At this juncture, nobody should be surprised to get fresh evidence of economic malaise out of the eurozone, but just because it isn’t surprising, doesn’t mean it should go unreported.

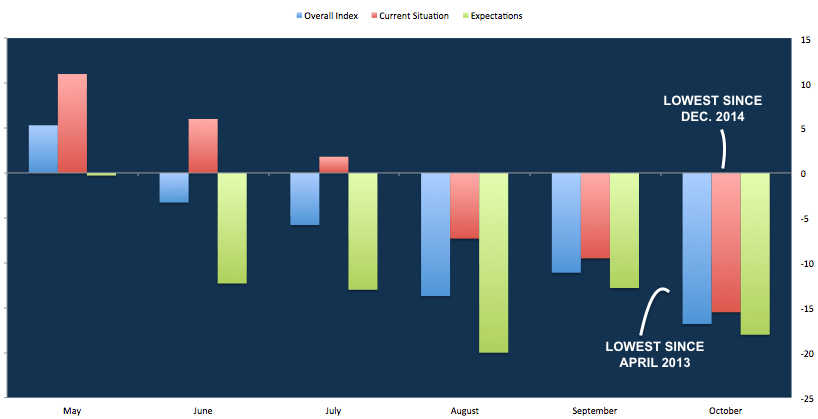

Investor sentiment tumbled to the lowest level in more than six years in October, according to the Sentix economic index, which printed a horrendous -16.8, missing the most pessimistic estimate from more than a dozen economists (the range was -14 to -10.1). It was the worst print since April of 2013.

“There is no positive reaction to central banks’ aid measures, and economic assessments are broadly negative in October”, Sentix said, adding that “the recovery of expectations from [September] has completely evaporated”.

At -15.5, the current situation gauge now sits at an almost five-year nadir.

“Fears of recession are immanent”, the report says, flatly.

Meanwhile, the latest read on the German manufacturing sector was predictably dour. Factory orders fell twice as much as expected in August, dropping 0.6% on a MoM basis. Consensus was looking for a 0.3% decline.

But the MoM series is noisy. To get a sense of how bad things really are, you need the YoY chart, which shows demand slumping for 15 consecutive months.

Germany is in a recession. Period. And yet, Berlin is still clinging to an almost pathological obsession with fiscal rectitude, despite being able to borrow for free.

For ECB doves, this is just more evidence in support of the Governing Council’s controversial September decision to relaunch net asset purchases. It simultaneously increases the sense of urgency around fiscal stimulus, despite Germany’s recalcitrance. One wonders what the pain threshold is in Berlin. Clearly, we haven’t reached it yet.

“There is a lack of awareness on the part of politicians and the public that quick answers must be found in order to counter the pace of the downturn”, Sentix managing director Patrick Hussy warned on Monday. “Monetary impulses are expected to produce wonders that they are increasingly no longer able to achieve on their own”.

Read more: Traders Eye Accounts Of High-Stakes Fed, ECB Meetings At Pivotal Moment For Global Economy

Rightfully so, taxpayers are wondering why QE didn’t work globally — and hopefully serious finger pointing will begin as to why central banks are allowing economic systems to fail. Understandably there are cyclical business cycles and downturns, after growth but after applying about $15 trillion in stimulus to attempt to obtain synthetic or organic growth is looking like a very bad way to do business. One might think that politicians around the world will be held accountable for supporting a weak, corrupt banking industry that infests all levels of government, all of whom need to be weeded out. Sadly, trump is a great symbol of global economic destruction — and his 3rd grade understanding of economics and his criminal intentions are quickly insuring that America will Never Be Great Again and we all can thank the GOP for placing us in the crosshairs of total failure!

Meanwhile, a fast look under the U.S. Treasury hood:

Something changes with treasuries around 2008-07-04:

Oct 8, 2008 – “The Federal Reserve, working in coordination with other central banks worldwide, enacted an emergency interest rate cut on Wednesday. The Fed lowered its fed funds rate by a half percentage point to 1.5%”

Then: Nov 3, 2010 “The Fed said it would buy an additional $600 billion in long-term Treasury securities by the end of June 2011, somewhat more than the $300 billion to $500 billion that many in the markets had expected.

The central bank said it would also continue its program, announced in August, of reinvesting proceeds from its mortgage-related holdings to buy Treasury debt. The Fed now expects to reinvest $250 billion to $300 billion under that program by the end of June, making the total asset purchases in the range of $850 billion to $900 billion.”

Then: 2019/08/13/ trillion-us-budget-deficit-could-lead-the-fed-to-cut-rates “We recognize that the Fed doesn’t bend to the circumstances of dealers and carry traders, but we’d also note that we never had this much Treasury supply during a curve inversion on top of record inventories with leverage constraints!” Pozsar wrote.”

Taxpayers, of course, are on the hook to those buying the government’s debt.

https://fred.stlouisfed.org/graph/?g=p62T ( slide the macro date from 2008 to about April 2019 )