The nice thing about XRP becoming a $100 billion currency – basically out of nowhere – is that there’s a lot of helpful information on both the currency and Ripple the company. You can start with the company’s Wikipedia entry, since that’s a place I borrowed from liberally, as well as the company’s resources.

Other good write ups on the company come from CoinDesk and Multicoin Capital, and both may do a better job recapping the Ripple/XRP history and 101. (I wrote this in a few hours, so just trying to capture the basics here. There are certainly areas that are imprecise, but I’ve tried to get the facts as best as I can considering the crypto myth factory that you must navigate during research.)

Ripple is a real-time gross settlement system, currency exchange, and remittance network. Its registered “gateways” are primarily financial institutions that issue new digital assets on the XRP Ledger (representing currencies and commodities, e.g.) or private exchanges like Bitstamp that hold XRP and facilitate trading. Gateways can make irreversible transfers of XRP and gateway-issued digital assets without lengthy back-office settlement delays, and transactions cost just fractions of a penny worth of XRP.

Fast, cheap, dynamic, and second only to bitcoin perhaps in longevity and usefulness. But it’s still a pretty centralized system, which relies heavily on trusted third parties.

Non-XRP assets issued on the XRP Ledger get their value from a given gateway’s agreement to honor the obligation that the issuances represent. Not much different from legacy “trusted” systems.

And unlike open proof-of-work or proof-of-stake blockchains that can be validated by anyone and require some type of work or skin in the game, Ripple has carefully maintained a permissioned network of “validators.” Transactions are added to the ledger once a supermajority of these trusted (and usually regulated) entities agree to a given ledger state. While anyone can sign up to be a validator or run their own nodes, most people simply default to Ripple’s own trusted, curated “unique node list.”

That UNL controls who has a say in changes to network rules, so theoretically, some network rule changes could make the system fully “permissioned” overnight. Even if Ripple will tell you it would fight this type of thing tooth and nail, the reality is its positioning pretty much guarantees a regulator or government could come in and say: “Make the change. Unregulated gateways are blacklisted.”

Even without that heavy-handed intervention, some contributors have voiced concern about the “Orwellian path” the project was on. (Eyemuffs. FUD.)

“It appears that there will be both “Session Access Control” and an embedded “Credential” in each [Ripple] transaction that will further serve to ‘qualify the level’ of transaction service and future history of the transaction. The X.500 Directory Services make this easy for anyone with hierarchical permissions… to view, control, to report, etc.

Cross references could be maintained for ‘Bill’ in company ‘X’, as well as for the same ‘Bill’ the citizen, in say, Ontario, inside the country, Canada. So any administrator at each of the nodes with viewing or control permissions in the Directory; in the province of Ontario; in the federal jurisdiction of Canada – not only has access, but may also have threshold setting controls and reporting or forwarding tax organizations… or whatever.

You will be familiar with other crypto exchanges, which all have multi-tiered level permissions. This is how Ripple will implement KYC monitoring for every transaction. There will be a Identity Management pointer from Directory into the Ripple Ledger. Lastly, you will note, that in one of the FinCen documents that Ripple has a requirement to ‘monitor’ accounts and their associated transactions… presumably… to which addresses and for recorded types and amounts. I know Microsoft Active Directory rather well, and this type reporting and control is easily implemented… just more code.”

Ahhh, the “FinCen documents”, the snafu that pushed Ripple further down the compliance and centralization path.

For historical context, the company was slapped with a fine by FinCEN in 2013 for acting as an unregistered MSB and failing to implement an adequate AML program. While the fine itself was kinda bullshit – all the company really did was “fail” to file know your customer documents on Roger Ver, one of the most well-known industry investors at the time – the event did lead to a radical shift towards enhanced oversight of its network.

Immediately following the FinCEN fine, Ripple beefed up its KYC/AML policies and today will only recognize and recommend gateways it trusts are in compliance with regulations. Makes sense. But while anyone can create a gateway in theory, “the XRP Ledger has a system of directional accounting relationships, called trust lines, to make sure that users only hold issuances from counter-parties they trust. [emphasis mine]” And since most people default to Ripple’s UNL list, they will usually just default to trusted verified Ripple counter-parties.

There’s nothing wrong with this at all. On the contrary, you can see just how much of a boon this renewed focus has been for the company. But it also fed the narrative that Ripple was creating a “bankcoin” with XRP far outside of bitcoin’s decentralized and censorship-resistant ethos. And with banks getting the explicit advertising nod on the Ripple site, it’s easy to see why people are buying the prophecy that the XRP-financial incumbent relationship is cozy:

The only XRP use cases highlighted are for banks and payment providers. This isn’t dirty drug money.

