Tech stocks are on fire. Perhaps you noticed.

2020 is starting to look suspiciously frothy on any number of fronts, and although you can always argue that one corner is more bubbly than another, it would be entirely fair to say that big-cap tech is at least as “guilty” as anybody when it comes to being the poster child for what may, in hindsight, be regarded as a “blow-off top” moment.

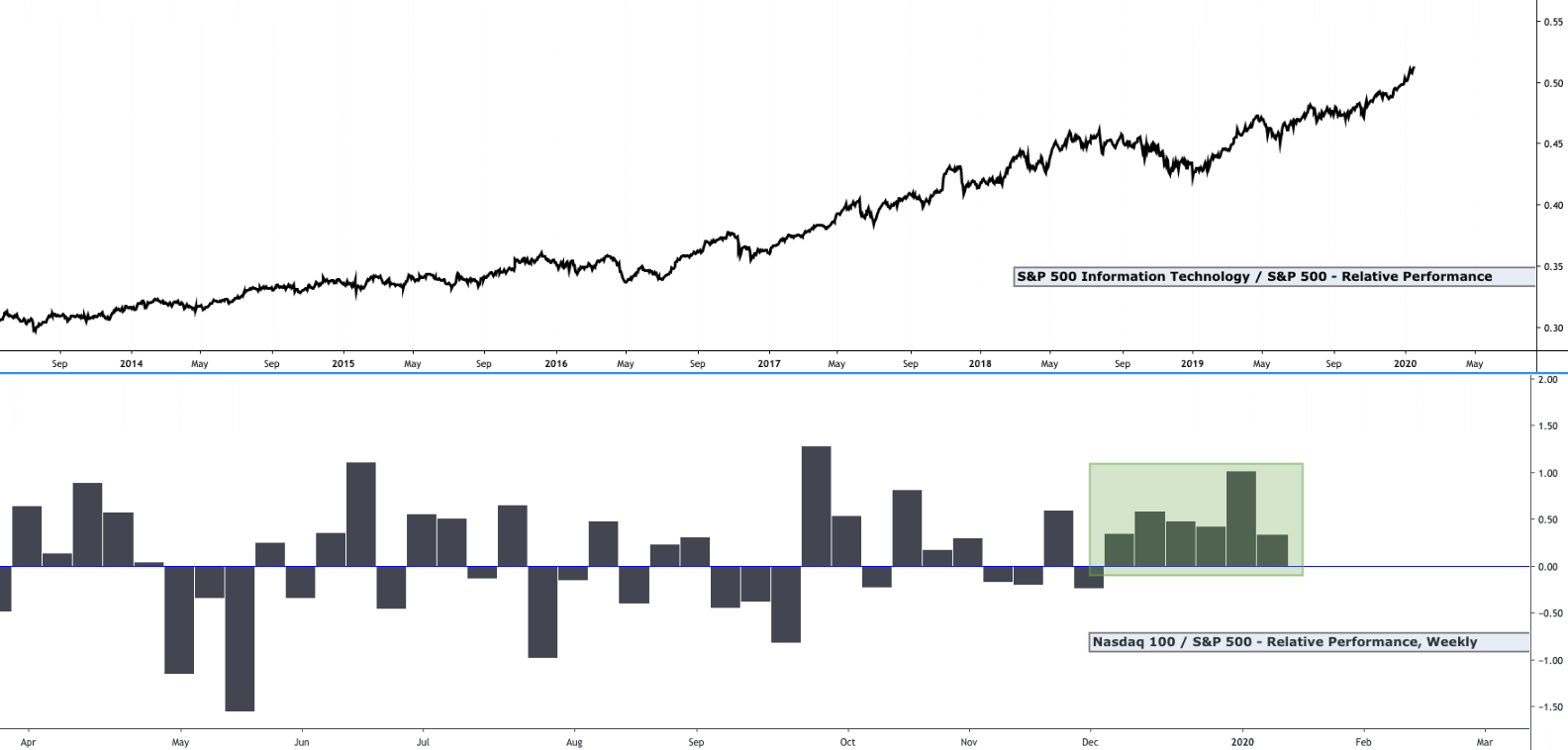

Alphabet joined the $1 trillion club this week and on one measure, the Nasdaq 100 is very nearly the most overbought since the tech bubble.

