“Who’ll buy all the debt?!”

So goes the overwrought interrogative whenever the discussion turns to profligate governments and fiscal largesse.

It’s supposed to be a rhetorical question. The (implied) answer says there’s more supply than demand, and that for the market to clear, yields will have to rise materially, further imperiling government finances.

We’re not used to hearing the question applied to high-grade, US corporate credit (massive issuance is easily absorbed because the best corporates are in some cases and on some vectors viewed as better credits than developed market sovereigns, absurd as that is), let alone to big-cap US equities (for nearly two decades, demand’s exceeded supply, hence an ever-shrinking float).

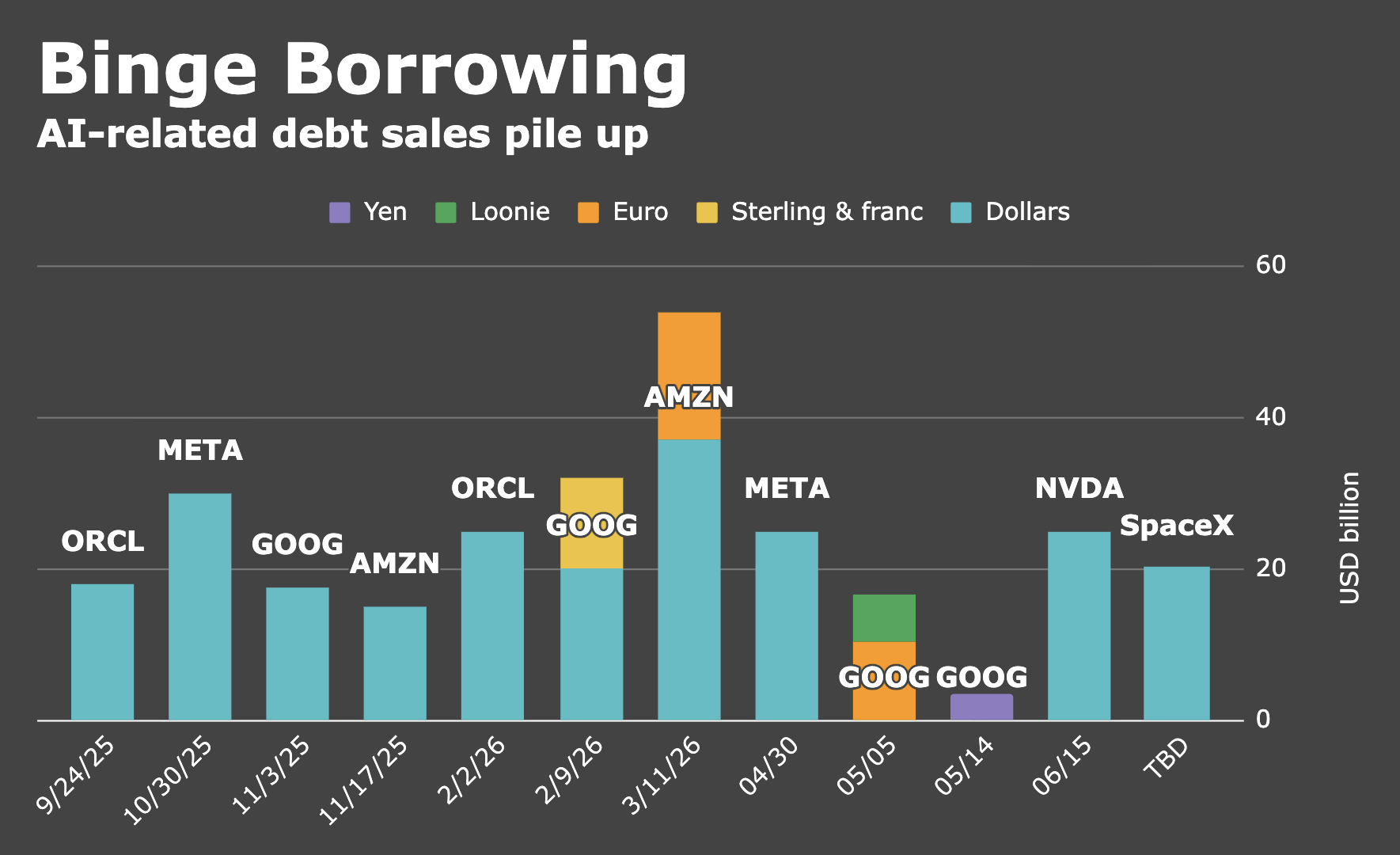

Suddenly, thanks almost entirely to massive outlays for AI data center construction and leasing, there are questions not just around whether the IG corporate credit market might eventually evidence indigestion with a never-ending succession of mega-deals (since Oracle started it all in September, total AI-related supply, inclusive of Nvidia’s June deal and SpaceX’s inaugural bond sale, as well as foreign-currency deals from Alphabet and Alphabet, exceeds $271 billion), but whether the equity market might struggle to absorb a series of major supply events.