Many have been hyping Ripple as a possible alternative to SWIFT, one reason the company has been successful in getting 100+ banks to test its platform – with particularly interest in Japan and Korea.

Ripple plays by the same global financial rules as the big banks, but offers them much faster settlement times and lower fees. Testing the system is a no brainer, and some have already praised its utility.

But that’s all about Ripple’s distributed ledger technology. Not XRP itself.

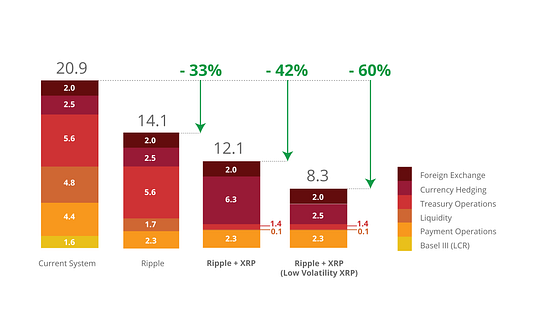

Even Ripple’s own rosy projections for XRP liquidity and reduced volatility show a fairly marginal benefit to using XRP vs. using RippleNet itself:

Even Ripple’s marketing team says RippleNet + XRP yields a mere 2bp incremental reduction in costs.

Yet up until a little over a year ago, most people – including many within Ripple – wrote off XRP as a legacy byproduct of a system that pivoted from crypto-currency to enterprise distributed ledger technology. Aside from the negligible amount required to prevent network spam (fractions of a penny per transaction), there was no need for anyone to hold it.

That is, of course, until the company renewed the narrative that XRP could pick up steam as a viable potential “bridge currency.” An asset that could be held in reserve by institutions who trade certain currency pairs infrequently, e.g. Tier 2 banks outside of the correspondent banking system who wish to settle a local currency transaction. How does Bank A in Africa settle a debt denominated in pesos if they do business infrequently with Bank B in Latin America? Usually they go through another correspondent bank who uses a larger reserve currency to settle up – multiple hops to get to the same transfer, with each intermediary in the process taking a cut of the action.

With the resurgence in cryptoasset prices underway in mid- to late- 2016, Ripple set out to reestablish XRP as an alternative.

A new potential global reserve currency for enterprise cross-border payments. One that could reliably circumvent expensive correspondent banks and traditional reserves at a lower costs.

In Miguel We Trust

American Banker’s Brian Eha nailed Ripple’s broad ambitions for XRP in a piece earlier this year: “once [XRP’s] market cap gets high enough and it is being traded heavily enough – use it to provide banks with liquidity on demand.”

“1) There’s a business that Ripple has providing transaction processing software to banks. It can work without XRP and without any blockchain tech. It improves international payments because it uses end to end messaging to track payment progress, ensure all necessary compliance information is in the transaction in the first place, precisely knows the fees ahead of time, and provides prompt, reliable confirmation of delivery. This is a big enough improvement that banks will use it even if the actual money moves the same way it does now.

2) Ripple has built a public blockchain with a native asset. It has various nice features – a distributed exchange, good governance, fast transactions, high transaction volume, native multisign, key rotation, payment channels, and so on.

3) The hard part about getting banks to use a blockchain isn’t the blockchain, it’s everything else. It’s governance, compliance, integration with banking systems, and so on. our software does all that stuff, so if routing a payment through XRP is a penny cheaper, the bank can take it. Then we have to make XRP cheaper somewhere that matters.

4) We don’t target the biggest corridors like USD->EUR because they’re efficient. We target an inefficient, but fairly high volume, corridor. For example, EUR->INR. Market makers have very small profit margins, so even a small incentive to place good EUR<->XRP and XRP<->INR offers can beat what banks are getting now through the correspondent banking system.

5) Once we get one corridor, we hang other countries off each end of the corridor, expanding the reach of XRP.

6) Now, say you’re a company like Seagate that pays out money all over the globe. If you have to make payments to five countries in our corridors, you’d rather hold one pile of XRP than five piles of different currencies. That increases demand.

7) Now, say you’re a company like Apple with a huge pile of cash. If you want to snap up other assets cheap, you’ll need to hold the asset the people selling want. If they’re going into any of our corridors, they’ll want XRP, so you would want to hold it.

8) If that succeeds, it should massively increase the price of XRP.

9) Ripple holds a huge pile of XRP and will be the dominant XRP holder for the foreseeable future. But we’re primarily VC financed and we get revenue from selling software to banks. We don’t use our XRP as a bank account but as a strategic weapon. (Though we do sell some for revenue, we just don’t need to for salaries or to keep the lights on.)

10) Anyone who gets XRP from us as part of some deal with a lockup has their incentives aligned with ours. They want the long-term price of XRP to go up too.

