The marquee gauge of US services sector activity was kinda “blah” in data released Wednesday, seemingly confirming a decidedly lackluster signal from the preliminary read on a separate index two weeks back.

The ISM services headline was 52.8, short of the 54 consensus. 51.3 on the new orders gauge was a seven-month low and represented a three-point decline versus December’s readout. Between that and a 3.5ppt drop on the business activity gauge, you could certainly argue the release was soft.

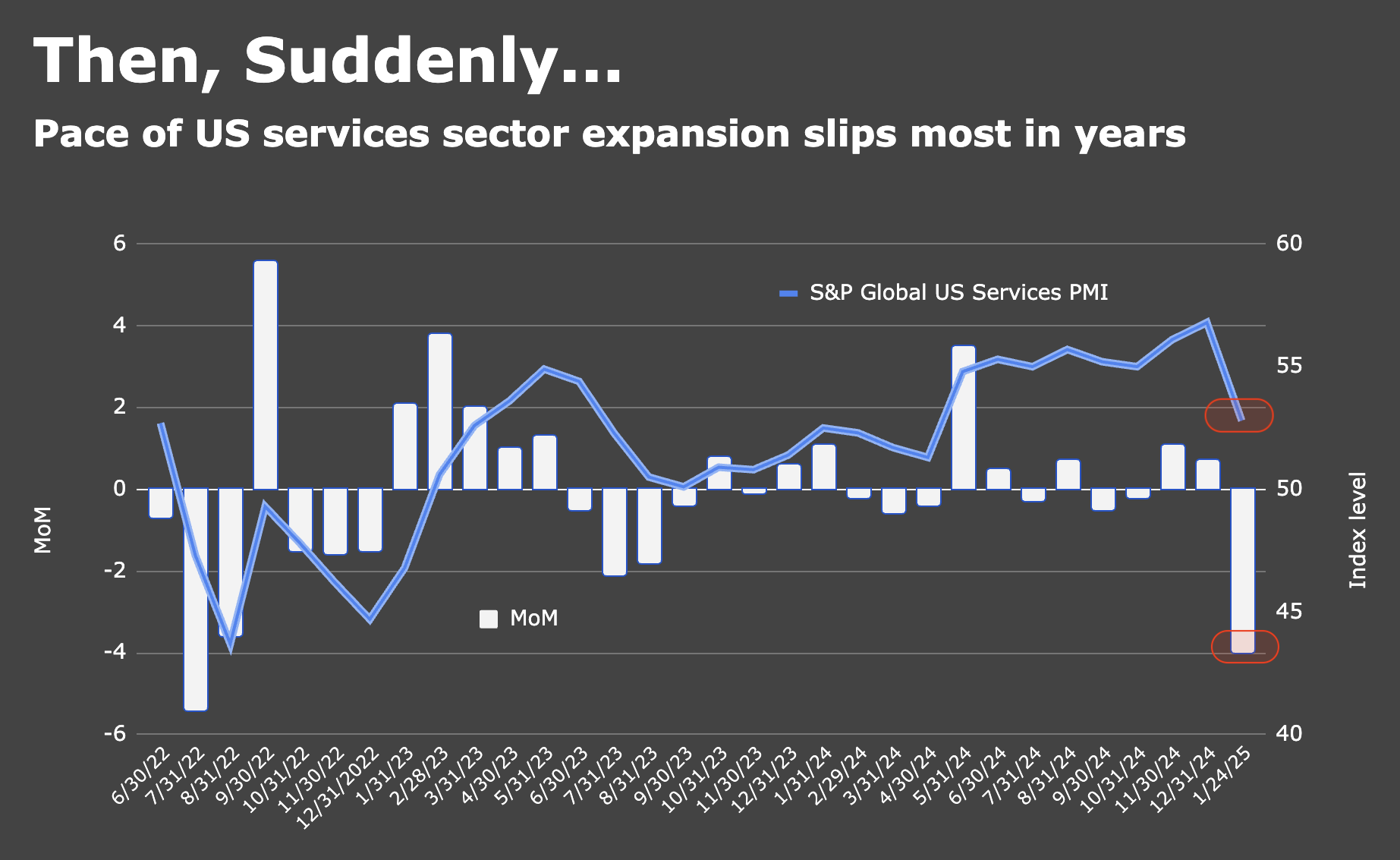

Similarly, S&P Global’s US services PMI printed 52.9 in the final read for January, (virtually) unchanged from the above-mentioned flash print.

Recall that the near four-point month-to-month drop on S&P Global’s gauge covering last month was the largest since 2022.

“Service sector businesses reported a slowdown at the start of 2025, with activity levels growing at a reduced pace compared to the robust gains seen late last year,” S&P Global’s Chris Williamson said Wednesday, suggesting some of the downshift might’ve been a function of cold weather which, as it turns out, is typical of the winter months.

And yet, despite the headline miss, I’d casually suggest the details of the ISM release were actually encouraging to the extent they tipped a marginally stronger hiring impulse, moderating (if still pervasive) price pressures and a respectable (if no longer galloping) expansion.

Specifically, the subindexes were still broadly above 50, and the employment gauge moved up to 52.3, a 16-month high, suggesting better luck for employers in sourcing qualified candidates, steady demand for workers or both. That’s good news. Further, the prices gauge moved lower to 60, still far too warm if you’re the Fed, but a four-point decline from December’s very uncomfortable temperature check.

Beyond that, there’s not a lot of utility in parsing these releases. It’s soft data, and I don’t think you’re going to glean a lot beyond the brief (for me) summary above. Simply put: The US services sector’s holding up, but may be cooling at the edges, which is good news from an inflation perspective, and as long as any demand downshift doesn’t manifest in job losses.

Notably, the nascent slowdown in services comes just as US manufacturing appeared to turn up, anecdotally anyway. Recall that both the ISM and S&P Global factory PMIs printed in expansion territory for January in data released earlier this week, the first simultaneous readings above 50 since March.

Williamson summed up the situation in services. January evidenced “some pullback in buoyant post-election optimism [but] a marked upturn in hiring supports the view that robust growth should resume,” he said, before cautioning that “hopes of more rate cuts will be diminished by the combination of increased hiring, reports of labor supply difficulties” and lingering price pressures.

{kind=link}

Having a mad king and a bunch of crazy henchmen will not help confidence. Plus we are kind of due for a slowdown after a post covid surge. The numbers are suggesting a slow decay in the economy’s orbit.

Business likes it ‘steady as she goes’. How do you invest for the long term when the ship’s captain changes the destination daily, or three times a day, and using his stable genius mind decides rudders are for suckers and losers.