The two sides discussed issues on the yuan including the need to abide by previous commitments made by the G-20 nations including not to engage in competitive depreciation and to communicate closely on currency issues. The negotiators discussed the necessity to respect the autonomy of each other’s monetary policy, a market-oriented foreign exchange mechanism and the disclosure of information according to International Monetary Fund standards.

That’s from PBoC governor Yi Gang, speaking Sunday at an NPC press conference.

What you want to note about those comments is that Yi stops short of referencing the kind of one-sided currency pledge that US officials have variously suggested is already written into a prospective Sino-US trade deal.

The currency “pledge” is a somewhat bizarre animal anyway, something we’ve discussed at length in these pages since February 19, when Bloomberg first reported that the US was demanding China promise currency stability as part of any trade deal.

We won’t endeavor to go back over the whole story here as you can read everything you’d ever want to know (and more) in the linked posts below, but suffice to say it’s not clear that the currency stability pledge has any real meaning under the circumstances. China wants a generally stable yuan and on top of that, Beijing went out of its way last August to slam the brakes on the currency’s slide after the yuan depreciated enough to offset the impact of the first rounds of 301-related tariffs. While the PBoC was clearly countenancing depreciation from June through August, some of the downward pressure on the currency was based on market expectations for a weaker yuan in light of the expected impact of the trade war on the Chinese economy. The Fed’s hawkish lean also pressured USDCNY higher.

Read more on the currency stability pledge

As US Demands Yuan Stability In Trade Talks, Let’s Go Insane Again

As Trump Meets Liu He, Let’s Talk About That ‘Stable Yuan Pledge’ Again

And don’t forget the delicious irony inherent in the US demanding yuan stability. “The US is asking China to keep the value of the yuan stable as part of trade negotiations”, SocGen’s Kit Juckes wrote last month, adding that “‘stable’ means more than one thing in FX (are they talking USD/CNY or the trade-weighted yuan, for starters?) but the irony of asking China not to let its currency float (or sink) freely after years of examining whether they are currency manipulators, is wonderful.”

In the end, this was probably more about optics and giving Donald Trump something to shriek about at campaign rallies (e.g., “Nobody has been able to stop illegal currency manipulation like I have!”) than anything else. Yi’s comments (cited above) appear to suggest that Beijing is inclined to blunt that message by making it clear that China didn’t just acquiesce, even if what the US is demanding on the currency is generally consistent with what’s going on anyway.

Of course there’s only so much yuan appreciation/”stability” that China is going to tolerate in the event the domestic economy continues to decelerate. Beijing isn’t going to keep the currency artificially strong if the market is trying to push it weaker amid worsening data. That is, China isn’t going to shoot itself in the foot by actively strengthening the currency amid crashing exports just to placate Trump.

Meanwhile, the latest credit data from China is out and suffice to say those who expected a dramatic snapback after January’s tsunami were correct.

TSF was 703 billion yuan in February, well below consensus, which was looking for 1.3 trillion. Out of 21 economists surveyed, the lowest estimate was 750 billion yuan.

New yuan loans in February were 885.8 billion, down from 3.23 trillion in January. Economists were looking for 950 billion.

There’s all manner of parsing to be done here and China strategists on the sellside are doubtlessly hard at work doing just that right now (or if not, they will be on Monday).

The slowdown from January was expected, but the breakdown will be important. It’s probably best to rollup January and February together, but the bottom line is that seasonal factors notwithstanding, questions remain as to whether Beijing will be willing to flood the market with liquidity, something authorities in China have repeatedly suggested they are not inclined to do.

M2 growth slowed to 8% in February, well below the 8.4% consensus expected and below the lowest estimate out of 26 economists.

Read more on the January deluge

A 4.64 Trillion Yuan Tidal Wave Of Credit Growth — Let’s Discuss

You’re reminded that there are pressing questions about the extent to which credit demand (not credit supply) is the problem in China.

The monetary policy transmission channel remains clogged and some argue that until we get a benchmark cut from the PBoC (as opposed to RRR cuts and other various half-measures), that’s not going to change.

Read more

‘Unavoidable Option’: Only Analyst To Nail PBoC In 2014 Says China Rate Cut ‘Imminent’

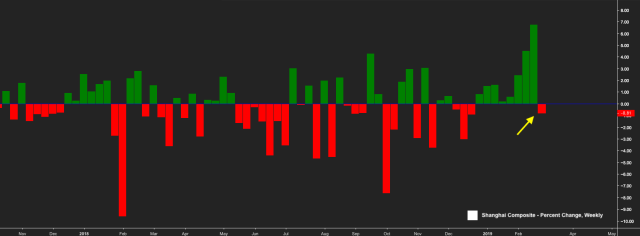

In any event, that’s the latest out of China as market participants prepare for yet another week of hand-wringing over the prospects for the trade deal. It’ll be interesting to see how Chinese equities act following Friday’s rather uninspiring session which brought the SHCOMP’s streak of weekly gains to an unceremonious halt.