I think that pretty much covers our vision. There is, of course, no guarantee of success. This is a pretty crazy thing we’re trying to do. But we have 160 full time employees and have raised tens of millions of dollars. We’ve hired many amazing people, and our track record speaks for itself.”

Seems plausible so far, and in fact, they had already hired a critical person who was driving this “pretty crazy thing.” And quite successfully at that.

Miguel Vias, a former CME Group executive, joined the team in late 2016 as head of XRP markets with a mandate to “strengthen the XRP markets and set the stage for large-scale institutional adoption.”

Vias’ quarterly markets updates have been revealing, and summarize the strategy his team has taken to drive XRP adoption: “re-educate” the bitcoin community about XRP. Lock Ripple’s treasury tokens in escrow, and institute trading policies that limit the amount that can be sold over time to limit the supply centralization fears. Strike agreements with the founders regarding sales of their network stakes so they can’t go rogue. Offer eye-popping incentives to “liquidity partners.”

Above all else, harp on that reflexive “if you build it, they will come” reserve currency narrative. If only XRP gets a higher market cap, it will get better liquidity, and that will lead to wide-scale bank adoption to replace $27 trillionof nostro/vostro accounts and their dead capital.

In Vias’ first quarter at the company, Q4 2016, market participants purchased $4.6m of XRP from Ripple. These purchases “include sales restrictions that help mitigate the risk of market instability due to large subsequent sales” and Vias noted, were “important because they introduce important new partners to the XRP ecosystem.”

In Q1, the company sold $6.7m of XRP, something Vias attributed to the bitcoin scaling debate, Ripple’s more vocal commitment to shore up XRP as an asset, and the market’s enthusiasm for its progress penetrating financial enterprises via bank pilot programs. He noted the importance of the bank partnerships especially, by concluding:

“Markets are clearly connecting the dots that banks which join the Ripple network today are prospective users of XRP liquidity in the future. Growing bank membership of the Ripple network creates opportunities for Ripple to deepen those customer relationships and cross-sell liquidity solutions built on XRP, all of which should be beneficial to the asset.”

Then the asset went totally vertical.

In April, the company announced its plans to escrow 55 billion XRP and added several high profile new exchange partners. Buyers followed suit: in Q2, Ripple sold $21m of XRP to strategic partners PLUS an additional $10.3m to its exchange partners as part of a new programmatic sales strategy to unload a small percentage of overall daily XRP volume. 3x what it had generated in the previous two quarters.

Remember, this is realized company revenue from secondary token sales, not mere appreciated corporate treasury tokens. They were starting to dip into the honey pot in a big way.

In Q2, the new programmatic sales program represented 9bps of the $11bn in total on-exchange volume for XRP. By Q3, that programmatic selling had doubled to 20bps of $16.50bn traded: some $33m sold into daily trading volumes plus another $19.6 in new direct strategic sales with resale restrictions.

In Vias’ first full calendar year aboard, Ripple earned over $200mm in revenue just from selling XRP, and the company’s unrealized 61 billion XRP war chest value swelled to over $100 billion.

The Retail Pump

It’s easy to look at the absolutely staggering price action in XRP in Q4, the unsubstantiated rumors about bank adoption of XRP, and some of the aggressive marketing from Ripple the company, and believe there may be corporate shenanigans to blame.

But after reviewing dozens of interviews, blog posts and transparency updates, I’m not sure that’s fair – even if XRP’s valuation is patently absurd.

It is true that Ripple is marketing XRP more aggressively than ever before, and doing so straight into the retail investor base’s speculative fervor and CNBC’s fellatial 24/7 coverage of all things crypto.

And they are marketing even more aggressively to enterprises, launching a direct competitive to SWIFT’s SIBOS conference in October; stacking its board with former regulators and compliance chiefs to woo partners; and introducing a $300m RippleNet accelerator program to promote the growth and utility of XRP. (Among its incentives: rebates of up to 300% of the integration fees and first year’s license fees for its new institutional partners.)

The company has also continued to tout its solution – perhaps fairly – as “the only enterprise-ready public blockchain” in order to distinguish itself from the ICO craze and other more fly-by-night operations.

XRP’s association with that enterprise-ready blockchain solution, however, is tenuous at best.

What do the all-powerful partner banks actually think?

From the ones I’ve spoken with: they think the company is seriously blurring some lines when it promotes its rising XRP volumes and insinuates that new liquidity is coming from institutions vs. retail investors via crypto exchanges.

This is from someone who has been very hands on with testing RippleNet and has followed the company and XRP closely:

“I know of no banks that are a) using it, or b) would touch it in any way as it is controlled by a SV company and 20% of all XRP in existence were taken by the founders. Ripple’s approach with XRP has been to get it listed on a bunch of exchanges and ‘infer’ but never explicitly say that banks are using it for settlement. We (and all the global players that I work with) are not. We wouldn’t touch it.”

