him?) called the pandemic his “worst nightmare”.

“[This] won’t burn itself out with mere public health measures”, he said Tuesday, during comments to the Biotechnology Innovation Organization. “We’re going to need a vaccine for the entire world — billions and billions of doses”.

Goldman alum Steve Mnuchin, Man of the People. LOL. Apparently, in this Robin Hood moment, we steal from the future to bail out a president whose poll numbers are sinking faster than the Titanic.

We need the fiscal stimulus as much as we need the orange devil removed from power. Imagine that in 4 more years he will be adept at screwing things up.

Fauci is blind to everything except a vaccine.

Trump wants stimulus (with his name on the checks). Mnuchin wants stimulus. Powell wants stimulus. The Dems want stimulus. Governors red and blue want stimulus. The Republican deficit hawks left in the Senate won’t be able to stop stimulus. They may not even want to, but rather just be seen as fighting it. $2 Trillion in August, anyone?

For those living through a federal government check (which I guess will be >20%), will they qualify to get a car loan and mortage?