One imagines there’s quite a bit of pressure to lean into the steepener now that signs of a swift economic recovery are colliding with massive government borrowing to fund virus relief and a veritable flood of corporate supply.

With the short-end pinned at zero, and a little extra impetus from rising oil prices (fodder for the inflation crowd), it’s not difficult to make a simple case for a steeper curve, especially as the market becomes increasingly obsessed with the reopening narrative.

Indeed, the 5s30s ballooned out to the steepest in more than three years this week.

One person who isn’t totally on board with the generic narrative is Deutsche Bank’s Stuart Sparks.

“Corporate supply is an obvious scapegoat for the latest wave of curve steepening”, he writes, in a note dated Friday.

It sure is. $1 trillion in investment grade supply inundated the market through May, a breathtaking pace that underscored both the rush to bolster cash positions in the face of the expected economic fallout from the COVID panic, and the Fed prying open the doors to ensure market access for corporates that might otherwise have been shut out. (See “Fed Engineers $1 Trillion Miracle In US Corporate Bond Market“)

But Sparks isn’t convinced the combination of corporate issuance (nearly two-thirds of which has been at the 10-year maturity point or longer) and Treasury supply is what’s behind the steeper curve.

“The sum of corporate supply and net Treasury issuance exceeded May’s Fed purchases by $187 billion, but in historical context this is not at all unusual”, he writes, noting that it’s actually always been the case during post-financial crisis QE. Consider this:

In fact, during QE periods since the global financial crisis, the size of the Fed QE demand/ corporate and Treasury supply discrepancy has had a very low correlation to changes in the 5s30s curve both during the same month, and over the subsequent month. On balance the historical data suggest that the corporate supply glut has had little to do with the bearish steepening of the curve.

If domestic supply/demand dynamics aren’t behind the steepening impulse, what is?

If you ask Sparks, it’s notable that this period of steepening (and higher long-end US yields) has been accompanied by a falling dollar.

Those of you steeped (no pun intended) in the market narrative should be able to anticipate the argument.

Over the past two weeks, news out of Europe on the fiscal front has been encouraging to say the least. Germany is leaning into stimulus, and the EU took the first major strides down the road to burden-sharing, jointly-issued debt, and a real fiscal union, with concrete plans for a €750 billion recovery fund.