The argument’s straightforward: Between SpaceX’s IPO, expected public debuts from OpenAI and Anthropic, possible follow-ons from the hyper-scalers (à la Alphabet’s massive equity raise) and a reduction not necessarily in the overall quantum of buybacks, but rather in the growth rate of aggregate executions given mega-tech’s prioritization of capex over shareholder returns, stocks could build in their own “concession” to account for the supply-demand shift, where that means equity prices get less support in an environment where net supply’s consistently positive for the first time in almost 20 years.

If the question’s “Who’ll buy all the high-grade supply?” the answer’s probably, “Somebody.” Because… well, because as I put it last week, while editorializing around SpaceX’s inaugural debt sale, “What’s not to like? You’re loaning money to an alleged, former ketamine addict to build AI data centers on the moon.” (That’s never gonna get old.)

If the question’s “Who’ll buy all the stock?” the answer’s probably still corporates, with help from retail investors who, as Citadel’s Scott Rubner recently remarked, “remain one of the strongest sources of demand in today’s market.”

I want to be cautious on the retail investor point. For one thing — and to his credit, Rubner alludes to this obliquely — Citadel has a vested interest in retail equity market participation and thus a vested interest in seeing it increase. Better than a third of all US-listed retail volume’s executed by Rubner’s employer.

Without casting aspersions (sincerely, because as any regular reader knows, I think Scott’s great and I don’t traffic in Citadel conspiracies), you have to keep that in mind when he says things like, “Retail trading activity has officially entered a new regime.” Or, “the defining characteristic of today’s retail investor is not just enthusiasm, but persistence.” Or, “Record [retail] activity does not necessarily imply exhaustion.” And so on.

For another thing, even if retail investors are “evolving,” as Rubner put it this month, one of their defining characteristics as a group is a penchant for FOMO and treating equities like poker chips.

To be sure, that’s a stereotype and I’d argue it doesn’t apply to the majority of retail investors because guess what? We’re all retail investors. (If you weren’t a retail investor, you’d know it.)

Nevertheless, the stereotype, like all stereotypes, serves a purpose. Stereotypes, even when derogatory, are one way the quick-thinking, intuitive part of our brain keeps us safe. Better to err on the side of caution even if, in doing so, we offend somebody.

With those caveats, the figure below from Scott’s pretty remarkable. It shows retail participation in cash equities. Note the emphasis.

The focus on cash equities (as opposed to options) doesn’t “sterilize,” so to speak, the data: You’re still seeing a manifestation of retail stereotypes like “FOMO” and “BTFD.” But it at least avoids the trap of equating outright gambling (i.e., retail options volume) with stock-buying.

In his latest note, Rubner observed that retail trading’s breaking records every three or so days across Citadel’s platform. Not surprisingly, the buy impulse is strongest on down days (i.e., retail net notionals are positive and larger on dips).

More importantly — and this is what really counts, I think — overall ETF-buying’s on track for a mammoth year in 2026, as shown on the left below. Rubner’s chart uses Bloomberg data, but the same’s evident in EPFR’s series, which reflects a near $800 billion inflow to global equity ETFs already in 2026.

The figure on the right shows you buyback authorizations across the entire US equity universe, broken down by sector.

That chart (the buyback chart) gives you the 30,000-foot view. Contrast it with the alarming chart I showed you late last week, when I flagged no YTD authorizations from the hyper-scalers.

“The scale of [ETF] flows remains extraordinary,” Rubner wrote, noting that during the first six months of 2026, equity ETFs attracted “more than twice the amount that historically represented a full year’s worth of flows.”

As to the corporate bid, Rubner said “the largest buyer of US equities remains active,” with the C-suite having authorized more than $925 billion of share repurchases, the strongest pace ever recorded through this point in the year.”

{kind=link}

Do the cash and ETF charts exclude or include leveraged ETFs and single stock double or triple performance?

How those retail buyers are making those stock purchases ought to be concerning.

FINRA Debit Balances in Customer’s Securities Margin Accounts:

May ’25 = $921B -> May ’26 = 1.416T

Two weeks ago or so I saw a table of who is stepping up their UST bond purchases and who is reducing them. (In the FT as I recall.) It indicated that the only group increading their purchases have been hedge funds doibg carry trades. They pretty much offst faling demand elsewhere. We know how leveraged those purchases are.

Today there was a piece on how private equity managers are having problems selling most of their portfolios of companies. The inventory build-up numbers were surprising to me.

So I guess it’s “all” going into AI trades?

I am 62, and the only example I can recall of a large U.S. corporation issuing large amounts of stocks and bonds at the same time was Ford in the early 2000’s. In that case, Ford was trying merely to survive — and they succeeded in that — although their share price has been stuck in the $9-14 range ever since. I am not so worried about the stocks: if the hyper-scalers want to dilute their (potentially?) overpriced shares, and people are willing to sign on, so be it. That is capitalism. The bond issuance is more concerning. Fitch and Moody’s and have allowed themselves to mislead investors before, and the credit worthiness of the hyper-scalers going forward must be rather challenging to accurately assess to say the very least. Additionally, competition with government issuance will push yields higher, and private credit still remains a largely unknown X-factor. As a reminder, if the bond market goes, everything else usually goes with it.

Does this mean the trillions sitting on the sidelines is moving into stocks?