One anecdote to be sure, but one that resonated enough that when I tweeted it out, several others from the blockchain banking community reached out proactively to basically say, “yeah, pretty much what [s]he said.”

Let’s assume though, that all of these corroborators were either a) sour grapes who missed the moon, b) true corporate dolts, c) simply ignorant about XRP updates, or d) some combination of all of the above.

An impossibly long list of things already needs to go right for XRP to become a reserve currency for banks, even though it’s already trading like a top 30 M1.

What Needs to Go Right

1) Many, many, many other banks must buy-in to the bridge currency thesis. Either buy holding XRP themselves, or trusting that they will see the promised basis point savings by working with Ripple’s (more opaque) market makers. The XRP “market cap” math doesn’t work otherwise. Yet wide-scale bank buy-in to XRP would essentially endorse this new reserve and bless Ripple’s ability to become a non-sovereign central bank. Absent a multi-bank, multi-national negotiation over Ripple’s treasury policies, it’s nearly impossible to picture. Are global financial institutions really so stupid as to give up correspondent banking revenues for anything other than an arm and a leg?

2) If #1 is true, then it stands to reason the company will need a small coterie of partners to start with who will extort incredibly lucrative terms in return for their use and promotion of XRP. Which banks would need to be given XRP to make this worth their while? How much would they demand? How would this clash with “wave two” adopters? Remember when R3’s consortium started to fall apart after squabbling over deal terms. XRP negotiations would have much higher stakes. Everyone will want in on the cartel. No one will want to pay dues.

3) Assuming #1-2, then the adopting banks need to be willing and able to accept XRP as revenue (rebates!) or buy it at a steep discount to market prices. Both could cause taxable events, though, and force the same recipient to sell (partially) for tax purposes? Which banks get these super special deals and discounted XRP? What are the terms that those banks will be able to negotiate during their purchases? How can you envision other banks demanding anything less? Perhaps there are clues in the details of the company’s XRP selling strategy, but the terms of those deals are opaque.

4) There needs to not be a crash in the meantime. Whoa baby, you thought the Tezos “tote bag” quote was tasty, how about some of the dozens of lines about building a new global reserve currency on Bloomberg, CNBC, at conferences and all over the financial media right now? If the market corrects, the ambulance chasers will be out in FULL force vs. Ripple. “The BitLicense dude is on your board, and you did nothing to protect speculators who were trading on empty promises!” Holy shit it could get ugly.

5) Let’s say XRP becomes a reserve currency that obviates the need for nostro/vostro balances; Ripple can use its reserves to create a holy alliance of banking partners and market makers who bring liquidity to emerging market currency pairs and open up untold business opportunities for “the other six billion”; the almost certain “two tiers” of deals (one to retail buyers and one to institutions via “rebates”) passes regulatory muster; and there is no crash that bogs the company down in legal misery: you still need to assume that the major central banks simply pat Ripple execs on the fanny, say good game and thank you for destroying big chunks of our business, we’ll just sit in the corner and go f*ck ourselves as you steal our money printing power.

Am I missing something here?!?

Yes. This. Is. Crypto.

Throw out this entire post. I mean, print it out and burn it.

Because this is crypto, and everyone in the industry is now slinging crack crypto cocaine to retail addicts.

XRP is probably going to get listed on Coinbase, and Grayscale will probably create an XRP investment trust to further add to the hysteria. A $3 coin could get listed alongside $900 ETH and $15,000 BTC.

The sky is still the limit for XRP.

Until people finally start asking: where are those big banks?

***

Weak arguments against XRP that I considered, but abandoned:

+ XRP won’t win because BTC will. BTC has better liquidity. Ok, but XRP has the volumes that BTC had mere months ago. That lead is only marginally important. Ripple also has an exceptional board and investors, and a relative utopian ecosystem vs. BTC right now.

+ Founders stakes! Meh. Even though the company retains the lion share of the treasury, they could still be fine re distribution. They would merely have to reach an agreement to split this “premine” with their other partner banks who invest in XRP as a bridge currency. Maybe they unlock all of their currency programmatically with pro rata distributions to partner institutions…a central bank on auto-pilot where early buy-in gets rewarded with rights to secondary sale proceeds. Then the banks get in on the action of selling new quasi-legal tender to the masses!

+ It’s not really innovative because it’s a centrally managed protocol. I don’t really know how to treat this one. XRP is a really bad crypto-currency, but it could be a great skynet currency if they somehow managed to trick all the central banks and correspondent banks that there were no other options, but to give up their money-printing powers.