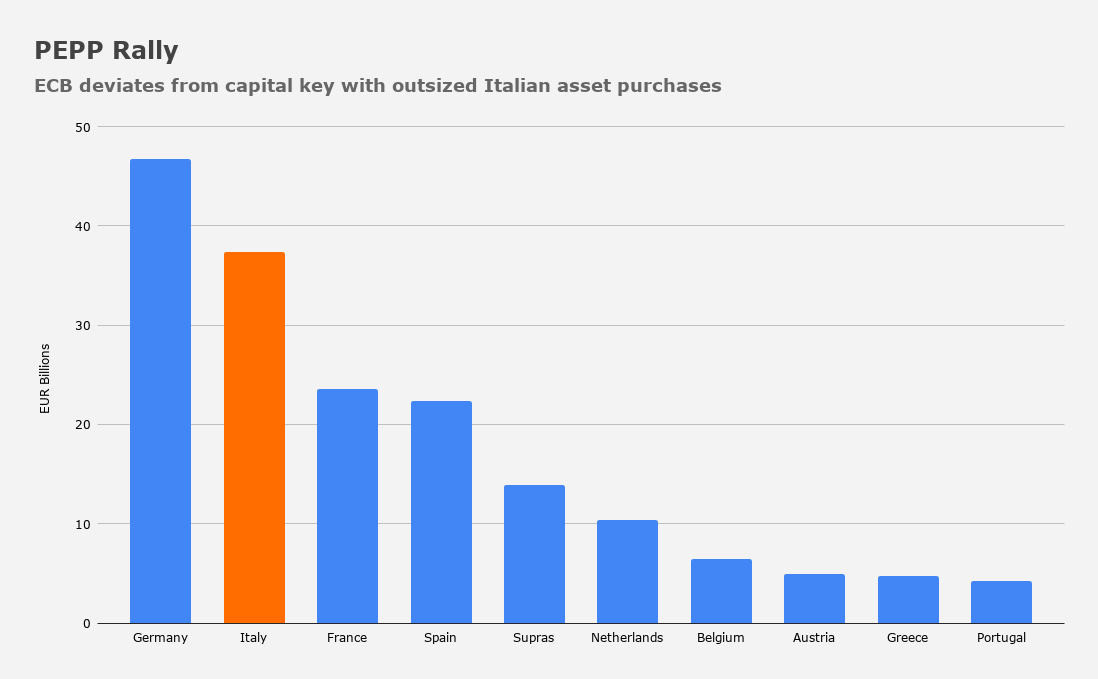

At the same time, details of purchases made under the ECB’s pandemic bond-buying program (PEPP) show the central bank deviated materially form the capital key to favor Italy.

On Thursday, Christine Lagarde topped up PEPP by €600 billion, more than the market anticipated.

All of this has catalyzed a rally in the euro as the market wonders if massive stimulus, fiscal coordination across countries, and the reopening of economies will lead to more robust economic outcomes. Italian bonds have rallied alongside the single currency.

“The strong co-movement of BTP spreads to Germany with the EURUSD exchange rate completes the picture, in our view”, Deutsche’s Sparks goes on to write.

“Positive structural developments in Europe have both led to sharp tightening of BTPs and mitigation of existential risks to the euro”, he adds, noting that “this evidence suggests that capital which had sought safety in the long end of the Treasury curve has flowed back into the euro, and more specifically into BTPs”.

If that’s true, it could explain the steeper US curve and the weaker dollar simultaneously, while the weaker dollar could then be cited in the modest rise in US breakevens.

So, what comes next?

Well, Sparks reiterates that at some point (likely soon, especially given that the latest weekly taper brings daily Treasury purchases to “just” $4 billion starting next week), the Fed will announce a set monthly pace of QE, which will continue in perpetuity. Remember, Sparks has emphasized the necessity of the Fed engineering a de facto policy rate in negative territory, and if Jerome Powell insists on not cutting rates below zero, it will fall to asset purchases to bridge the gap.

But the key point comes when Sparks notes that “the increase in term premium over recent weeks can be seen as a ‘challenge’ to the Fed’s attempts to ease financial conditions and drive capital into the non-financial corporate sector via the portfolio balance channel”.

Out of five previous episodes during which 30-year real yields rose as much as they just did (trough to peak), three were met with a decline in the S&P the following month.

(Deutsche Bank)

“Absent concrete guidance from the Fed, we see significant risks that markets will ‘probe’ for the yield level sufficiently high to provoke a Fed response”, Sparks says.

Angela and Xi having fun on the phone with each other!!

Long Euro short USD.

Euro could go to 1.12/13 on it’s way to 0.80.

Fiscal union, banks in terrible shape, just the first tranche. I don’t know. They’re going to need a few trillinon. Just Italian banks alone. The dollar is more liquid than the euro. Plus the European deficits, pensions, reduced international trade. The euro could go higher. Anything seems possible these days.

Then there is the trade weighted dollar. Seems the Fed (but, what do I know, nothing) would be more intersted in the trade weighted dollar than the eur usd pair. Then there is the relative attractiveness of US rates if they go up too much more when compared to Bunds (and evennow), and movement of capital into the dollar as rates go up. And there is the fabled $SPX to continue attracting captial. Then there is the dollar denomiated debt outside the US. Anythings possible, I guess.

Run- trend for past decades is decreasing amount of international contracts denominated in USD. As European Union ( larger population than USA) cozies up to China and Russia, more contracts will be denominated in Euros. If Euro survives internal conflicts- it will increase in international stature.