You can conjure any number of amusing visuals to illustrate the same point, but we would also note that big-cap tech has now outperformed the S&P for six consecutive weeks.

That is the longest such streak in two years, and it’s pushed multiples to extremes, leading to even more outsized representation for the behemoths.

As mentioned last week, Apple, Microsoft, Alphabet, Amazon and Facebook now comprise 18% of the S&P 500’s market cap, the most ever.

(Morgan Stanley)

Just how detached are tech shares these days? That depends on who you ask.

Morgan Stanley’s Mike Wilson has been relatively bearish on tech since the summer of 2018, when he called for “a proper rain storm” in the space. Here is the famous quote from a July 9, 2018 note:

Similarly, we think the risk is rising that US tech and growth stocks will get wet. While we are not worried about an economic recession as the catalyst for underperformance in these market leaders like it was back in early 2016, we do think that 2Q earnings season will bring an inevitable acknowledgement from companies that trade tensions increase the risk to forward earnings estimates, even if managements don’t formally lower the bar. Throw in the fact that these stocks have rarely, if ever, been so over-loved and over-owned, and the risk of a proper rain storm in this zip code increases significantly.

That call turned out to be spectacularly prescient. Q4 2018 was the second-worst quarter for big-cap tech since the bubble burst.

Then, the Nasdaq 100 promptly rallied 38% in 2019.

So, what does Wilson think now? Well, he thinks that relative forward earnings for tech are totally disconnected from relative performance, for one thing. Of course, that’s been the case since his original downgrade, but as you can probably surmise from the above, now it’s even more extreme.

“Tech’s relative performance has significantly overshot relative to forward earnings”, Wilson wrote earlier this week. “In fact, relative forward earnings are essentially flat since November of 2017, while relative performance for the tech sector is up 26%”.

(Morgan Stanley)

As you can see, that’s pretty glaring. “In fact”, Wilson goes on to note, “the only other time we have observed such a disparity was during the tech bubble of the late 1990s”.

Wilson thinks that’s not sustainable, although like everyone else, he recognizes the perils of trading against central banks. “We appreciate that momentum can go further in a liquidity driven bull market but we can’t ignore the lagging relative earnings growth”, he says, in the course of explaining why Morgan’s allocation still has tech shares at underweight.

Although he does grant that relative earnings revisions breadth has taken a turn for the better in tech over the past several months, it’s hardly enough to explain the price performance disparity.

(Morgan Stanley)

Ultimately, Wilson is convinced that a “powerful rotation to other sectors and stocks” will unfold “at some point this year”.

While those of you riding the Nasdaq to ever higher highs may be tempted to scoff, don’t forget that it was just over a year ago when Apple plunged 30% in the space of three months.

Yes, it subsequently rebounded to soar a ridiculous 90%, but you didn’t know that was going to happen during the dark days of December 2018, now did you?

Read more: Nasdaq Floats Off Into Stratosphere As ‘Other 1 Percenters’ Conjure 1999 Parallel

30-40% of the SP500 is probably in secular decline. Of those that are left growth is low in many areas and health care will eventually be pressured. So a dearth of growth (not that AAPlL is growth) pushes everyone into tech.

It is a sign of troubles in other sectors in addition to excess liquidity that are leading to the excesses.

GOOGL in innovating in amazing ways. AAPL and FB not really.

But if you want mispricings look at Utilities and bonds of all stripes.

I’ll take my risks with GOOGL rather than owning a utility for the next 10 years.

But no doubt tech and pretty much everything else is grossly overvalued. Nasdaq hasn’t even doubled from the early 2000 peak. I remember the infous (and insane) Nasdaq 5000 bubble daze…………..