On the heels of an unthinkable “red” day for stocks, things got back to “normal” Wednesday, as equities touched fresh intraday records.

The summit push to new peaks came less than 24 hours after health officials confirmed the first US case of the Wuhan virus.

Pandemic fears aside, the dip-buying propensity is deeply entrenched. Familiar dynamics are serving to suppress volatility. “FOMO” reigns. “The force is strong with this one”.

Read more: Markets ‘Still Insulated From Shocks’, Nomura’s McElligott Says, Amid Virus Scare

And yet, the higher stocks climb, the more reason to suggest a pullback is nigh. That’s almost tautological, unless you believe we’ve transcended pullbacks – that the era of stocks going down as well as up has passed for good.

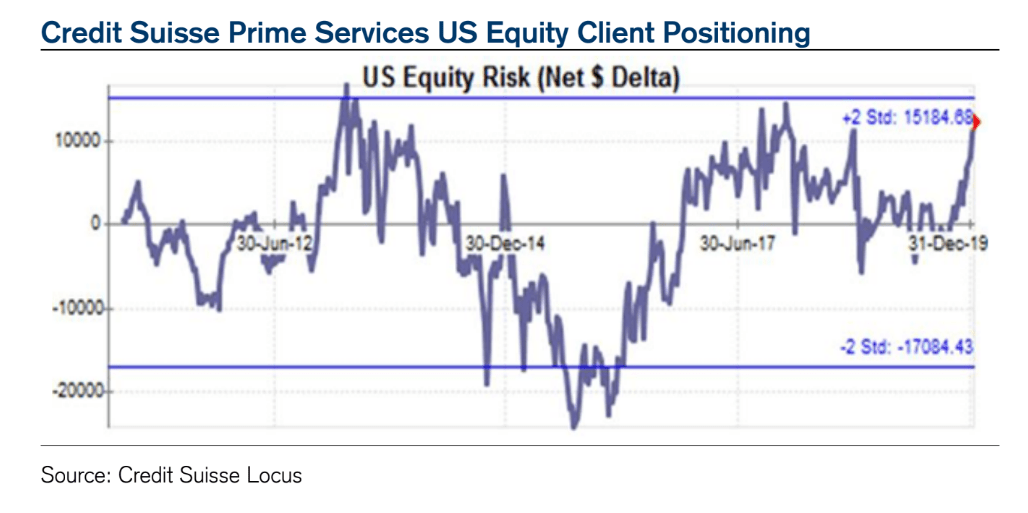

This week, strategists have variously suggested that key indicators are flashing red. In that context, it’s worth noting that data from Credit Suisse’s prime services desk shows positioning in US equities at the highest since September 2018 and January 2018.

(Credit Suisse)

Needless to say, things went awry shortly after those previous peaks, something the bank underscores.

“On both of these previous occasions the market subsequently saw a sharp selloff”, Credit Suisse wrote Tuesday, adding that if you ask them, the US equity market “has moved into a ‘melt-up’ phase, where the risk of a correction becomes increasingly elevated… even if there is still no sign of an outright reversal or price top as yet”.

Late last week, while discussing the viability of their “Great Rotation II” thesis in the context of stubbornly subdued equity fund flows, JPMorgan noted that a measure of individual investor leverage actually fell in 2019, even as stocks surged.

“The previous extremity in US individual investor leverage seen in Q2 2018 has been largely unwound, but what is more striking is that [NYSE Net Debit balances] declined last year despite strong equity market performance”, the bank’s Nikolaos Panigirtzoglou said.

(JPMorgan)

“This again shows how unwilling US retail investors were last year to leverage their equity bets”, he went on to suggest, before noting that “this unwillingness might indicate that leveraged US retail investors feel that their equity exposures and leverage are already elevated and are thus reluctant to add with the equity market at historical highs”.

Colloquially speaking, these are signs that both retail investors and the pros are maxed out, although we should note that hedge fund equity beta is sitting in just the ~20th percentile.

Spinal Tap references are somewhat clichéd, but they’re always funny: “You’re on 10… where can you go from there? Nowhere. Exactly”.

Of course, none of this is to say that picking a top is easy. As Credit Suisse cautions, “timing this correction [is] increasingly challenging”.

Using margin debt balances to calculate the retail appetite for stocks is jaw-droppingly crazy. How many individual investors, as opposed to hedge funds and high-frequency traders, use margin anymore? What I see on the ground is investors tapping margin loans to “bridge” property transactions and such (no avoid taking capital gains).

The melt-up is hedge funds scrambling to justify their miserable existences.

While the latest “melt-up” shares technical characteristics from Jan and Sep 2018, the difference now is that the Fed is ultra accommodative and is continuing to pump liquidity into the markets. So what is going to be the catalyst for that kind of pullback? Markets seem to be shrugging off everything else (war, geopolitics, pandemics).